_1784547039242.webp&w=828&q=75)

NRI Income Tax Compliance

30+ Important Income Tax Terms in India You Need to Know30+ Important Income Tax Terms in India You Need to Know

Written by Shubham Jain

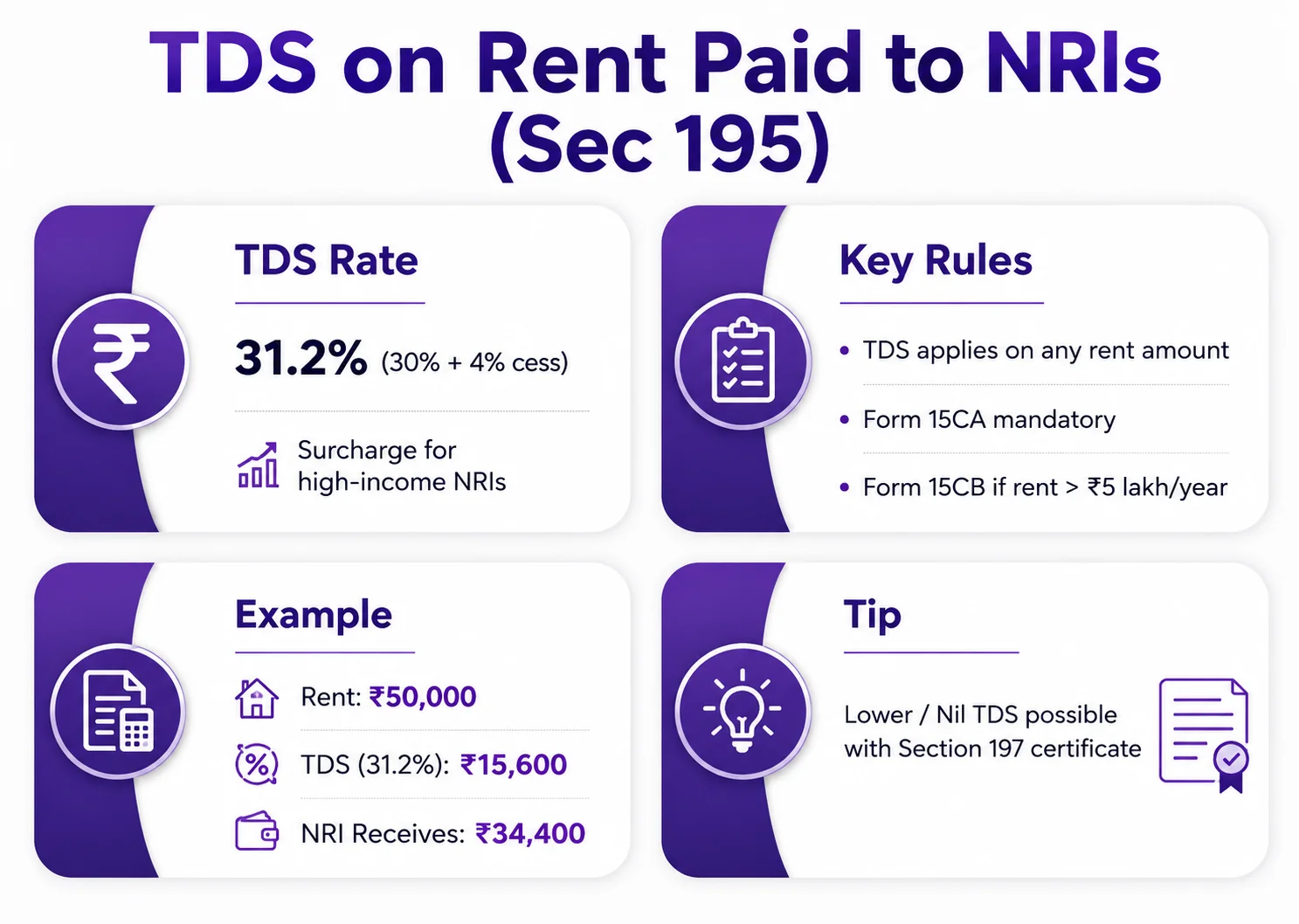

If you are paying rent to an NRI landlord in India, you may be required to deduct TDS under Section 195 of the Income Tax Act. Unlike rent paid to resident landlords, TDS on rent paid to NRIs applies regardless of the rental amount, and non-compliance may attract penalties and prosecution.

