- Laws Governing NRI Residential Status in India

- New Definition of Tax Residency in India

- 120-Day Rule for High-Income NRIs and PIOs: Key Change Explained

- Understanding Resident but Not Ordinarily Resident (RNOR) Status

- Deemed Residency Rule Under the Income Tax Act

- Other Important Residency Rules for NRIs

- Taxability of Income for NRIs and RNORs in India

- Foreign Income Taxability Under the New Income Tax Bill

- What Is Considered Income Earned in India?

- What Is Considered Income Accrued in India?

- Tax Deductions Available to NRIs Under Section 80C

- How Can NRIs Avoid Becoming Tax Residents in India?

- Summary of New NRI Taxation and Residency Rules

- Conclusion: Impact of New Residency Rules on NRIs

A Non-Resident Indian (NRI) is an Indian citizen who lives overseas for employment, education, or business purposes. However, being an NRI does not fully exempt an individual from Indian taxation. If an NRI earns or receives income in India, they are required to pay tax in India as per the applicable provisions of the Income Tax Act.

For non-resident Indians, the Income Tax Act, 1961, prescribes specific tax rules that have evolved over time. In this context, on 13 February 2025, the Central Government of India introduced the Income Tax Bill 2025 in Parliament, proposing a major overhaul of the existing tax system to simplify compliance and improve clarity.

A key feature of the proposed bill is a significant revision to tax residency rules, which will come into effect from 1 April 2026. These changes are expected to impact NRIs, Persons of Indian Origin (PIOs), and frequent foreign visitors to India. Understanding these new rules is essential for effective tax planning and compliance. This blog explains the updated NRI taxation and residency provisions under the Income Tax Act, so let’s get started.

- The NRI status in India is governed by two primary laws: the Income Tax Act, 1961, and the Foreign Exchange Management Act (FEMA).

- Residential status determines the tax liability of an individual. While residents are taxed on their global income, non-residents are taxed only on income sourced or received in India.

- An individual is considered a resident if they stay in India for 182 days or more in a financial year, or 365 days in the preceding four financial years, along with 60 days (or 120 days, where applicable) in the current year.

- Common sources of income for NRIs include rental income from property in India, capital gains, and interest earned on NRO accounts.

- Interest earned on NRE and FCNR accounts is exempt from tax in India, subject to compliance with FEMA regulations.

- An NRI can avoid double taxation by claiming benefits under the Double Taxation Avoidance Agreement (DTAA). For this, they must submit a Tax Residency Certificate (TRC) and Form 10F, as applicable.

Laws Governing NRI Residential Status in India

In Indian, the NRI status is prescribed and governed by two main laws. These are as follows:

- Income Tax Act 1961: It states the NRIs' tax liabilities in India

- Foreign Exchange and Management Act (FEMA): This act governs all investments and transactions, opening of bank accounts, and more of NRIs in India.

Under both acts, the definition of an NRI is different. Also, a person's NRI status is calculated based on the number of days they stayed in Indian during a financial year.

New Definition of Tax Residency in India

Under the revised 2025 income tax bill, a person will be considered an Indian resident if they fulfil either of the following conditions:

