_1784547039242.webp&w=828&q=75)

NRI Income Tax Compliance

30+ Important Income Tax Terms in India You Need to Know30+ Important Income Tax Terms in India You Need to Know

Written by Shubham Jain

_1756729655.webp&w=3840&q=75)

A Hindu Undivided Family (HUF) is one of the most powerful yet underutilised tax-saving structures available to Indian families under the Income Tax Act, 1961. Whether you earn a salary, run a business, or hold ancestral property, forming an HUF can help you legally split income, claim extra deductions, and reduce your overall tax burden — all without any complicated registration.

In this comprehensive guide, we explain everything about a Hindu Undivided Family — from HUF meaning and HUF full form to step-by-step formation, tax benefits, income sources, dissolution, and common mistakes to avoid. If you have ever wondered "what is HUF" or "how does an HUF save tax," this article is written specifically for you.

A Hindu Undivided Family, commonly known by its abbreviation HUF, is a separate legal and taxable entity recognised under Indian law. It consists of all persons who are lineally descended from a common ancestor, together with their wives and unmarried daughters.

The concept of HUF originates from traditional Hindu personal law and the Mitakshara school of Hindu jurisprudence. However, for tax purposes, the Income Tax Act, 1961 treats an HUF as a distinct "person" under Section 2(31). This means it can earn income, own property, open bank accounts, make investments, and file its own income tax return — completely independent of its individual members.

In simple terms, think of an HUF as a family unit that functions like a separate taxpayer. Just as a company has its own PAN, bank account, and tax return, an HUF operates in a similar manner — but without the need for formal registration under any company law.

This is precisely what makes the Hindu Undivided Family such a valuable tax-planning tool. By routing certain income streams through the HUF instead of individual returns, families can legally reduce their aggregate tax liability.

The HUF full form is Hindu Undivided Family.

Under Section 2(31) of the Income Tax Act, 1961, an HUF is classified as a "person" for the purpose of taxation. The Act does not define HUF directly; instead, it derives its meaning from Hindu personal law.

According to Hindu law, a Hindu Undivided Family is a family that:

A critical point to note is that an HUF is not limited to Hindus alone. Under the Income Tax Act, Jains, Sikhs, and Buddhists can also form a Hindu Undivided Family and avail of all associated tax benefits. This is because these religions are governed by Hindu personal law for matters of succession and family property.

Understanding the distinctive characteristics of an HUF helps clarify how it differs from other taxable entities:

Automatic Formation: An HUF comes into existence automatically upon the marriage of a Hindu individual or the birth of a child. Unlike a company or partnership firm, no formal registration is required for its creation.

Separate Legal Entity: For income tax purposes, an HUF is treated as a separate person, distinct from its individual members. It has its own PAN, bank account, and tax assessment.

Ancestral and Self-Acquired Property: An HUF can hold both ancestral property (inherited from forefathers) and self-acquired property (contributed or gifted by members). Income from these assets is taxed in the hands of the HUF, not the individual members.

Perpetual Succession: An HUF does not dissolve upon the death of a member. It continues to exist through successive generations until it is formally partitioned.

Managed by Karta: The senior-most coparcener of the HUF acts as the Karta (manager) who has the authority to manage the HUF's affairs, enter into contracts, and make financial decisions on behalf of the family.

No Maximum Member Limit: There is no restriction on the number of members in an HUF. As the family grows through births and marriages, the HUF expands naturally.

Any Hindu family can form an HUF, provided there are at least two members — typically a married couple. However, it is important to understand the eligibility criteria clearly:

Religions Eligible to Form an HUF: An HUF can be formed by families following Hinduism, Jainism, Sikhism, or Buddhism. These religions fall under the umbrella of Hindu personal law, which governs the concept of joint family property.

Minimum Requirement: At the bare minimum, a married Hindu individual can create an HUF with their spouse. With the birth of a child, the HUF gains its first coparcener by birth.

Who Cannot Form an HUF: Individuals belonging to religions not governed by Hindu personal law — such as Muslims, Christians, Parsis, and Jews — cannot form a Hindu Undivided Family. However, if a Hindu individual marries a non-Hindu, the HUF is still valid; the non-Hindu spouse becomes a member of the HUF (though not a coparcener).

Can a Single Person Have an HUF? No, a single unmarried individual cannot create an HUF. The minimum requirement is a family of at least two members. However, a widowed individual with children can continue an existing HUF.