In this guide, we explain the applicable TDS rate on rent paid to NRIs, Section 195 rules, Form 15CA/15CB requirements, lower TDS certificates, penalties, exemptions, and return filing requirements for tenants and NRI property owners.

TDS on rent paid to NRI refers to tax deducted at source under Section 195 when a tenant pays rent to a non-resident Indian property owner. The tenant must deduct TDS at applicable rates before paying rent and deposit it with the Income Tax Department.

A person who is of Indian origin or a citizen of India but does not qualify as a resident under Section 6 of the Income Tax Act is considered an NRI.

A person is treated as a resident if they meet either of the following:

Anyone who does not meet these criteria is an NRI.

The residential status of an individual directly impacts the applicability of TDS on rental income under Indian tax laws.

Under Section 195, tenants who pay rent to an NRI landlord must deduct TDS at the applicable rates.

✔ The standard TDS rate on rent paid to NRIs generally starts at 31.2% (including cess).

However, a surcharge may apply if the total Indian income exceeds the surcharge thresholds.

High-income NRIs may face a higher effective TDS rate if surcharge becomes applicable based on their total taxable income in India.

✔ Key Rules

Example:

Rent = ₹50,000/month

TDS = ₹15,600

Landlord receives = ₹34,400

| Particulars | Resident Landlord | NRI Landlord |

|---|---|---|

| Applicable Section | Section 194IB | Section 195 |

| TDS Rate | 5% | 31.2% + applicable surcharge |

| TAN Requirement | Not Mandatory | Mandatory |

| Threshold Limit | ₹50,000/month | No minimum threshold |

| TDS Return Form | Form 26QC | Form 27Q |

The TDS is generally deducted on the gross rent amount before making payment to the NRI landlord.

✔ Tenant must obtain a TAN (Tax Deduction and Collection Account Number).

(TAN is compulsory for NRI rent TDS, unlike resident rent TDS under Section 194-IB.)

✔ Steps:

Example

Rent = ₹8,000/month

TDS = ₹2,496

Landlord receives = ₹5,504

TDS return filing under Section 195 must be completed quarterly using Form 27Q.

After filing the TDS return, tenants must issue Form 16A to the NRI landlord within 15 days from the due date of filing Form 27Q.

If TDS is not deducted or deposited:

Penalties include:

