NRI Income Tax Compliance

Difference Between TDS and ITR for NRIsDifference Between TDS and ITR for NRIs

Written by Shubham Jain

The DTAA (Double Tax Avoidance Agreement) between India and the UK is an initiative made by the Indian government to prevent residents of both nations from being taxed twice on the same income. The Indian Government has signed DTAAs with almost 100 countries worldwide.

It allows different types of tax relief and deductions. Also, the taxes paid in one country can be claimed as a credit in another country under this tax treaty. An NRI or a business operating in both nations must understand this agreement to reduce their tax liability and ensure compliance.

In this blog, we will learn about the DTAA between India and the UK and understand the details for avoiding double taxation.

On 26 October 1993, India and the UK agreed to abide by the articles included in the DTAA and signed the agreement. With this agreement, both India and the UK can avoid paying taxes twice on the income earned in either country. An individual, a company, or an entity operating across India and the UK qualifies for the DTAA.

Anyone who resides in the UK for at least 182 days in a financial year can claim tax exemptions under the UK-India DTAA. This agreement consists of 31 articles and a few sub-sections that elaborate on the rules for claiming tax benefits by a tax resident of either nation.

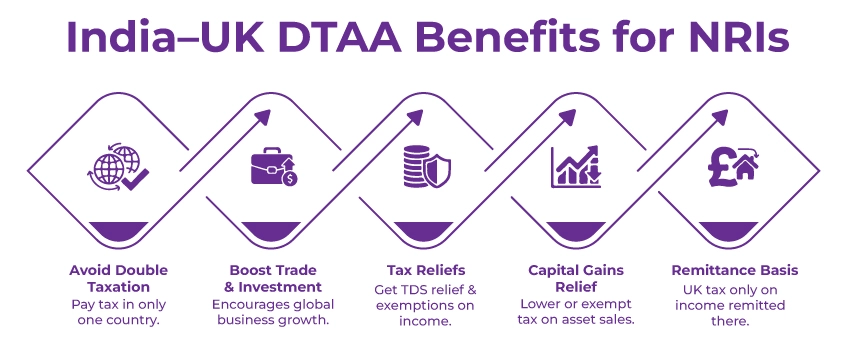

The India-UK DTAA offers several benefits to an NRI, which help them reduce their tax burdens, including:

The DTAA applies to two categories—United Kingdom Tax and Indian Tax.

Under DTAA, taxes that fall under the 'United Kingdom Tax' are:

Taxes in the 'indian Tax' category are:

These are some of the India-UK DTAA TDS rates:

Generally, Capital Gains are taxed under the domestic laws of India and the UK. It applies until they are specifically exempted under the treaty. Additionally, gains from air transportation and shipping contracts often qualify for the relief (Articles 8 and 9).

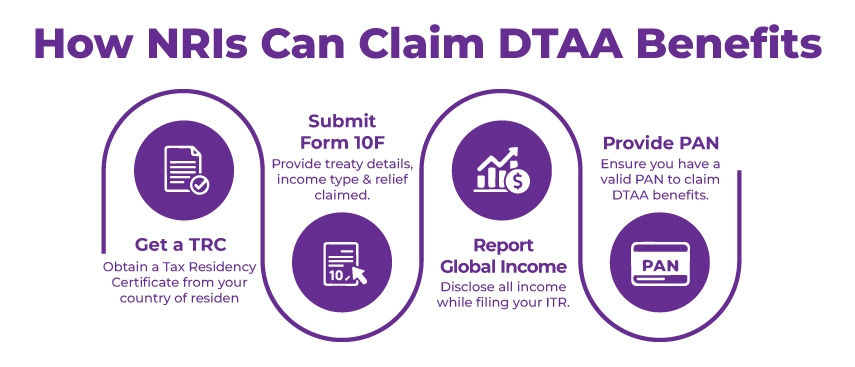

An NRI must follow the steps below to claim the benefits of the DTAA tax treaty:

Step 1: Obtain a TRC

Firstly, an NRI must get a TRC (Tax Residency Certificate) as it is an essential document required to avail the DTAA benefits. The TRC will be issued by the tax authorities of the NRI's country of residence. It will prove that the NRI is a tax resident of the country.

Step 2: Submit Form 10F

NRIs must fill Form 10F with the treaty's name, the income type, and the tax relief claimed. You must submit this form along with the TRC.

Step 3: Report Global Income in the ITR

Now, you must pay your taxes abroad and report your global income when filing your Income tax returns. You must report the accurate income to ensure compliance and avoid hefty penalties.

Step 4: Submit a Valid PAN

To claim the benefits under the DTAA, a PAN must be submitted. An NRI may face difficulties in claiming the relief if there is no PAN (Permanent Account Number).

Filing a DTAA comes with several benefits, but furnishing an improper application may attract problems. The following are some of the common mistakes that an NRI must avoid:

Understanding the DTAA between India and the UK is very important. It not only avoids double taxation but also provides significant tax benefits to the taxpayer. Proper documentation, such as a valid TRC, Form 10F, is vital to claim these benefits. However, one must understand its provisions to maximize the benefits, which may seem complex to some.

Given its complexity, seeking help from the experts at Savetaxs can be a wise decision. We have an entire team of experts who can help you understand and claim the DTAA to maximize your benefits. Our team can help you enjoy the process with utmost convenience, accuracy, and peace of mind. Contact us anytime, as we are working around the clock globally to help you resolve all your tax queries.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784884591623.webp&w=828&q=75)

_1784883440506.webp&w=828&q=75)

Ans:DTAA covers various types of income, such as:

Ans: The DTAA can be classified depending on the number of countries involved: