- What is NRI Income Tax in India?

- How to Determine Residential Status of an NRI?

- What Income is Taxable for NRIs in India?

- Income Tax Slabs for NRIs (FY 2025-26)

- NRO, NRE and FCNR Account Taxation for NRIs

- Deductions and Exemptions Available to NRIs

- Deductions and Investments Not Available to NRIs

- TDS on NRI Income

- When Should NRIs File Income Tax Return (ITR) in India?

- How Can NRIs Avoid Double Taxation?

- NRI Tax Implications: Practical Examples and Case Studies

NRI taxation in India is governed by the Income Tax Act, 1961, and depends primarily on your residential status and the source of income. NRIs are generally taxed only on income earned or received in India, including rental income, capital gains, dividends, salary for services rendered in India, and interest from NRO accounts.

This guide explains the key tax rules applicable to NRIs, including taxable income, tax slabs, deductions, TDS provisions, DTAA benefits, and ITR filing requirements, helping you understand and manage your tax obligations in India.

What is NRI Income Tax in India?

If you are a Non-Resident Indian (NRI), you are generally taxed in India only on income that is earned, received, accrued, or deemed to accrue in India. Income earned and received outside India is generally not taxable for NRIs.

Common taxable income sources for NRIs include:

-

Rental income from property in India

-

Interest earned on NRO accounts

-

Capital gains from Indian property, shares, or mutual funds

-

Dividend income from Indian investments

-

Salary for services rendered in India

-

Business or professional income earned in India

However, interest earned on NRE and FCNR accounts is generally tax-free, subject to applicable conditions.

Key Takeaways for NRIs

| Income Type | Taxable in India? |

|---|---|

| Foreign salary earned abroad | No |

| Salary for services rendered in India | Yes |

| Rental income from Indian property | Yes |

| Capital gains from Indian assets | Yes |

| Interest from NRO account | Yes |

| Interest from NRE account | No |

| Interest from FCNR account | No |

| Foreign rental income | No |

Understanding what income is taxable is the foundation of NRI taxation. The next step is determining your residential status, as it directly impacts how your income is taxed in India.

How to Determine Residential Status of an NRI?

Residential status is the foundation of NRI taxation in India. Before calculating your tax liability, you must determine whether you qualify as a Resident, Resident but Not Ordinarily Resident (RNOR), or Non-Resident Indian (NRI) under the Income Tax Act.

Your residential status determines the scope of income taxable in India and your eligibility for various tax provisions.

Why Residential Status Matters

Your residential status affects:

-

Taxability of Indian income

-

Taxability of foreign income

-

Disclosure requirements

-

Eligibility for deductions and exemptions

-

Income tax return filing obligations

Basic Conditions for Residential Status

You will be treated as a Resident in India if you satisfy either of the following conditions during a financial year:

Condition 1: Stay in India for 182 Days or More

You are considered a resident if you stay in India for 182 days or more during the financial year.

Condition 2: Stay in India for 60 Days or More and 365 Days in the Previous Four Years

You are considered a resident if:

-

You stay in India for 60 days or more during the financial year, and

-

You stay in India for 365 days or more during the four preceding financial years.

If you do not satisfy either condition, you will generally qualify as a Non-Resident Indian (NRI).

Residential Status at a Glance

| Condition | Residential Status |

|---|---|

| Stay in India for 182 days or more | Resident |

| Stay in India for 60 days or more and 365 days in the previous 4 years | Resident |

| Does not satisfy either condition | NRI |

Types of Residential Status

For income tax purposes, individuals generally fall into one of the following categories:

Resident and Ordinarily Resident (ROR)

A Resident and Ordinarily Resident is generally taxed on worldwide income, including income earned in India and abroad.

Resident but Not Ordinarily Resident (RNOR)

RNOR is a transitional status that may apply to individuals returning to India after living abroad. Under certain conditions, some foreign income may remain outside the scope of Indian taxation.

Non-Resident Indian (NRI)

An NRI is generally taxed only on income that:

-

Is earned in India

-

Is received in India

-

Accrues or arises in India

-

Is deemed to accrue or arise in India

Foreign income earned and received outside India is generally not taxable in India for NRIs.

Expert Tip: Many NRIs incorrectly assume that moving abroad automatically makes them a non-resident. Your residential status depends on the number of days spent in India during the financial year and must be reviewed every year.

Once your residential status is determined, the next step is understanding how different NRI bank accounts—NRO, NRE, and FCNR—are taxed in India.

