- What Is Residential Status Under the Income Tax Act and Why It Matters

- How to Determine Residential Status in India (Section 6 Rules)

- Resident and Ordinarily Resident (ROR): Meaning and Tax Implications

- Exceptions to Residential Status Rules Under Section 6

- Resident but Not Ordinarily Resident (RNOR): Definition and Taxability

- Non-Resident (NR) Status Under Income Tax Act

- Key Points to Remember While Determining Residential Status

- Important Terms Related to Residential Status Explained

- Taxability Based on Residential Status in India

- Residential Status of a Hindu Undivided Family (HUF)

- Residential Status of a Company Under the Income Tax Act

- Residential Status of Businesses and Other Entities

- Residential Status of LLPs, Firms, AOPs, BOIs, Local Authorities, and Artificial Juridical Persons

- Final Thoughts

In India, an individual's taxability is determined by his/her residential status under Section 6 of the Income Tax Act. It is worth noting that, under the income tax rules, residential status differs for different types of entities, such as individuals, corporations, and companies. The Income Tax Department needs to know a tax-paying individual or entity's residential status in India, especially at the time of income tax filing, as it is a key factor in determining a person’s tax liability.

Want to know more about it? This blog will walk you through the factors that help determine a person’s residential status in India, including the number of days spent in the country and their previous residency history. So, let’s begin by understanding the meaning of residential status.

- Their residential status determines a person's tax liability.

- The Income Tax Act defines three statuses - Resident and Ordinarily Resident (ROR), Resident but not Ordinarily Resident (RNOR), and Non-Resident (NR).

- An individual will be considered a deemed Indian resident if they are an Indian citizen and have income exceeding INR 15 lakhs.

- A person can be a resident of one or more countries, regardless of how many domiciles they have.

What Is Residential Status Under the Income Tax Act and Why It Matters

In India, an individual's taxability depends on their residential status for a specific financial year. Here, the term 'residential status' is defined under the Income Tax rules in India, and it should not be confused with a person's citizenship in India. It is only used for tax purposes. As per this, even if a person is an Indian citizen, they might be considered a non-resident, and a foreign citizen might be stated as a resident in the country during a specific accounting year.

Moreover, in India, the residential status of different types of individuals, such as firms, persons, or companies, is determined differently. Additionally, to determine a person's tax liability, it is necessary to know their residential status.

*Note: As per the amendment from the financial year 2020-21, a person who is a citizen of India with income exceeding INR 15 Lakhs or more from Indian sources is considered a deemed resident in the country isife/she is not liable to pay tax in any other nation due to domicile, residence, or other similar reason.

This was all about the meaning and importance of residential status in India to determine tax liability. Moving on, let's look at how to determine a person's residential status in the country.

How to Determine Residential Status in India (Section 6 Rules)

For income tax purposes, the Income Tax Act defines three statuses for determining residential status in India. These are as follows:

- Resident and ordinarily resident (ROR)

- Resident but not ordinarily resident (RNOR)

- Non-Resident (NR)

For the above-mentioned categories, the tax liability differs. So, before we get into the taxability, let's first know how a taxpayer in India becomes a resident, an NR, or an RNOR.

