Business Setup

Difference Between a LLP and a Partnership FirmDifference Between a LLP and a Partnership Firm

Written by Hatim Dudhiyawala

_1775566690480.webp&w=3840&q=75)

Directors play a key role in a company. They make strategic decisions, represent the business in the world, and guide operations. However, sometimes things do not work as planned. Due to inactivity, misbehavior, or disagreement, a director is dismissed by the shareholders. Considering this, the process to remove a director from the company is regulated by the Companies Act, 2013. It has to be cautiously undertaken to follow the procedure and the law.

Want to know more about the removal process of the director from the company in detail? The blog contains all the information that you should know about the process, from director types, reasons, legal provisions, and more. So read on and gather all the information.

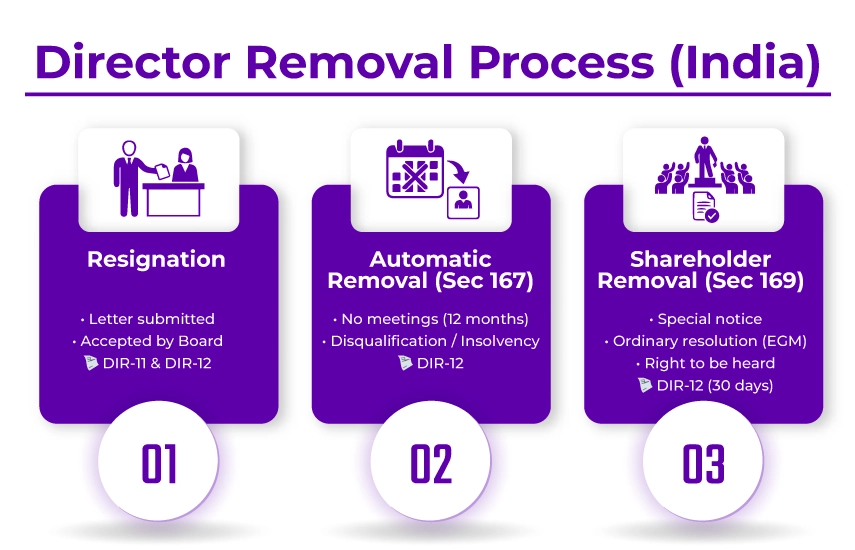

Section 169 of the Companies Act 2013 provides a power to the company to remove a director before the expiry of his term by passing an ordinary resolution. Members who want to remove the director at least 14 days before the meeting need to provide a special notice to the company at which the removal resolution is conducted.

After passing the resolution, the company should fill out Form DIR-12 with the Ministry of Corporate Affairs for the removal of the director.

This was all about the director's removal under the company law. Moving ahead, let's know the grounds to remove a director from the company.

Varying from company to company, here are some of the grounds upon which a director can be removed from their position:

These are some of the key reasons to remove a director from the company. Moving forward, let's know the types of directors who can be removed from their positions.

Here are the different types of directors who can be removed from their position:

Further, a director appointed by the Tribunal or under proportional representation under section 169 of the Companies Act, 2013, cannot be removed.

This was all about the different types of directors who can be removed from a company. Moving further, let's know the process to remove a director from the company.

The process to remove a director from the company can be done in three different ways. These are as follows:

When the director of the company voluntarily tendered his/her resignation.

Under this, the director automatically vacated the company in case of:

When shareholders under section 169 decided to remove a director from their position:

Further, once the ROC updates the records of the company, the name of the director is officially removed from the MCA database. Additionally, the process remains the same to remove an NRI director from the company in India.

These are the three methods for removing a director from a company. Moving ahead, let's know the compulsory criteria that you need to follow for director removal.

To remove a director from a company, you need to fulfill the following mandatory requirements:

This is the checklist you need to follow when removing a director from their position in the company. Moving forward, now, let's look at the consequences of non-compliance in the removal of directors.

Consequences of non-compliance with the stated legal procedure to remove the director include:

These are some of the consequences the company may face when non-compliant in the removal of a director from a company.

For smooth business operations in India, Savetaxs provides expert consultancy to NRIs.

Lastly, from the above blog, it is clear that to remove a director from a company, you need to follow legal procedures stated in the Companies Act, 2013, or relevant local regulations. Additionally, it is an important decision that demands strict compliance and careful consideration of the legal processes. Considering this, whether it includes a board resolution, ordinary resolution, or court order, the process should be transparent, fair, and align with the best interests of the company.

Further, at Savetaxs, we assist NRIs in navigating the director removal process in India. From legal consultation to director removal, our end-to-end service covers every step. We ensure a stress-free experience tailored to your business needs.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1780491123033.webp&w=828&q=75)

_1778757638178.webp&w=828&q=75)