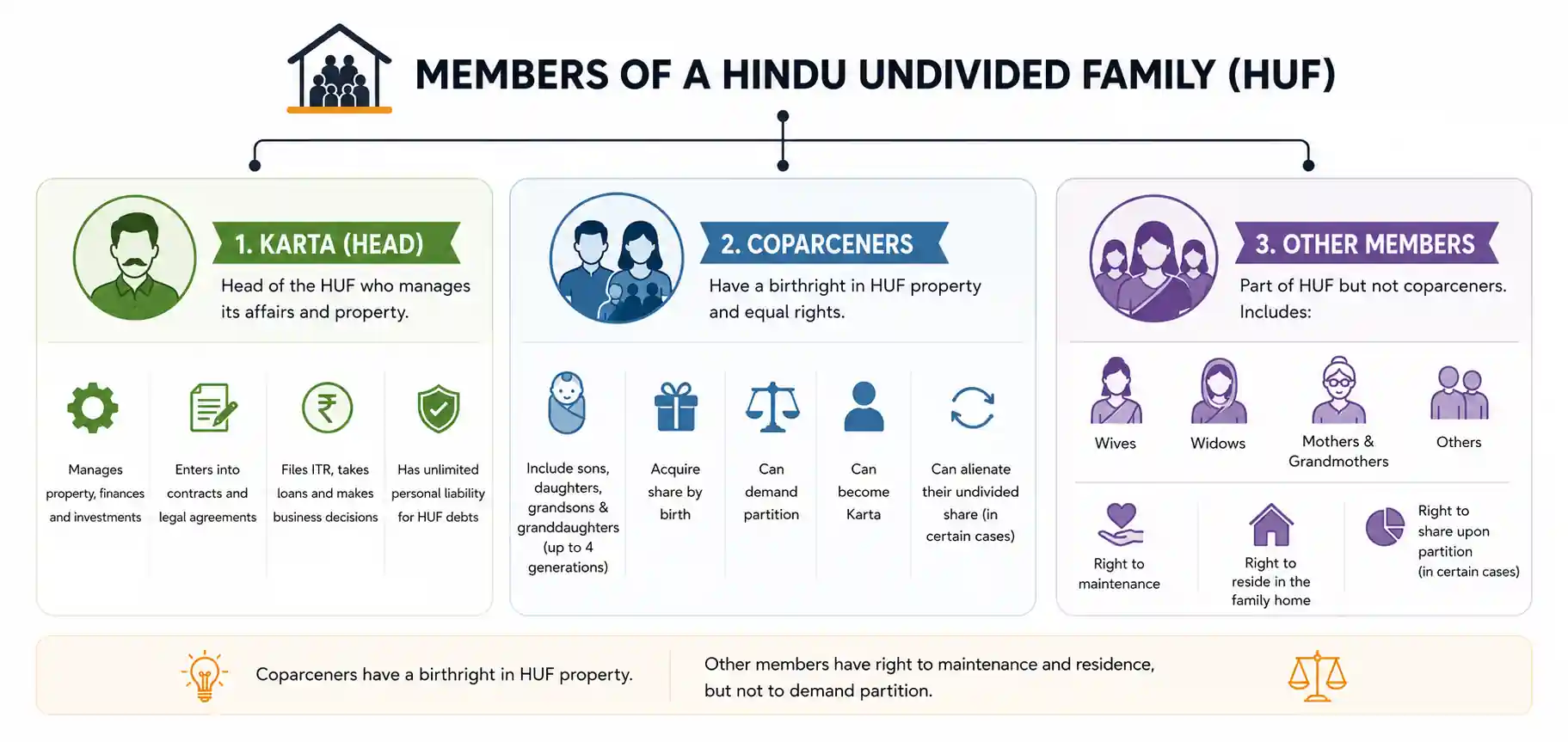

An HUF comprises three categories of members, each with different rights and responsibilities:

The Karta is the head of the Hindu Undivided Family. Traditionally, the senior-most male coparcener served as the Karta. However, following the Hindu Succession (Amendment) Act, 2005, a female coparcener (daughter) can also become the Karta.

Key powers and responsibilities of the Karta include:

The Karta holds a position of immense trust. Unlike a company director who has limited liability, the Karta's personal assets can be attached if the HUF fails to meet its obligations.

Coparceners are members who have a birthright to the property of the HUF. They hold the most significant legal position within the family structure.

After the 2005 Amendment to the Hindu Succession Act, coparceners include:

Rights of coparceners:

Other members include individuals who are part of the HUF but are not coparceners. This category typically includes:

Other members have the following rights:

However, other members do not have the right to demand partition or claim a birthright share in HUF property.

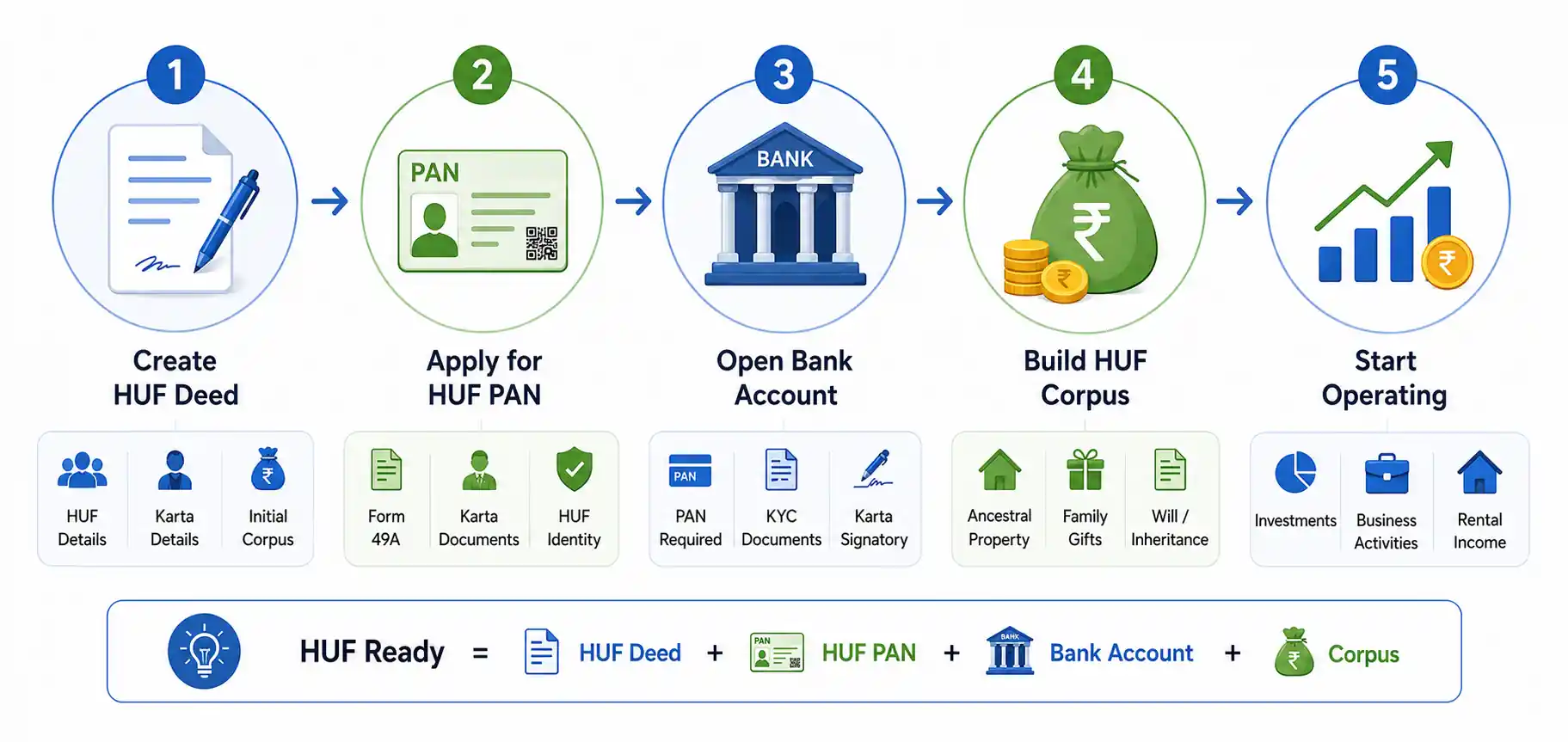

Forming a Hindu Undivided Family is a straightforward process that involves four essential steps:

The first step is to draft a legal document called the HUF Deed (also known as the HUF Declaration). While an HUF exists automatically under Hindu law, a written deed is necessary for official purposes such as obtaining a PAN card and opening a bank account.

The HUF Deed should contain:

The deed should be executed on stamp paper of the requisite value (varies by state) and signed by all adult members.