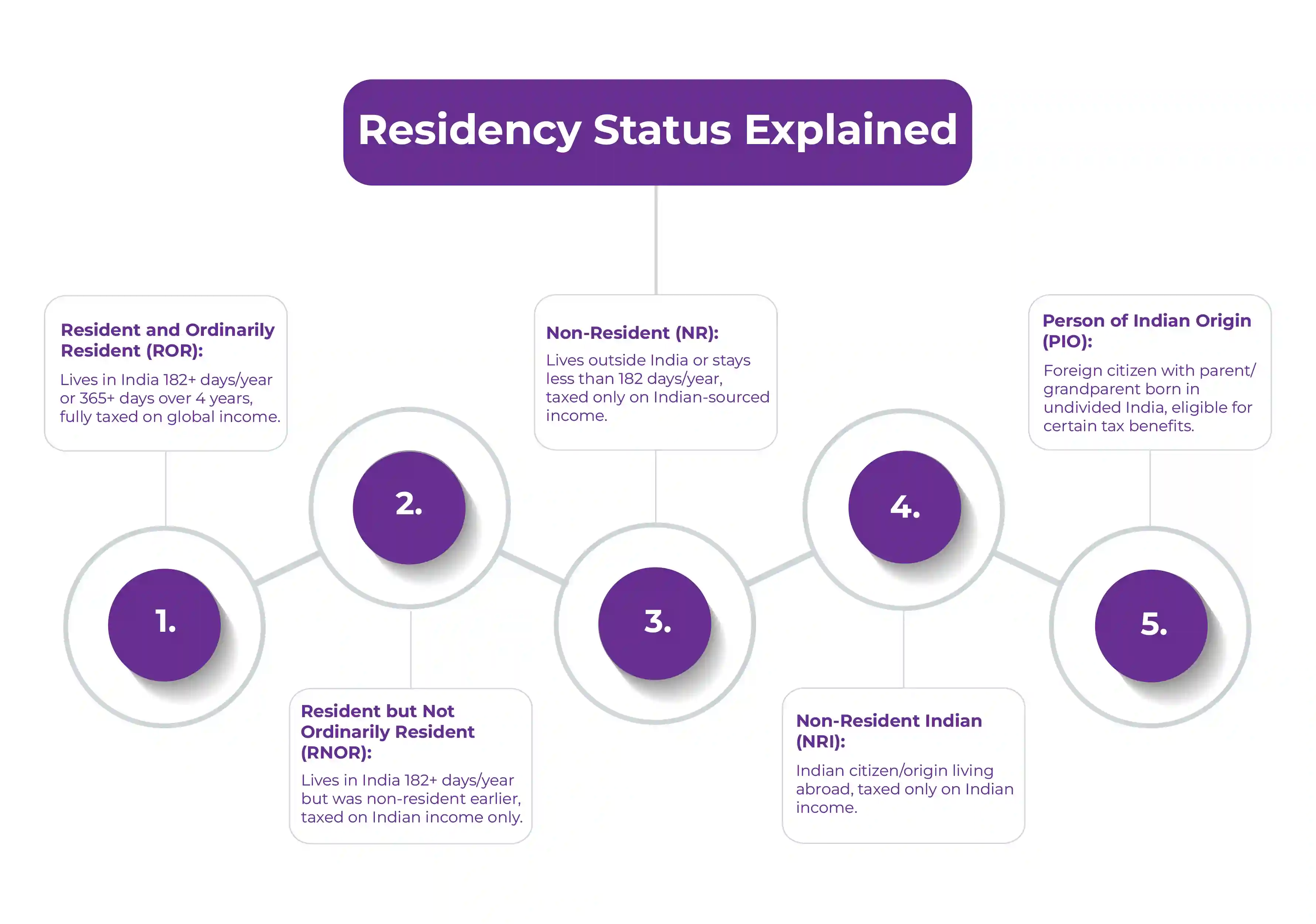

Resident and Ordinarily Resident (ROR): Meaning and Tax Implications

In India, a taxpayer would qualify as an Indian resident if they fulfill any of the following conditions:

- Live in India for 182 or more days in the previous year

- Stay in India for a total of 365 days or more in the last four financial years or 60 or more days in the current financial year.

If any person fulfills any of these conditions, under the income tax laws, they become an Indian resident. Moving ahead, let's know the exceptions to residential status.

Exceptions to Residential Status Rules Under Section 6

These are the following exceptions to residential status:

- Suppose an Indian citizen is a crew member of the Indian ship or, for employment purposes, leaves the country during the financial year. In that case, they will be considered an Indian resident if they stay in India for 182 days or more.

- Citizens of India or persons of Indian origin (PIO) who live outside India, visit the country during the financial year, and have a total income of more than INR 15 lakhs, other than the earnings from foreign sources during the previous accounting year, will be stated as Indian residents if:

- In the last year, if they lived in the country for 182 or more days

- Suppose they stayed in India for 365 days or more during the last four years. Additionally, lived in the country for at least 120 days in the previous year.

As stated in the above amendment, an individual will be treated as a 'deemed Indian resident' if he/she is an Indian citizen, have income exceeding INR 15 lakh, and have nil tax liability in other nations.

These are some of the exceptional cases under resident status. Moving ahead, let's know about a resident not ordinarily resident (RNOR).