What Income is Taxable for NRIs in India?

As an NRI, you are generally taxed only on income that is earned, received, accrued, or deemed to accrue in India. Income earned and received outside India is generally not taxable in India.

The taxability of income depends primarily on its source rather than your citizenship.

Taxable Income for NRIs at a Glance

| Income Source | Taxable in India? |

|---|---|

| Salary for services rendered in India | Yes |

| Rental income from property in India | Yes |

| Interest from NRO account | Yes |

| Interest from NRE account | No |

| Interest from FCNR deposits | No |

| Capital gains from Indian assets | Yes |

| Business income earned in India | Yes |

| Foreign salary earned abroad | No |

1. Salary Income

Salary is taxable in India if the services are rendered in India, irrespective of where the salary is credited or received.

Taxable: Salary for work performed in India

Generally Not Taxable: Salary for work performed outside India

2. Income from House Property

Rental income from a property located in India is taxable in India, even if the property owner resides abroad.

NRIs can claim:

-

Standard deduction of 30%

-

Home loan interest deduction under Section 24

-

Municipal taxes paid, subject to conditions

3. Interest Income

The tax treatment depends on the type of bank account.

| Account Type | Tax Treatment |

|---|---|

| NRO Account | Taxable |

| NRE Account | Tax-Free* |

| FCNR Deposit | Tax-Free* |

*Subject to maintaining NRI status and applicable regulations.

4. Business or Professional Income

Income earned from a business, profession, or consultancy that is controlled, managed, or carried out in India is generally taxable in India.

Examples include:

-

Consultancy services provided through an Indian office

-

Business operations managed from India

-

Professional income earned in India

5. Capital Gains

Capital gains arising from the sale of assets located in India are generally taxable in India.

Common examples include:

-

Residential property

-

Commercial property

-

Listed shares

-

Mutual funds

-

Bonds and securities

NRIs may be eligible to claim exemptions under Sections 54, 54EC, and 54F, subject to prescribed conditions.

6. Investment Income

Certain investment income earned from specified Indian assets acquired in foreign currency may be subject to special tax provisions under the Income Tax Act.

These may include:

-

Shares of Indian companies

-

Certain debentures

-

Government securities

-

Bank deposits and other notified assets

Understanding which income is taxable is only one part of NRI taxation. The next step is determining your residential status, which decides whether you are taxed only on Indian income or on a broader scope of income under Indian tax laws.

Income Tax Slabs for NRIs (FY 2025-26)

NRIs can choose between the old tax regime and the new tax regime while filing their income tax return. The Income Tax Slabs applicable to NRIs are generally the same as those applicable to resident individuals.

Income Tax Slabs Under the Old Tax Regime

The old tax regime allows taxpayers to claim eligible deductions and exemptions such as Section 80C, Section 80D, and home loan benefits.

| Taxable Income | Tax Rate |

|---|---|

| Up to ₹2,50,000 | Nil |

| ₹2,50,001 to ₹5,00,000 | 5% |

| ₹5,00,001 to ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Income Tax Slabs Under the New Tax Regime

The new tax regime offers lower tax rates but restricts many deductions and exemptions available under the old regime.

| Taxable Income | Tax Rate |

|---|---|

| Up to ₹4 lakh | Nil |

| ₹4 lakh to ₹8 lakh | 5% |

| ₹8 lakh to ₹12 lakh | 10% |

| ₹12 lakh to ₹16 lakh | 15% |

| ₹16 lakh to ₹20 lakh | 20% |

| ₹20 lakh to ₹24 lakh | 25% |

| Above ₹24 lakh | 30% |

Old Tax Regime vs New Tax Regime

| Particulars | Old Tax Regime | New Tax Regime |

|---|---|---|

| Basic Exemption Limit | ₹2.5 lakh | ₹4 lakh |

| Deductions & Exemptions | Available | Limited |

| Home Loan Benefits | Available | Restricted |

| Section 80C Deduction | Available | Not Available |

| Tax Rates | Higher | Lower |

Surcharge Rates for NRIs

A surcharge may apply if your total income exceeds specified thresholds.

| Total Income | Surcharge Rate |

|---|---|

| Above ₹50 lakh up to ₹1 crore | 10% |

| Above ₹1 crore up to ₹2 crore | 15% |

| Above ₹2 crore up to ₹5 crore | 25% |

| Above ₹5 crore | 37%* |

*Subject to applicable provisions and limitations under the chosen tax regime.