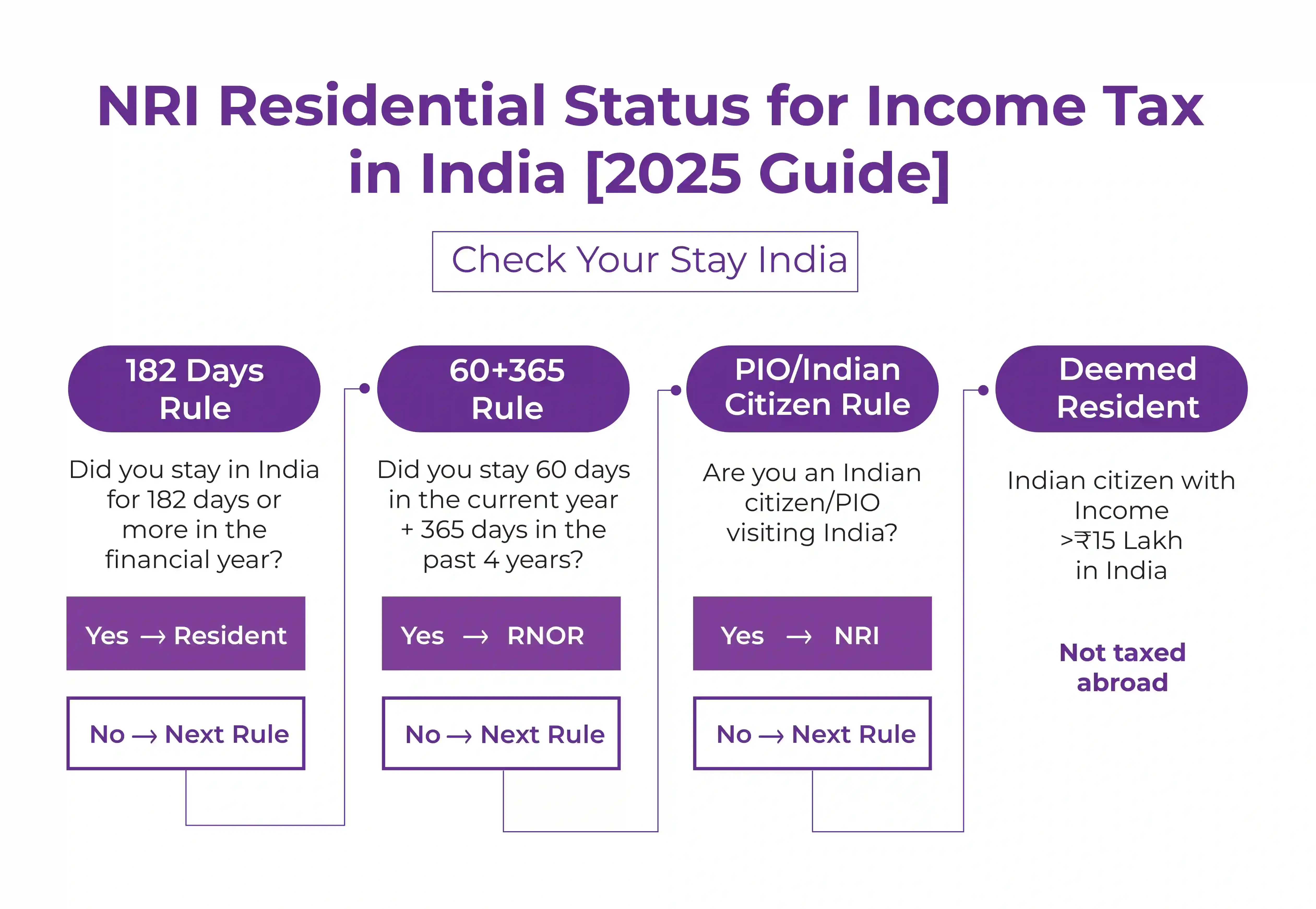

182-Day Rule (Unchanged Under the Income Tax Act, 1961)

A person will be considered a tax resident in India if they stay in the country for 182 or more days in an accounting year. To know the residential status, this remains a primary factor. Whereas, if a person remains less than 182 days in India, they will continue to be known as an NRI. With no additional conditions mentioned in the new income tax bill issued by the Indian government, the 182-day rule remains the same.

60-Day + 365-Day Rule (Revised Residency Conditions)

Previously, a person who stayed in the country for 60 or more days in a financial year was considered a tax resident in India and lived in India for 365 days over the last four years. While the rule is the same, some exemptions have been made. These are as follows:

- Under the new tax regime, Indian citizens working overseas or serving on crew are no longer subject to the 60-day rule.

- Additionally, if NRIs and PIOs have earned INR less than 1.5 million in India, they are also not covered by this rule.

For instance, Shivam, an Indian citizen working in Australia, came to India for 100 days in a financial year. Under the old 60-day rule, Shivam might be classified as a resident in India. However, since he moved overseas for a job, he is now exempt from paying tax and remains an NRI.

*Note: In India, according to the residential status of the person, the tax liability of a person is calculated in that financial year, not according to his/her citizenship in the country. For tax purposes, a person who is a citizen of India can be considered an NRI for a specific year. Also, a foreign national can be considered an Indian resident under the tax laws.

Classification of Taxable Individuals in India

For income tax purposes in India, individuals are classified into three groups:

- Non-Resident (NR)

- Resident and Ordinarily Resident (ROR)

- Resident but Not Ordinarily Resident (RNOR)

120-Day Rule for High-Income NRIs and PIOs: Key Change Explained

Under the new income tax bills, for NRIs and PIOs who earn INR 1.5 million or more, an essential change has been made under the high-income category. Considering this, the 120-day rule has officially replaced the 60-day residency rule. According to the new rule, an NRI or PIO will be considered resident but not ordinarily resident if their income is more than 1.5 million in India and if they:

- In a financial year, they live in India for 120 or more days

- Have lived in India for 365+ days in the last four years

For instance, Ravi is an NRI earning INR 2 million in India and visiting the country for 30 days. According to the previous rule, he would be classified as an NRI, but under the new rule, he is now known as an RNOR.

Why Is the 120-Day Rule Important for NRIs and PIOs?