Every HUF must have its own Permanent Account Number (PAN). You can apply for an HUF PAN using Form 49A through:

Documents required for HUF PAN application:

The PAN card will be issued in the name of the HUF, with the Karta's details mentioned as the representative assessee.

Once the PAN card is obtained, the next step is to open a bank account in the name of the HUF. Visit any bank branch and submit:

The bank account will be operated by the Karta, who will be the primary signatory.

An HUF needs an initial corpus to begin operations. The corpus can be built through:

Important Note on Clubbing: If a member transfers personal funds to the HUF and the HUF earns income from those funds, the income may be clubbed back in the member's hands under Section 64(2) of the Income Tax Act. However, the income earned by the HUF from investing this clubbed income (i.e., income on income) is not clubbed and remains taxable in the HUF's hands.

With the deed, PAN, and bank account in place, the HUF is ready for business. You can:

The primary motivation behind forming a Hindu Undivided Family is tax savings. Since an HUF is treated as a separate taxpayer, it enjoys its own set of exemptions and deductions — over and above what individual members already claim. Here are the major tax benefits:

An HUF is eligible for the same basic exemption limit as an individual taxpayer:

This means if your family routes Rs 2.5 lakh of income through the HUF under the old regime, that entire amount is tax-free — a benefit that would otherwise be unavailable if the income were reported in an individual's return where the basic exemption is already exhausted.

An HUF can independently claim deductions up to Rs 1,50,000 under Section 80C for investments in:

This is a completely separate Rs 1.5 lakh deduction in addition to the Rs 1.5 lakh that each individual member already claims in their personal return.

The HUF can pay health insurance premiums for any of its members and claim a deduction under Section 80D:

This deduction is separate from the individual member's own Section 80D claim.

If the HUF takes a home loan to purchase or construct a property, it can claim a deduction on the interest paid:

The principal repayment qualifies for deduction under Section 80C (within the Rs 1.5 lakh limit).

An HUF can avail of the same capital gains exemptions available to individuals:

Gifts received by the HUF from its members are completely tax-free, regardless of the amount. This is because gifts from "relatives" (as defined under the Income Tax Act) are exempt from tax under Section 56(2)(x).

Additionally, gifts received on the occasion of the marriage of any member, or through inheritance or will, are also fully exempt.

Gifts from non-relatives up to Rs 50,000 in aggregate during a financial year are also exempt.

The most powerful tax advantage of an HUF is income splitting. By distributing family income between the individual returns and the HUF return, the total tax liability of the family can be significantly reduced.

Example:

Suppose Mr Sharma earns Rs 15,00,000 annually. His individual tax liability (old regime) would be approximately Rs 2,62,500 (before cess).

Now, if he forms an HUF and routes Rs 5,00,000 of legitimate income (say, rental income from ancestral property) through the HUF:

Saving: Rs 1,37,500 — a reduction of over 52% in tax outgo, entirely within the legal framework.

Donations made by the HUF to approved charitable organisations qualify for deduction under Section 80G, further reducing the taxable income of the HUF.

An HUF can earn income from multiple sources, just like an individual. The key sources include:

Income from House Property: Rental income from property owned by the HUF. This includes both ancestral property and property purchased using HUF funds.

Profits and Gains from Business or Profession: The HUF can carry on a business in its own name. Profits from such business are taxed in the hands of the HUF.

Capital Gains: Gains arising from the sale of HUF assets — including property, shares, mutual funds, and other investments.

Income from Other Sources: Interest income from bank deposits, dividends from shares, and any other miscellaneous income earned by the HUF.

Important: Salary income cannot be earned by an HUF because salary is personal to an individual. Similarly, income under the head "Income from Salary" cannot be routed through an HUF.

Starting from FY 2023-24, the new tax regime became the default regime for all taxpayers, including HUFs. However, an HUF can opt for the old tax regime if it wishes to claim exemptions and deductions.

Here is how the choice impacts an HUF:

Old Tax Regime:

New Tax Regime:

Which regime should your HUF choose?

If the HUF has investments in Section 80C instruments, pays health insurance premiums, and earns rental income with a home loan, the old regime may result in lower tax. However, if the HUF has limited deductions and the income is primarily from capital gains or business, the new regime's lower slab rates may be more advantageous.

We recommend computing the tax liability under both regimes before filing to determine the optimal choice.