Health and Education Cess

A Health and Education Cess of 4% is levied on the total tax payable, including surcharge where applicable.

Rebate Under Section 87A

NRIs are not eligible to claim the rebate under Section 87A under either the old tax regime or the new tax regime.

Need Help Calculating Your NRI Tax Liability? Compare your tax liability under both regimes before filing your return to ensure you choose the most beneficial option.

NRO, NRE and FCNR Account Taxation for NRIs

Once you become an NRI, your banking arrangements in India must comply with FEMA regulations. To manage income earned in India and abroad, NRIs can use NRO, NRE, and FCNR accounts, each serving a different purpose and receiving different tax treatment.

NRO vs NRE vs FCNR Accounts

| Particulars | NRO Account | NRE Account | FCNR Account |

|---|---|---|---|

| Purpose | Manage income earned in India | Hold foreign earnings in India | Hold foreign earnings in foreign currency |

| Currency | Indian Rupees (INR) | Indian Rupees (INR) | Foreign Currency |

| Interest Taxability | Taxable | Tax-Free* | Tax-Free* |

| Repatriation | Limited | Freely Repatriable | Freely Repatriable |

| Suitable For | Rent, pension, dividends, interest | Overseas salary and savings | Foreign currency deposits |

*Subject to maintaining NRI status and applicable tax regulations.

NRO Account

An NRO (Non-Resident Ordinary) Account is primarily used to manage income earned in India, such as:

-

Rental income

-

Pension income

-

Dividend income

-

Interest income

-

Property sale proceeds

Interest earned on an NRO account is taxable in India and is generally subject to TDS.

NRE Account

An NRE (Non-Resident External) Account is designed for holding foreign earnings transferred to India.

Key benefits include:

-

Funds are fully repatriable

-

Interest earned is generally tax-free in India

-

Suitable for overseas salary and savings

FCNR Account

An FCNR (Foreign Currency Non-Resident) Account allows NRIs to maintain deposits in designated foreign currencies without converting them into Indian Rupees.

Key benefits include:

-

Deposits remain in foreign currency

-

Protection from exchange rate fluctuations

-

Interest is generally tax-free in India for NRIs

Which Account Should an NRI Use?

| Source of Funds | Suitable Account |

|---|---|

| Rent from Indian property | NRO Account |

| Pension from India | NRO Account |

| Foreign salary | NRE Account |

| Overseas savings | NRE Account |

| Long-term foreign currency deposits | FCNR Account |

Choosing the right account can help you manage funds efficiently while optimizing tax treatment. The next step is understanding the deductions and exemptions available to NRIs that can help reduce your tax liability in India.