Here are the two key reasons why this new rule is essential for NRIs:

- As an RNOR, only the income that a person earned in India is taxable, while their global income remains tax-free in India.

- If a person lives in India for 182 days, they become an Indian resident, and their global income is now taxable in India.

Understanding Resident but Not Ordinarily Resident (RNOR) Status

A person is classified as not ordinarily resident (NOR) in India if they fulfil any of the following conditions:

- For nine out of the last ten years, they were an Non-Resident Indian

- Over the last seven years, they have lived in India for 729 days or fewer

- They are citizen of India or PIOs with Indian income of more than INR 1.5 million and have lived in the country for 120 to 180 days in an accounting year.

For instance, Avinash, a non-resident Indian, returned to India and has lived here for only 500 days over the last seven years. He will be classified as NOR. It means he is liable to pay tax on the income he earned in India, even though his global income is tax-free in the country.

Deemed Residency Rule Under the Income Tax Act

Under the new income tax bill, a debatable provision is the deemed residency rule. The deemed residency rule applies to Indian citizens whose income in India exceeds INR 1.5 million but who are not paying tax in any other foreign nation. This rule affects Indian residents living in tax-free jurisdictions such as Monaco, the UAE, or Saudi Arabia who have significant income from India. Here, it is worth noting that even if that person has never visited India, they can still be considered a tax resident in India, making their global earnings taxable in the country.

For example, Amit, an Indian citizen employed in Dubai who does not pay income tax, earns INR 2 million in India but does not visit the country. Under the new income tax rules, he will still be treated as an Indian resident and will need to pay tax on his global income in India.

Other Important Residency Rules for NRIs

Here are the other important residency rules associated with the income tax laws in India:

- Crew Members of Foreign Ships: The time of the crew members who are Indian residents is calculated in India under special rules.

- Association of Persons (AOPs), Firms, Trusts, and Hindu Undivided Family (HUF): Unless the entire control and management of these entities is outside India, these are considered Indian residents.

- Companies: A company is taxable in India if:

- If the company is an Indian-incorporated entity

- The Place of Effective Management (PoEM) of the company is located in India

For example, if the main management decisions of a foreign company are taken in India, it will be known as a tax resident in India.

Taxability of Income for NRIs and RNORs in India

If you are an NRI, and if you are earning any income in India or any income is accrued in India, then on that money, you need to pay tax in the country. Here, the money you earn outside the country is not taxable. Additionally, the income of a non-resident seafarer for services provided outside the country on a foreign ship is not included in their income taxable in India, even though they receive their salary in an NRE account with an Indian bank.

For example, a seafarer rendered services in Europe and lived in India for less than 182 days. He received his salary in his NRE Account with an Indian bank. Here, his income will not be taxable in India.

If you are RNOR and have just come to India, you can maintain this status for a maximum of 3 accounting years after your return to the country. It can assist you with taxes in a big way since your Indian taxation will be in line with that of an NRI. Hence, the money that you earn outside India will not be taxable in the country. Therefore, like a non-resident Indian (NRI):

- Any income that you earn inside India is taxable.

- The income that you earn outside India, for which you do not need to pay tax for up to three years after your return

However, once you become an Indian resident, all your income, whether you earn inside or outside India, will be taxable in the country, barring any claims that may be applicable under the Double Taxation Avoidance Agreement (DTAA) between India and any foreign country from which you earned your income.

Foreign Income Taxability Under the New Income Tax Bill

Income that you earned outside Indian is considered as foreign income, except for these:

- Professional earnings, if the professional practice was situated in India

- Income from business, if it is controlled and managed from India

For example, Anshul is an NRO and earned INR 50 million in income from his business in Dubai. Since his business is set up in Dubai, he did not need to pay tax in India. However, if his Dubai business were managed from India, it would be subject to Indian tax.

What Is Considered Income Earned in India?

Any income that you or someone on your behalf received in India is known as 'income earned in India.' Additionally, any earnings that arise or accrue in India, or that Indian tax law treats as arising or accruing in India, are part of income earned in India. Under the Income Tax Act 1961, whether an Indian resident or an NRI earns it, these incomes are taxable in India, and to avoid double taxation on the same income, a person can claim tax relief under a DTAA.

What Is Considered Income Accrued in India?

It is mentioned in Section 9 of the Income Tax Act, 1961. This tax rule applies to everyone whose income arises or accrues in India, irrespective of their residential status in the country. Confused? To help you out, here are some questions. If any of the following questions have a Yes answer from your side, then your income will be considered accrued in India:

- Income generated from a business connection in India.

- You receive money from any asset, property, or source of income in India.

- From the assets transfer situated in India, a capital gain was received.