An HUF is taxed at the same slab rates as an individual (non-senior citizen for the new regime, and age-based for the old regime if the Karta qualifies as a senior citizen).

| Taxable Income | Tax Rate |

|---|---|

| Up to Rs 2,50,000 | Nil |

| Rs 2,50,001 – Rs 5,00,000 | 5% |

| Rs 5,00,001 – Rs 10,00,000 | 20% |

| Above Rs 10,00,000 | 30% |

Rebate under Section 87A: If the total income does not exceed Rs 5,00,000, the tax payable is nil (rebate of up to Rs 12,500).

| Taxable Income | Tax Rate |

|---|---|

| Up to Rs 4,00,000 | Nil |

| Rs 4,00,001 – Rs 8,00,000 | 5% |

| Rs 8,00,001 – Rs 12,00,000 | 10% |

| Rs 12,00,001 – Rs 16,00,000 | 15% |

| Rs 16,00,001 – Rs 20,00,000 | 20% |

| Rs 20,00,001 – Rs 24,00,000 | 25% |

| Above Rs 24,00,000 | 30% |

Health and Education Cess of 4% applies on the total tax amount under both regimes.

The ITR form for an HUF depends on the nature and sources of its income:

HUFs are not eligible to file ITR-1 (Sahaj) as this form is restricted to individual resident taxpayers with total income up to Rs 50 lakh.

The due date for filing the HUF's return is 31st July of the assessment year (same as individuals), unless the HUF is required to get its accounts audited, in which case the due date extends to 31st October.

Understanding how an HUF compares with other entities helps in choosing the right structure:

| Parameter | HUF | Individual | Partnership Firm |

|---|---|---|---|

| Formation | Automatic (by birth/marriage) | By birth | By agreement (partnership deed) |

| Legal Status | Separate taxable entity | Natural person | Separate taxable entity |

| PAN Required | Yes (separate HUF PAN) | Yes | Yes |

| Tax Slabs | Same as individual | Individual slabs | 30% flat rate |

| Basic Exemption | Rs 2.5L (old) / Rs 4L (new) | Rs 2.5L (old) / Rs 4L (new) | No basic exemption |

| Deductions (80C, 80D) | Available (old regime) | Available (old regime) | Not available |

| Dissolution | Only by partition | Not applicable | By agreement or court order |

| Liability of Head | Karta has unlimited liability | Personal liability | Partners have joint and several liability |

| Succession | Perpetual (continues on death) | Not applicable | May dissolve on partner's death |

| Registration | Not required | Not required | Optional under Partnership Act |

One of the most misunderstood aspects of HUF taxation is the clubbing of income provisions under Section 64(2) of the Income Tax Act.

The Rule: When an individual member transfers personal assets (which are not ancestral) to the HUF without adequate consideration, the income generated from those assets is clubbed back in the hands of the transferring member — not taxed in the HUF's return.

Example: Mr Verma transfers Rs 10,00,000 from his personal savings to his HUF. The HUF invests this amount in a fixed deposit earning Rs 70,000 interest per year. This Rs 70,000 will be clubbed back in Mr Verma's individual return, not in the HUF's return.

The Workaround — Income on Income: If the HUF reinvests the Rs 70,000 interest (the clubbed income) and earns further income from it, this secondary income (income on income) is taxed in the HUF's hands and is not clubbed back. Over time, this compounding effect creates a growing corpus of legitimately HUF-owned income.

How to Avoid Clubbing Issues:

While an HUF offers significant tax benefits, it is not without its drawbacks:

Equal Rights of All Coparceners: All coparceners have equal rights to HUF property. As the family grows, managing these rights becomes increasingly complex and can lead to disputes.

Difficult to Dissolve: Closing an HUF (partition) requires the consent of all coparceners. If even one coparcener disagrees, the partition may need to be pursued in court, which can be a long and expensive process.

Unlimited Liability of the Karta: The Karta bears unlimited personal liability for all debts and obligations of the HUF. If the HUF takes a loan and defaults, the Karta's personal assets can be seized.

Clubbing Provisions: As discussed above, income from assets transferred by individual members may be clubbed back, reducing the tax benefit.

No Customization in Holding Pattern: Unlike a company where shareholding can be customized, all coparceners hold an equal undivided share in the HUF property. You cannot allocate a larger share to a specific member.

Family Disputes: Joint ownership of assets can create friction, especially during significant financial decisions or when a member wishes to separate.