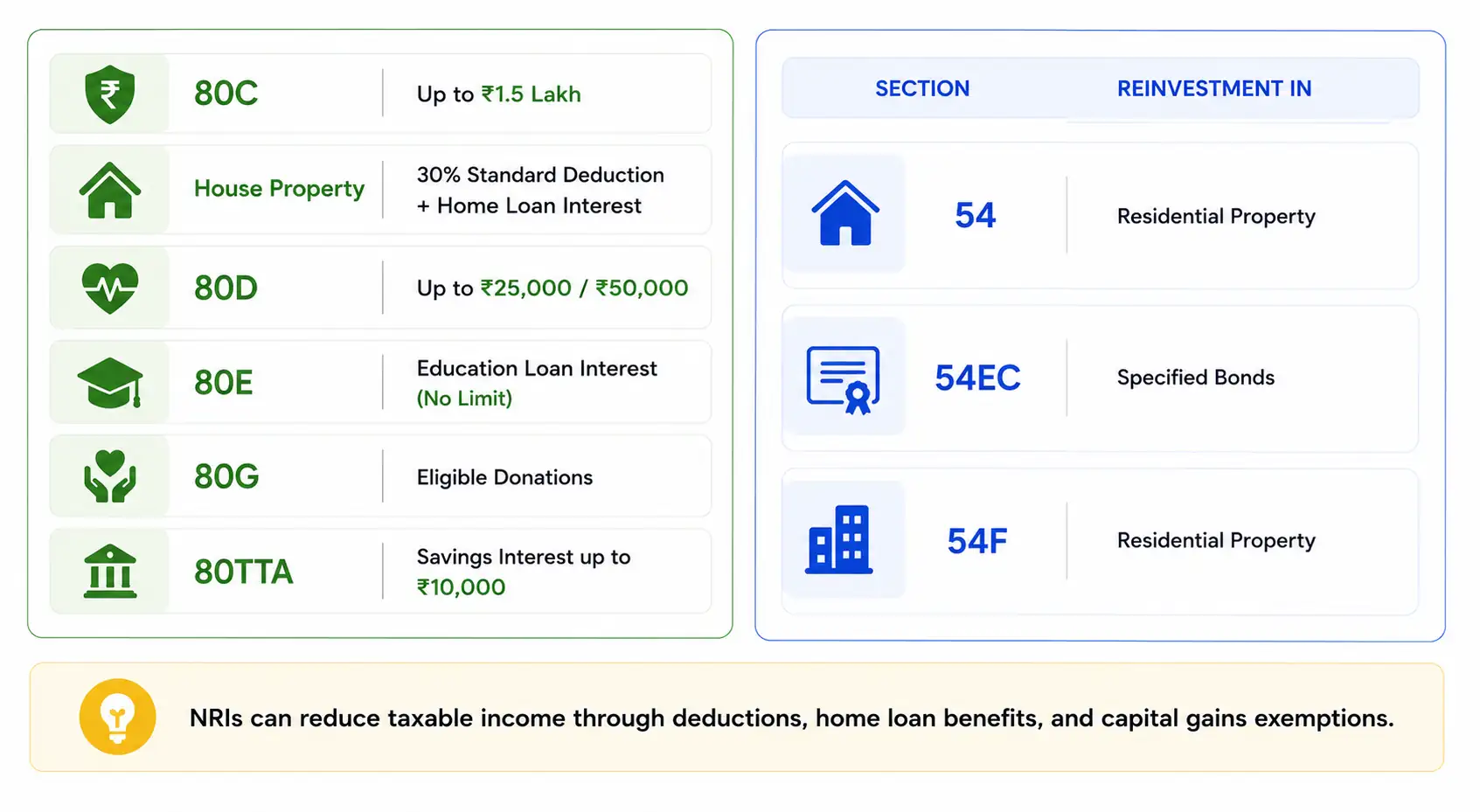

Deductions and Exemptions Available to NRIs

NRIs can claim several deductions and exemptions under the Income Tax Act to reduce their taxable income and overall tax liability in India. While some benefits are restricted to resident taxpayers, many commonly used deductions remain available to NRIs.

Deduction Under Section 80C

NRIs can claim a deduction of up to ₹1.5 lakh for eligible investments and expenses, including:

-

Life insurance premiums

-

ELSS investments

-

ULIPs

-

Children's tuition fees

-

Principal repayment of a home loan

-

Eligible tax-saving fixed deposits

Deduction for House Property

NRIs earning rental income from property in India can claim the same deductions available to resident taxpayers.

These include:

-

Standard deduction of 30% of net annual value

-

Home loan interest deduction under Section 24

-

Principal repayment deduction under Section 80C

-

Additional benefits under Sections 80EE and 80EEA, subject to eligibility

Deduction Under Section 80D

NRIs can claim deductions for health insurance premiums paid for themselves and eligible family members.

| Category | Maximum Deduction |

|---|---|

| Self, spouse and dependent children | ₹25,000 |

| Parents below 60 years | ₹25,000 |

| Senior citizen parents | ₹50,000 |

Deduction Under Section 80E

Interest paid on an education loan for higher education may be claimed as a deduction under Section 80E.

Key benefits:

-

No upper deduction limit

-

Available only on the interest component

-

Can be claimed for up to 8 years or until the interest is fully repaid

Deduction Under Section 80G

NRIs can claim deductions for eligible donations made to approved charitable institutions and funds, subject to the conditions prescribed under Section 80G.

Deduction Under Section 80TTA

NRIs can claim a deduction under section 80TTA of up to ₹10,000 on interest earned from savings accounts maintained with:

-

Banks

-

Co-operative societies engaged in banking

-

Post offices

This deduction is not available on fixed deposit or recurring deposit interest.

Capital Gains Exemptions for NRIs

NRIs may claim exemptions on long-term capital gains by reinvesting the gains or sale proceeds in specified assets.

| Section | Capital Gains Arising From | Reinvestment Required In |

|---|---|---|

| Section 54 | Residential Property | Residential Property |

| Section 54EC | Residential Property | Specified Bonds |

| Section 54F | Long-Term Capital Asset (other than residential property) | Residential Property |

Proper tax planning and utilization of available deductions can significantly reduce an NRI's tax liability. However, certain deductions and investment benefits remain unavailable to NRIs, which is important to understand before claiming tax benefits.