- Salary payable to you by the government of India for services rendered outside the country when you were a citizen of India.

- Received salary for services rendered in India.

- Technical fees, royalty, or interest, from the State or Central government, or from a specific person, in certain situations.

- Even though you already paid outside India, the dividend paid by an Indian company.

Instantly determine if you qualify as Resident, RNOR, or NRI under Indian Income Tax rules.

Tax Deductions Available to NRIs Under Section 80C

While filing ITR, NRIs under Section 80C can claim the following tax deductions in India:

- Payment made towards Life Insurance Premium

- Investment made in the Equity Linked Savings Scheme (ELSS)

- Tuition fees paid for children

- Paid for Unit Linked Insurance Plan (ULIP)

- Amount spent to repay the main loan amount taken for the construction or purchase of a residential property

Apart from Section 80C, NRIs can also claim tax deductions under Sections 80G, 80D, 80TTA, 54, and 54EC in India.

How Can NRIs Avoid Becoming Tax Residents in India?

To avoid tax residency in India, NRIs or any foreign resident can follow thefollowing stepss:

- If your income is INR 1.5 million or more in India, visit the country for less than 120 days.

- Strategically plan your visit across different assessment years.

- If you are living overseas in a tax-free country, wisely structure your income.

- To avoid deemed residency, keep your income below INR 1.5 million.

- To minimise tax liability in India, invest smartly in business and property.

Summary of New NRI Taxation and Residency Rules

From the above guide, i.e., new NRI taxation and residency rule under the Income Tax Act, these are the following takeaways:

- There are no changes in the 182-day rule; it remains the primary standard for residency.

- The 60-day residency rule no longer applies to crew members, NRIs, or Indian citizens working overseas.

- The 120-day rule applies to the high-income NRIs, who earn INR 1.5 million or more in India.

- Additionally, the deemed-residency tax rule applies to NRIs who earn 1.5 million or more in India but do not pay tax in any country.

- Through an RNOR status, individuals can avoid paying global taxation on the same income.

Conclusion: Impact of New Residency Rules on NRIs

This was all about the new NRI taxation and residency rules under the Income Tax Act. The 2025 Income Tax Bill has made significant changes to tax rules affecting NRIs, PIOs, and citizens of India living overseas. Considering this, to avoid paying unexpected tax in India, proper tax planning and maintaining residency status are vital. Apart from this, understanding these new tax provisions will help people make informed financial decisions and ensure compliance with India's tax laws. Furthermore, if you need more information on NRI taxation or are facing issues in filing ITR, connect with Savetaxs. We have professionals by our side who can help you in solving your tax-related queries and assist you in filing your ITR on time in India without any issues.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Expert CA-led ITR filing

- Laws Governing NRI Residential Status in India

- New Definition of Tax Residency in India

- 120-Day Rule for High-Income NRIs and PIOs: Key Change Explained

- Understanding Resident but Not Ordinarily Resident (RNOR) Status

- Deemed Residency Rule Under the Income Tax Act

- Other Important Residency Rules for NRIs

- Taxability of Income for NRIs and RNORs in India

- Foreign Income Taxability Under the New Income Tax Bill

- What Is Considered Income Earned in India?

- What Is Considered Income Accrued in India?

- Tax Deductions Available to NRIs Under Section 80C

- How Can NRIs Avoid Becoming Tax Residents in India?

- Summary of New NRI Taxation and Residency Rules

- Conclusion: Impact of New Residency Rules on NRIs

Frequently Asked Questions

According to Income Tax rules, an Indian citizen who has stayed overseas for carrying out business/ employment or vocation for 182 days or more during a financial year is considered an NRI. An NRI is liable to pay tax in India on income he/she received or earned in the country.

If an individual is 9 out of 10 accounting years a non-resident or lived in India for 729 days or fewer in the last 7 accounting years, that person will be considered as RNOR (resident but not ordinarily resident) in India.

In India, a resident is taxed on their total income that includes both the income they generate in the country as well as money received outside India. The tax burden on them is limited in the country to the money they earn in the country. Considering this, in case of NRI, the taxation rules change; they need to pay tax in both countries, in India or the foreign country from where they are generating money.

The concept of deemed residency was introduced in the Finance Act 2020. As per this, Indian citizens or NRIs whose income is 1.5 million or more in India but are not paying any tax on this in any other country. According to this, if a person never even visited India, they are still classified as a tax resident in the country, making their international income taxable in the country.

Generally, the foreign income is not taxable for NRIs and RNORs in India. However, they need to pay tax in India on the capital gains from fixed deposits, mutual funds, rental income from property and shares, applicable according to the income tax slab. Furthermore, from time to time, these rules are subject to change.