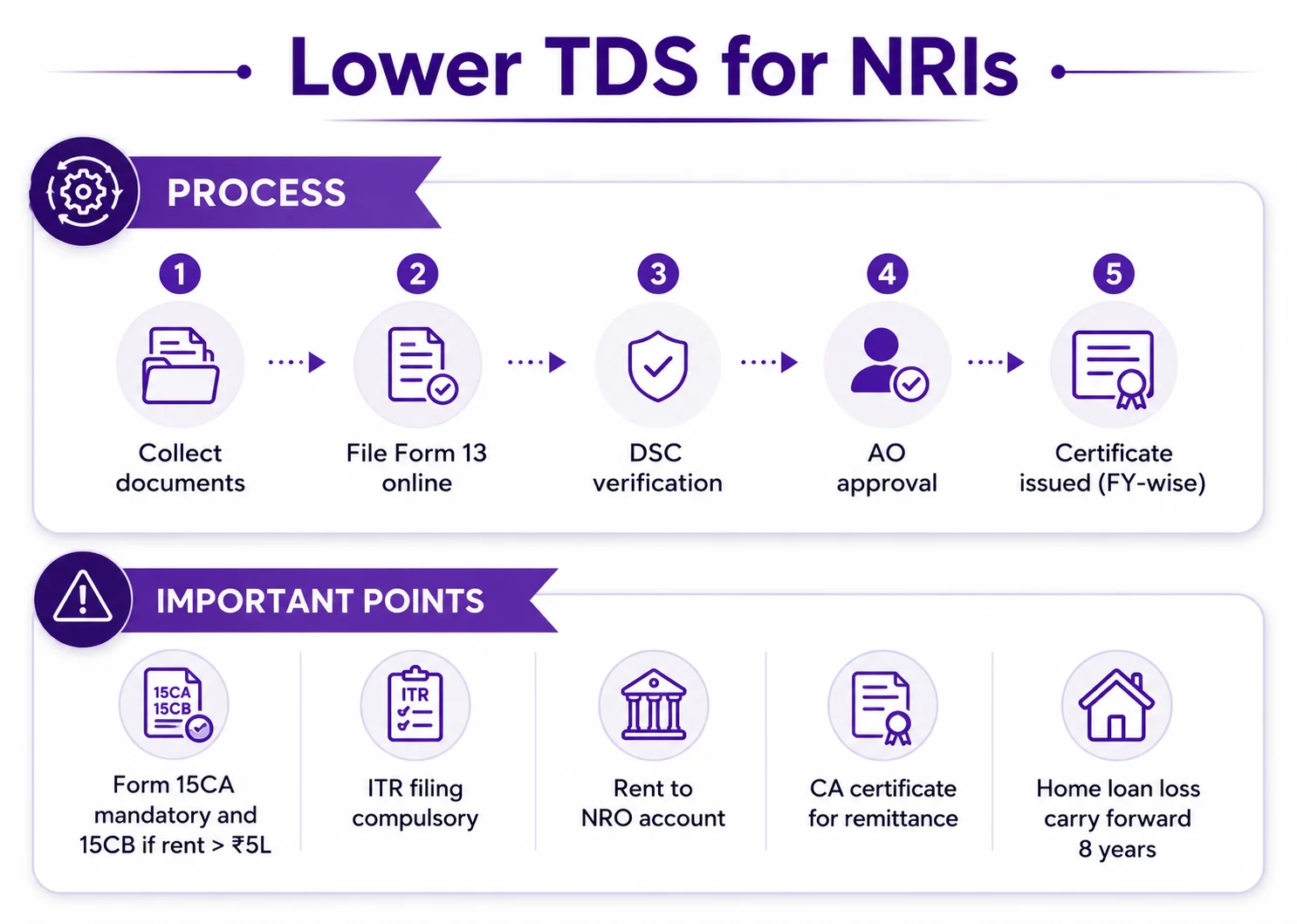

Here are the situations where NRIs may claim lower tax liability or tax relief on rental income earned in India:

More than 90 countries, including the USA, Canada, the UK, and Australia, have DTAA agreements with India.

Under Section 197 of the Income Tax Act, an NRI can apply for a Lower or Nil TDS Certificate that allows tenants to deduct TDS at a reduced or nil rate based on the landlord’s estimated income and tax liability.

If you are renting a property in India, it is important to confirm whether the landlord qualifies as an NRI. This helps ensure proper TDS deduction and compliance with the Income Tax Act.

Understanding the rules for TDS on rent paid to NRIs under Section 195 is important for both tenants and NRI property owners to ensure proper tax compliance and avoid penalties.

To avoid legal issues and penalties, NRI landlords should clearly inform tenants about their NRI status. Tenants should deduct TDS correctly, file the required forms on time, and maintain proper documentation.

Savetaxs offers expert NRI tax filing, TDS compliance, form handling, CA certification, and end-to-end assistance for hassle-free tax management.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784546974133.webp&w=828&q=75)

_1784376356528.webp&w=828&q=75)

_1784375756402.webp&w=828&q=75)