Deductions and Investments Not Available to NRIs

While NRIs can claim several deductions under the Income Tax Act, certain tax benefits and investment options are restricted to resident taxpayers. Understanding these limitations can help avoid incorrect claims and potential notices from the Income Tax Department.

Deductions and Investments Restricted for NRIs

| Deduction / Investment | Available to NRIs? |

|---|---|

| Public Provident Fund (PPF) – New Account | No |

| National Savings Certificate (NSC) | No |

| Senior Citizens Savings Scheme (SCSS) | No |

| Post Office 5-Year Deposit Scheme | No |

| Section 80DD | No |

| Section 80DDB | No |

| Section 80U | No |

Public Provident Fund (PPF)

NRIs cannot open a new PPF account after becoming non-residents. However, an existing PPF account opened while the individual was a resident can generally be continued until maturity, subject to applicable regulations.

Section 80DD

Section 80DD provides a deduction for expenses incurred on the maintenance and medical treatment of a dependent person with a disability. This deduction is available only to resident individuals.

Section 80DDB

Section 80DDB allows a deduction for expenses incurred on the treatment of specified diseases and medical conditions. This benefit is restricted to resident taxpayers and is not available to NRIs.

Section 80U

Section 80U provides a deduction to individuals suffering from a specified disability. This deduction is available only to resident individuals and cannot be claimed by NRIs.

Important: Residential status plays a key role in determining eligibility for deductions. Before claiming any tax benefit, ensure that the deduction is specifically available to non-resident taxpayers.

Apart from deductions, NRIs should also understand how Tax Deducted at Source (TDS) applies to different types of income earned in India, as it directly impacts tax liability and refund claims.

TDS on NRI Income

Tax Deducted at Source (TDS) is an important aspect of NRI taxation in India. In many cases, tax is deducted before the income is credited to the NRI, even if the final tax liability is lower.

If excess TDS has been deducted, NRIs can claim a refund by filing an Income Tax Return (ITR).

Common TDS Rates for NRIs

| Income Type | TDS Rate* |

|---|---|

| Rental Income from Property in India | 30% |

| Long-Term Capital Gains on Property Sale | 12.5% |

| Interest on NRO Account | 30% |

| Dividend Income | 20% |

*Applicable surcharge and cess may apply based on income level and specific tax provisions.

TDS on Rental Income

When an NRI earns rental income from a property located in India, the tenant is generally required to deduct TDS before making the payment.

If the actual tax liability is lower than the TDS deducted, the NRI can claim a refund through ITR filing.

TDS on Sale of Property

When purchasing property from an NRI, the buyer is generally required to deduct TDS before making payment.

Since the amount deducted may exceed the actual capital gains tax liability, filing an ITR is often necessary to claim eligible exemptions and refunds.

TDS on NRO Account Interest

Interest earned on NRO accounts and NRO fixed deposits is taxable in India. Banks generally deduct TDS automatically before crediting the interest.

TDS on Dividend Income

Dividend income received from Indian companies may also be subject to TDS. In certain cases, the applicable rate may be reduced through DTAA benefits, subject to the required documentation.

Can NRIs Claim a TDS Refund?

Yes. An NRI may be eligible for a tax refund if:

-

Excess TDS has been deducted

-

Taxable income is below the exemption limit

-

Eligible deductions reduce the final tax liability

-

DTAA benefits lower the applicable tax rate

The refund can be claimed by filing an Income Tax Return in India.

Do NRIs Need to Pay Advance Tax?

NRIs are required to pay advance tax if their estimated tax liability after considering TDS exceeds ₹10,000 during the financial year.

Failure to pay advance tax may result in interest being charged under Sections 234B and 234C.

Understanding TDS obligations is important, but filing the correct Income Tax Return is equally essential for claiming deductions, refunds, and maintaining tax compliance in India.

When Should NRIs File Income Tax Return (ITR) in India?

Many NRIs assume that filing an Income Tax Return (ITR) is unnecessary if tax has already been deducted at source. However, filing may be mandatory in some cases and beneficial in many others.

When is ITR Filing Mandatory for NRIs?