Resident but Not Ordinarily Resident (RNOR): Definition and Taxability

A person with a close connection to India is considered an ordinarily resident. Factors like place of birth, nationality, or permanent residence can classify it. However, according to the Income Tax Act 1961, a person is known as an ordinary resident if he/she fulfills any of the following conditions:

- They have lived in India for 729 or more days in the seven years before the current financial year.

- Before the current financial year, if they have stayed in India for at least 9 of the 10 preceding financial years.

These are the situations in which a person will be stated as RNOR. Additionally, if a PIO or an Indian citizen has a total income of more than INR 15 lakh, excluding foreign income, and stayed in the country for 120 days or more but less than 182 days during that financial year, then the person will be considered an RNOR. Furthermore, deemed residents are classified as RNORs and are required to pay tax in India under this status. This clause applies to citizens of India who are not residents of any other country.

This was all about RNOR. Moving further, let's know who are non-residents in India.

Non-Resident (NR) Status Under Income Tax Act

A person will be classified as a non-resident in India if they fulfill any of the following conditions:

- If they live in India for less than 182 days in a financial year.

- If in a financial year, they did not stay in India for more than 60 days.

- If, in a fiscal year, they live in India for more than 60 days but, over the last four financial years, have not stayed in the country for 365 or more days.

If a person fulfills any of the above conditions, they will be considered a non-resident in India (NR). Well, this is how an individual's residential status is determined under Indian tax laws. However, to obtain this status, an individual must meet the required criteria. Want to know what it is? Read the following section and get your answers.

Instantly determine if you qualify as Resident, RNOR, or NRI under Indian Income Tax rules.

Key Points to Remember While Determining Residential Status

These are the following points that you need to consider while determining your residential status in India:

- Living in India also includes living in the country's territorial waters, i.e., from the coastline of India to 12 nautical miles offshore.

- The stay period in India must be active and continuous.

- When determining the number of days you stayed in India for your residential status, both your departure and arrival dates are considered.

- The residence of a person has nothing to do with their place of birth, citizenship, or domicile for income tax purposes. Hence, a person can be a resident of one or more countries, even though they have only one domicile.

While estimating a person's residential status for tax purposes in India, the following points are considered. Moving further, let's talk about the essential terms that you have generally heard during the payment of income tax.

Important Terms Related to Residential Status Explained

Before moving ahead, let's know the key factors included in Section 6 of the Income Tax Act, 1961. One should understand these terminologies:

- Non-Resident Indian (NRI): An individual who is an Indian citizen or of Indian origin but does not live in the country.

- Person of Indian Origin (PIO): A foreign citizen will be considered of Indian origin if they or either their parent or grandparents were born in undivided India.

- Income from Foreign Sources: It applies to income earned outside India. It does not include income sourced from a profession set or a business operated in India that is not deemed to arise or accumulate in the country.

These are some of the terms you need to understand when paying tax in India. Moving ahead, let's discuss how tax is charged in India based on a person's residential status.

Taxability Based on Residential Status in India

As mentioned above, in India, you pay tax based on your residential status. It helps determine how to file your income tax returns (ITR) and which tax obligations you have. In short, the tax filing requirements and liabilities are directly affected by whether a person or entity is considered a resident or NRI. Confused? Have a look at the table and clear any doubts you have about it.

| Resident and Ordinarily Resident (ROR) | A resident needs to pay tax in India on their total income. It includes money earned in India as well as obtained outside the country. |

|---|---|

| Non-Resident (NR) and Resident but Not Ordinarily Resident (RNOR) | The tax burden of NR and RNOR is limited to the income they earned or received in India. They do not need to pay tax on income earned outside India. Also, in case of double taxation on the same income, they can opt for the Double Taxation Avoidance Agreement (DTAA) that India has signed with other countries to provide tax relief to individuals and avoid paying tax twice on the same income. |

This is how a person's residential status in India determines their tax liability in the country. Moving ahead, let's know the residential status of the different entities.

Residential Status of a Hindu Undivided Family (HUF)

Let's know the residential status of HUF as per different categories:

- Resident HUF: If the management and control of the HUF are entirely or predominantly in India, and the members in the country take decisions, it is considered a resident HUF.