Limited Corpus Initially: A newly formed HUF typically starts with a small corpus. Building it up takes time, and the tax benefits are proportional to the HUF's income.

Inter-Religious Marriage Complications: If a Hindu coparcener marries a non-Hindu, the non-Hindu spouse becomes a member but not a coparcener. This can create complexities in the HUF's structure and in determining rights.

An HUF can be dissolved through a process called partition. Partition results in the division of HUF property among the coparceners, after which the HUF ceases to exist (in the case of total partition).

A total partition occurs when the entire HUF property is divided among all coparceners. After a total partition:

For a total partition to be recognized by the Income Tax Department, the Karta must apply to the Assessing Officer under Section 171 of the Income Tax Act. The Assessing Officer will conduct an inquiry and record the partition.

A partial partition occurs when only some members separate from the HUF, or only a portion of the HUF property is divided.

Important Note: Under Section 171(9), partial partitions of an HUF effected after 31st December 1978 are not recognised for income tax purposes. This means the Income Tax Department will continue to treat the HUF as undivided and tax the entire income in the hands of the HUF, even if a partial partition has taken place under Hindu law.

Tax Implications on Partition:

There is no capital gains tax on the partition of an HUF. The transfer of assets from the HUF to coparceners upon partition is not treated as a "transfer" under Section 47(i) of the Income Tax Act. However, when the coparcener subsequently sells the asset received on partition, the cost of acquisition for capital gains purposes is the cost at which the HUF originally acquired the asset.

Yes, a daughter can be the Karta of a Hindu Undivided Family.

Following the Hindu Succession (Amendment) Act, 2005, daughters have been granted equal coparcenary rights as sons. Since they are now coparceners by birth, they are eligible to become the Karta of an HUF.

This was further affirmed by the Supreme Court of India in the landmark judgement of Vineeta Sharma vs Rakesh Sharma (2020), where the Court held that the coparcenary rights of daughters are by birth and are not contingent on the father being alive on the date the Amendment came into effect (9th September 2005).

In practice, however, the Karta is traditionally the senior-most coparcener. If a daughter is the eldest coparcener, she can assume the role of Karta and manage the HUF's affairs.