You are generally required to file an ITR if your total taxable income in India exceeds the applicable basic exemption limit during the financial year.

| Tax Regime | Basic Exemption Limit |

|---|---|

| Old Tax Regime | ₹2.5 lakh |

| New Tax Regime | ₹4 lakh |

When Should NRIs File an ITR Even if It Is Not Mandatory?

Filing an ITR may still be beneficial if:

-

TDS has been deducted on NRO interest

-

TDS has been deducted on rental income

-

TDS has been deducted on the sale of property

-

You want to claim a tax refund

-

You want to carry forward capital losses

-

You need income proof for loans, visas, or financial applications

-

You want to maintain tax compliance in India

Due Date for Filing NRI ITR

For most NRIs who are not subject to tax audit requirements, the due date for filing an Income Tax Return for FY 2025-26 is generally:

31 July 2026

The government may extend the due date in certain circumstances.

Which ITR Form Should an NRI File?

Choosing the correct ITR form is essential for accurate tax reporting.

| ITR Form | Applicable For |

|---|---|

| ITR-2 | Salary, house property, capital gains, interest, dividend income |

| ITR-3 | Business or professional income |

| ITR-5 | Firms, LLPs, and certain entities |

| ITR-6 | Companies |

Most NRIs with salary, rental income, capital gains, or investment income typically file ITR-2.

Documents Required for NRI ITR Filing

Keep the following documents ready before filing:

Identity & Residency Documents

-

PAN Card

-

Passport

-

Overseas residency or visa documents (if applicable)

Income Documents

Bank Account Documents

-

NRO account statements

-

NRE account statements

-

FCNR account statements

Capital Gains Documents

-

Sale deed and purchase deed

-

Capital gains statements

-

Brokerage and investment statements

-

Cost of acquisition records

How to File ITR as an NRI

The filing process generally involves:

-

Determine your residential status.

-

Calculate taxable income in India.

-

Choose the appropriate tax regime.

-

Select the correct ITR form.

-

Claim eligible deductions and exemptions.

-

Reconcile income with Form 26AS and AIS.

-

Apply DTAA benefits, if applicable.

-

File the return through the Income Tax e-Filing Portal.

-

Verify the return electronically.

Need Help Filing Your NRI Tax Return? Professional assistance can help ensure accurate reporting of capital gains, DTAA benefits, TDS credits, and eligible deductions while reducing the risk of notices and delays.

For NRIs earning income in multiple countries, understanding the Double Taxation Avoidance Agreement (DTAA) is equally important to avoid paying tax twice on the same income.

How Can NRIs Avoid Double Taxation?

Many NRIs earn income in more than one country. For example, you may earn a salary abroad while also receiving rental income, dividends, or capital gains from India. Without proper tax relief, the same income could be taxed in both countries.

To avoid double taxation, India has signed Double Taxation Avoidance Agreements (DTAAs) with several countries, including the USA, UK, Canada, Australia, Singapore, and the UAE.

What is DTAA?

A Double Taxation Avoidance Agreement (DTAA) is a tax treaty between two countries that helps taxpayers avoid paying tax twice on the same income.

The primary objectives of DTAA are:

-

Prevent double taxation

-

Reduce overall tax liability

-

Provide tax certainty

-

Promote cross-border investment and employment

Methods of DTAA Relief

DTAA benefits are generally available through one of the following methods:

1. Exemption Method

Under this method, income is taxed in one country and exempt in the other, as specified under the relevant tax treaty.

2. Tax Credit Method

Under this method, income may be taxed in both countries, but the taxpayer can claim credit for taxes already paid in one country while filing taxes in the other.

Income Commonly Covered Under DTAA

DTAA provisions may apply to:

-

Salary income

-

Rental income

-

Interest income

-

Dividend income

-

Capital gains

-

Royalty income

-

Professional income

-

Pension income

The exact tax treatment depends on the DTAA between India and the relevant country.

Documents Required to Claim DTAA Benefits

To claim treaty benefits, NRIs may need:

-

Tax Residency Certificate (TRC)

-

PAN Card

-

Passport copy

-

Self-declaration forms

-

Foreign tax payment records

-

Supporting income documents

What is a Tax Residency Certificate (TRC)?

A Tax Residency Certificate (TRC) is issued by the tax authorities of your country of residence and serves as proof that you are eligible to claim DTAA benefits under the applicable tax treaty.

In most cases, a valid TRC is essential for claiming treaty relief in India.

Section 89A and Foreign Retirement Accounts

Section 89A provides relief in situations where income accumulates in a foreign retirement account but is taxed only when withdrawn in the foreign country.

This provision helps eligible taxpayers avoid timing mismatches that could otherwise lead to double taxation.

Benefits of DTAA for NRIs

DTAA can help NRIs:

-

Avoid double taxation

-

Reduce tax liability

-

Claim foreign tax credits

-

Improve tax efficiency

-

Simplify cross-border tax compliance

Expert Insight: Many NRIs pay more tax than necessary simply because DTAA benefits are not claimed correctly. Reviewing treaty provisions and maintaining proper documentation can significantly reduce your overall tax burden.

Understanding the practical application of NRI tax rules is often easier through real-world examples. The following case studies illustrate some of the most common tax situations faced by NRIs.

NRI Tax Implications: Practical Examples and Case Studies

While the basic principles of NRI taxation are straightforward, the actual tax treatment often depends on factors such as residential status, source of income, and the nature of transactions. The following examples highlight some of the most common situations faced by NRIs.

Case Study 1: NRI Working Abroad

Rahul moved to the United States for employment during the financial year and qualifies as an NRI based on his stay in India.

During the year, he earned:

-

Salary from his US employer

-

Interest from an NRO fixed deposit in India

Tax Treatment

-

Salary earned and received abroad is generally not taxable in India.

-

Interest earned on the NRO fixed deposit is taxable in India.

Key Takeaway: NRIs are generally taxed only on income that arises, accrues, or is received in India.

Case Study 2: NRI Earning Rental Income from India

Anjali lives in Australia and owns a residential property in Pune that generates monthly rental income.

Tax Treatment

-

Rental income is taxable in India because the property is located in India.

-

The tenant may be required to deduct TDS before making rent payments.

-

Anjali can claim deductions such as:

-

30% standard deduction

-

Home loan interest deduction

-

Municipal taxes, subject to applicable provisions

-

Key Takeaway: Income from property situated in India remains taxable even when the owner is an NRI.

Case Study 3: NRI Selling Property in India

Amit, an NRI residing in Canada, sells a residential property in Mumbai after holding it for several years.

Tax Treatment

-

Capital gains arising from the sale are taxable in India.

-

The buyer may be required to deduct TDS before making payment.

-

Amit may claim exemptions under Sections 54, 54EC, or 54F if the prescribed conditions are satisfied.

Key Takeaway: Filing an ITR after a property sale by NRI in India is often necessary to claim exemptions, adjust TDS, and determine the actual tax liability.

What These Examples Show

The taxability of NRI income depends on several factors, including:

-

Residential status

-

Source of income

-

Nature of investments

-

Capital gains provisions

-

Applicable deductions

-

DTAA benefits

Reviewing your tax position each financial year can help ensure compliance, reduce tax liability, and avoid unnecessary penalties.

The most common questions NRIs have about taxation, deductions, refunds, and return filing are answered in the FAQ section below.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Expert CA-led ITR filing

- What is NRI Income Tax in India?

- How to Determine Residential Status of an NRI?

- What Income is Taxable for NRIs in India?

- Income Tax Slabs for NRIs (FY 2025-26)

- NRO, NRE and FCNR Account Taxation for NRIs

- Deductions and Exemptions Available to NRIs

- Deductions and Investments Not Available to NRIs

- TDS on NRI Income

- When Should NRIs File Income Tax Return (ITR) in India?

- How Can NRIs Avoid Double Taxation?

- NRI Tax Implications: Practical Examples and Case Studies

Frequently Asked Questions

Income up to INR 2.5/4.0 lakhs is tax-free for NRIs in India. This tax exemption is the same for both Indian residents and NRIs in India.

If the total income of the OCI is less than Rs 250000, then it is tax-free in India, if the income is between Rs 250000- Rs 500000, then they need to pay 5% tax, if the income is between Rs 500000- Rs 100000, then they need to pay 20% and if the income is more than Rs 1000000 then they need to pay 30% tax.

If an NRI sells an Indian property, the buyer has the right to deduct 20% TDS as long-term capital gains tax for properties sold after 2 years. However, if the property is sold within two years after its purchase, 30% TDS is deducted as short-term capital gains tax in India.

Yes, you can keep money in USD in your NRE account in India. However, once you deposit your foreign currency in this account, it will be converted into Indian INR, as these accounts are designed to manage and hold funds received outside India in Indian currency.