NRI Income Tax & Compliance

What Is Section 54B Of The Income Tax Act?What Is Section 54B Of The Income Tax Act?

Written by Hatim Dudhiyawala

When discussing international taxes, the India-Singapore Double Taxation Avoidance Agreement (DTAA) has had a significant impact. The Government of India has signed a Double Tax Avoidance Agreement (DTAA) with Singapore to help taxpayers avoid being taxed twice on their foreign income. This is primarily beneficial for Indian business owners planning to expand their businesses and individuals earning income abroad. Under DTAA, taxes paid in one country can be credited in another, ensuring tax is effectively paid in only one country.

This agreement applies to taxpayers residing in either India, Singapore, or both. India has signed a similar agreement with nearly 100 other countries. The DTAA between India and Singapore benefits both nations regarding tax benefits and promotes economic growth. In this blog, we will discuss everything about the DTAA treaty between India and Singapore. Additionally, we will explore its effectiveness in various aspects.

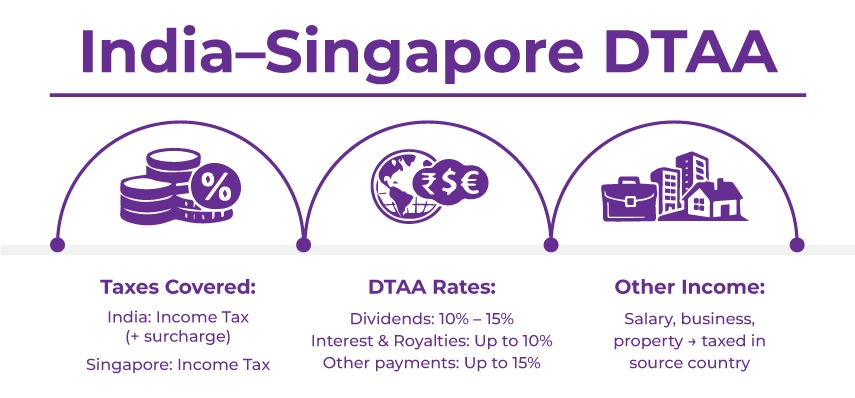

The DTAA between India and Singapore aims to prevent double taxation on income sourced from these countries, thereby eliminating the tax burdens for residents of both these nations. This agreement was signed in 1994 and last amended in 2017. According to the latest amendment, it comprises the Multilateral instruments of the OECD (The Organization for Economic Cooperation and Development). According to this treaty, a Singapore resident earning income in India is eligible to enjoy the same tax treatment as Indian residents earning income from India.

The DTAA also alleviates various types of taxes on income, such as royalties, interest, or fees for technical services, making it easier for all Singapore-based businesses to invest in India by reducing the overall tax liability or earnings from India. Additionally, the DTAA between India and Singapore has facilitated improvements in investment and trade relations between the two countries. Singapore is one of the largest foreign investors in India, with significant investments in various sectors, including infrastructure, real estate, and finance. This treaty facilitates stable and predictable economic growth. India has signed the DTAA with several other countries, including the India-USA DTAA.

The importance of the India-Singapore DTAA depends on its improvement of international relations and growth in trade and investments. By preventing double taxation, Singaporean investors can invest comfortably in Indian companies or establish their company branches in India.

Furthermore, the DTAA between India and Singapore also helps prevent tax evasion and facilitate the free flow of trade and commerce. It ensures that individuals from one country are taxed only in their home country, regardless of the source of their income.

This agreement is also crucial for promoting information exchange and cooperation between the tax authorities of both countries, thereby helping to prevent tax evasion and enforce tax regulations in both countries. Taxpayers from either nation can also benefit from lower TDS rates, tax credits, and exemptions.

Concerning tax rates, several different income sources are subject to withholding tax. For example, Singapore shareholders receiving dividends from Indian companies are subject to a 15% tax on gross dividend income. In comparison, dividends paid by Singaporean corporations to Indian residents are taxed at a maximum of 10% in Singapore. A maximum withholding tax of 10% applies to interest and royalties from an Indian resident to a Singaporean resident. Additionally, a maximum rate of 15% applies to payments made by a Singaporean resident to an Indian resident.

Other types of income, including gains from immovable properties, shipping or airline profits, business profits, employment income, and government payments, are typically taxed in the country of origin.

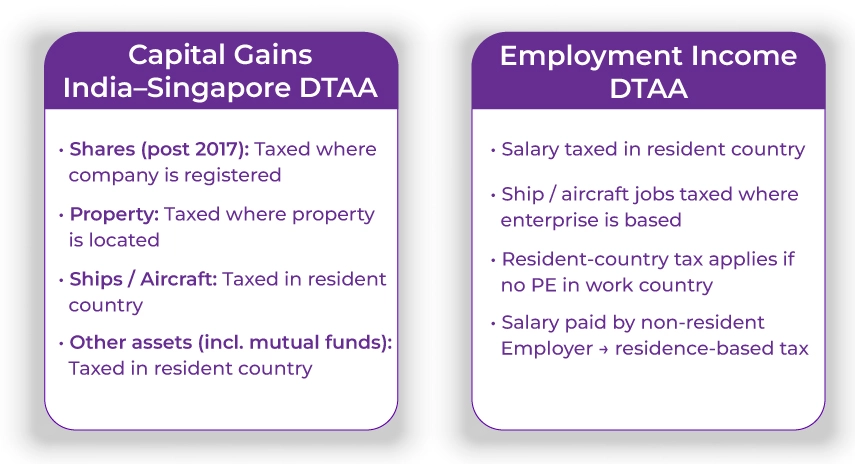

Article 13 of the DTAA between India and Singapore contains the provision for taxation of capital gains. The following are the provisions:

Point to Note: Since mutual fund units are considered as other assets, rather than shares, they are subject to taxation in the country where the assessee is a resident.

The taxation of employment income under the DTAA is governed by Article 15, dealing with the taxation of employment-related income or salary income. It states that remuneration earned by a resident of one country while employed in another country is taxable primarily in the resident's country of residence. Below are the provisions of this tax:

However, the taxation may depend on the taxpayer's country of residence rather than the country where the employment is situated. The following conditions are applied in this scenario:

The DTAA (Double Taxation Avoidance Agreement) between India and Singapore states that income from renting out an immovable property will be taxed in the country where the property is situated.

The India-Singapore DTAA serves as a vital link for enhancing economic ties between the two nations. Both businesses and individuals can benefit from relief from double NRI taxation, which in turn promotes trade and investment. Hence, if you are concerned about your tax responsibilities related to income from Singapore, the DTAA provisions will help you in achieving fair taxation on your total income. Try to ask for assistance from the experts at Savetaxs. Their team can help you optimize your tax liabilities and ensure compliance with the treaty provisions. They can help you navigate the complexities of the India-Singapore DTAA easily, saving you from facing any issues.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1782996918646.png&w=828&q=75)

_1782911003992.webp&w=828&q=75)