- Resident and Ordinarily Resident: If the Karta (manager) of HUF fulfils any of the below-mentioned conditions, it is classified as ROR:

- The Karta have stayed in India for a minimum of 2 years out of the last 10 years

- The Karta have lived in India for 730 or more days in the previous seven years

- Resident but Not Ordinarily Resident: If the Karta does not fulfil any of the above conditions, then the HUF is stated as RNOR.

*Note: Only persons and HUFs can be classified as resident not ordinarily resident in the country. All other entities can be stated as either resident or non-resident in India.

This was all about the HUF's residential status. Moving ahead, let's determine the company's residential status.

Residential Status of a Company Under the Income Tax Act

In the following conditions, a company will be considered a resident in India:

- If it is an Indian organization or a company

- If the place of effective management of the company in previous years was located in India

*Note: Here, the place of effective management (POEM) means the location where the decisions of the business related to management and commercial are taken, such as policy decisions and strategic planning.

This was all about a company's residential status. Moving on, let's look at how the residential status of businesses and other entities in India is determined.

Residential Status of Businesses and Other Entities

Here is how residential status for businesses and other entities is classified in India for tax purposes:

- Resident: If the management and control of the business and other entities are primarily exercised in India, then these entities are treated as residents.

- Non-Resident: If the management and control of the businesses and other entities are primarily exercised from outside India, these entities are treated as non-resident.

This was all about how residential entities of businesses and other entities are determined for tax purposes in India. Furthermore, let's look at the residential status of firms, LLPs, AOPs, and more in India.

Residential Status of LLPs, Firms, AOPs, BOIs, Local Authorities, and Artificial Juridical Persons

If the management and control of a firm, LLP, BOIs, AOPS, local authorities, and artificial juridical persons are wholly or partly located within India during the relevant financial year, they are said to be resident in India; if not, they are considered non-resident.

Final Thoughts

This was all about how the residential status under Section 6 of the Income Tax Act is determined in India for a person or any entity. It is vital to know your residential status in India, as this determines whether you need to pay tax in the country and fulfil your tax liability. If you are still confused about your residential status in India, or want to know about NRI taxation, contact Savetaxs. We have a team of tax experts who can solve any queries related to tax and help you with filing your ITR before the due date without any issues. So, why struggle when you have the option to take assistance? Connect with us and let us guide and assist you with your tax liability in India.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Expert CA-led ITR filing

- What Is Residential Status Under the Income Tax Act and Why It Matters

- How to Determine Residential Status in India (Section 6 Rules)

- Resident and Ordinarily Resident (ROR): Meaning and Tax Implications

- Exceptions to Residential Status Rules Under Section 6

- Resident but Not Ordinarily Resident (RNOR): Definition and Taxability

- Non-Resident (NR) Status Under Income Tax Act

- Key Points to Remember While Determining Residential Status

- Important Terms Related to Residential Status Explained

- Taxability Based on Residential Status in India

- Residential Status of a Hindu Undivided Family (HUF)

- Residential Status of a Company Under the Income Tax Act

- Residential Status of Businesses and Other Entities

- Residential Status of LLPs, Firms, AOPs, BOIs, Local Authorities, and Artificial Juridical Persons

- Final Thoughts

Frequently Asked Questions

Under Section 6 of the Income Tax Act, a person is an NRI if he/she has not stayed in India for 182 or more days during the fiscal year or if he or she lived in India for less than 365 days during the four years before the current financial year and less than 60 days in the current financial year.

According to the Income Tax Act, to become an Indian resident, a person needs to be physically present in the country for 182 or more days during the fiscal year. It is the minimum days that a person needs to stay in India to become a resident there.

Yes, RNOR is different from NRI. RNOR is a contraction for the resident but not ordinary resident, and applies to individuals of Indian origin opting to return to India after living overseas for several years. NRIs who have lived 9 out of 10 years outside India before the current financial year can be stated as RNOR.

Yes, in the course of one year, the residential status of a person can change in India, if he/she stays outside the country for more than 182 days. In India, the tax liability of a person is determined according to the number of days he/she stayed in the country.

If you stayed in India for 182 or more days during a financial year, yes, it can affect your NRI status. However, if you stay in the country for a limited time during your every visit, it will not impact your NRI status. For instance, staying in the country for 100 days during a fiscal year.