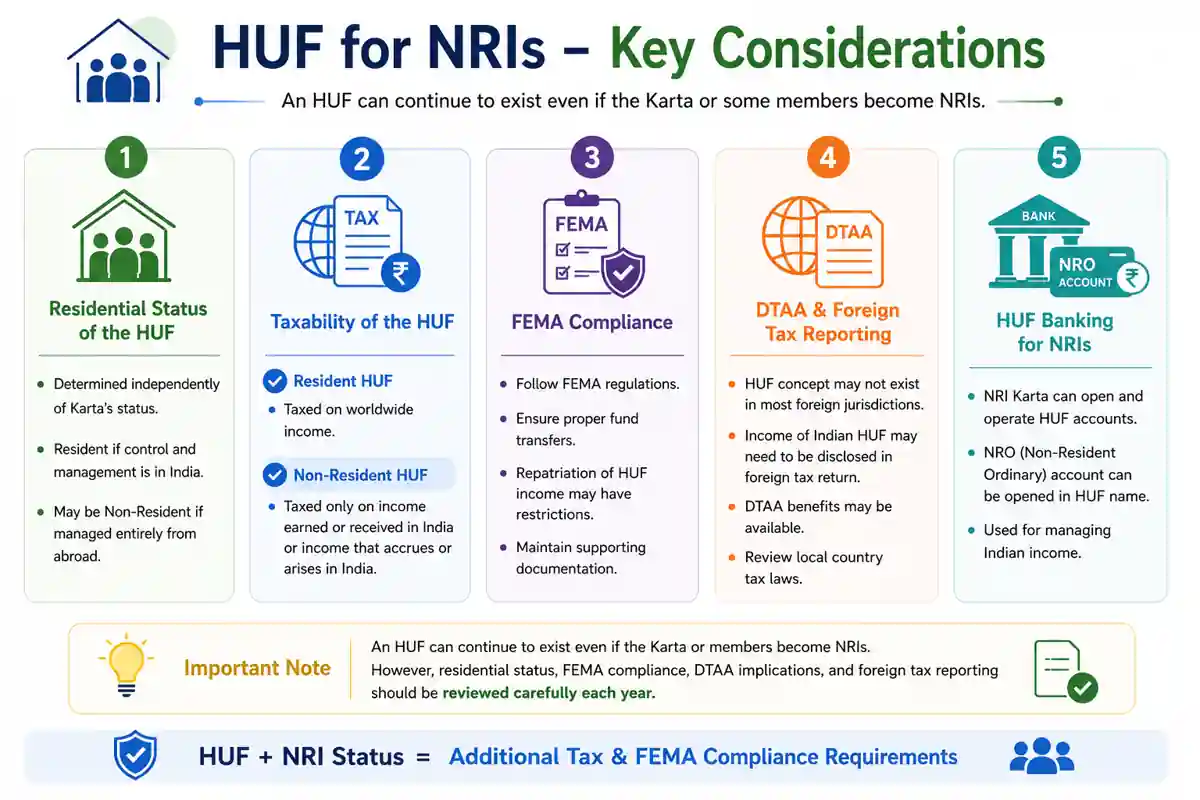

Non-Resident Indians (NRIs) can have an HUF in India, and the HUF continues to exist even if the Karta or some members become NRIs. However, there are specific tax and compliance considerations:

Residential Status of the HUF: The residential status of an HUF is determined independently — it is not automatically the same as the Karta's status. An HUF is considered a resident if the control and management of its affairs is situated wholly or partly in India. If the Karta manages the HUF from abroad, the HUF may be treated as a non-resident.

Taxability: A resident HUF is taxed on its worldwide income. A non-resident HUF is taxed only on income earned or received in India, or income that accrues or arises in India.

FEMA Compliance: NRIs need to ensure compliance with the Foreign Exchange Management Act (FEMA) when transferring funds to or from the HUF. Repatriation of HUF income outside India may have restrictions.

Double Taxation: If the NRI Karta is a tax resident of another country (such as the USA), there is no concept of HUF in most foreign jurisdictions. The income of the Indian HUF may need to be disclosed in the foreign country's tax return, depending on the local tax laws and the applicable Double Taxation Avoidance Agreement (DTAA).

Bank Account: An NRI Karta can open an NRO (Non-Resident Ordinary) bank account in the name of the HUF to manage Indian income.

Many families form an HUF but fail to manage it correctly, leading to tax disputes and lost benefits. Here are the most common mistakes:

Not Creating a Written HUF Deed: While an HUF exists by operation of law, not having a written deed creates problems when applying for PAN or opening a bank account. Always document the HUF formally.

Mixing Personal and HUF Funds: The HUF must maintain a separate bank account. Never co-mingle personal funds with HUF funds. Every transaction should be clearly identifiable as belonging to the HUF.

Ignoring Clubbing Provisions: Transferring large amounts of personal income to the HUF without understanding Section 64(2) can result in the income being clubbed back in the individual's return, defeating the purpose.

Not Filing the HUF's Income Tax Return: Even if the HUF's income is below the taxable limit, filing a nil return is advisable. It creates a paper trail and establishes the HUF's existence with the Income Tax Department.

Failing to Update the HUF Deed: When new members are born, or members pass away, the HUF Deed should be updated to reflect the current composition.

Choosing the Wrong Tax Regime: Blindly opting for the new tax regime without calculating the impact of foregone deductions can result in higher tax for the HUF.

Not Maintaining Proper Books of Account: If the HUF carries on a business, it must maintain books of account under Section 44AA. Failure to do so may result in penalties.

Assuming All Family Income Can Be HUF Income: Only income from HUF-owned assets or HUF business is legitimate HUF income. You cannot simply reclassify personal salary or freelancing income as HUF income.

The Hindu Undivided Family is a time-tested and legally robust tax-planning structure that every Hindu, Jain, Sikh, and Buddhist family in India should consider. By creating a separate taxable entity within the family, an HUF allows you to claim an additional basic exemption, extra deductions, and legally split income — resulting in substantial tax savings year after year.

However, forming an HUF is just the beginning. The real benefits come from disciplined management — maintaining separate accounts, choosing the right tax regime, investing wisely through the HUF, and keeping proper documentation.

If you are unsure whether an HUF is right for your family, or if you need help forming one, consult a qualified Chartered Accountant or tax advisor who can assess your specific situation and guide you through the process.

Disclaimer: This article is intended for informational and educational purposes only. It does not constitute legal or tax advice. Tax laws are subject to change, and you should consult a qualified professional before making any financial decisions based on this content.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784546974133.webp&w=828&q=75)

_1784376356528.webp&w=828&q=75)

_1784375756402.webp&w=828&q=75)