_1784624542261.png&w=828&q=75)

NRI Income Tax Compliance

7 Mistakes That Could Trigger an Income Tax Notice for salaried employees7 Mistakes That Could Trigger an Income Tax Notice for salaried employees

Written by Shubham Jain

_1767003468.png&w=3840&q=75)

An NRI (Non-Resident Indian) is an Indian citizen living outside India for employment, business, education, or other long-term purposes and qualifying as a non-resident under Indian laws. NRI status affects Taxation in India, Banking and investments, Property ownership, FEMA compliance, Repatriation of funds.

If you are moving abroad or already settled overseas, understanding NRI rules is important for managing taxes, investments, and bank accounts correctly.

An NRI refers to an Indian citizen residing outside India for:

Even while living abroad, many NRIs continue maintaining financial ties with India through:

This is why understanding NRI taxation and compliance becomes important.

NRI status is determined under:

The Income Tax Act mainly considers the number of days stayed in India, while FEMA also considers the purpose and intention of staying abroad.

Under Section 6 of the Income Tax Act, an individual becomes a Resident Indian if:

If these conditions are not satisfied, the individual generally qualifies as an NRI.

Certain Indian citizens and Persons of Indian Origin (PIOs) may also be covered under the modified 120-day rule if their Indian income exceeds prescribed limits.

Example

Rahul moved to the USA for employment and stayed in India for only 105 days during the financial year. Since he did not satisfy the residency conditions, he generally qualifies as an NRI for that year.

Under FEMA regulations, residential status mainly depends on:

An individual generally becomes an NRI under FEMA if they move abroad for:

This distinction becomes important for:

| Feature | NRI | OCI | PIO |

|---|---|---|---|

| Citizenship | Indian Citizen | Foreign Citizen | Foreign Citizen |

| Passport | Indian Passport | Foreign Passport | Foreign Passport |

| Voting Rights | Yes | No | No |

| Property Purchase | Allowed except agricultural land | Same as NRI | Same as NRI |

Although these categories are often used interchangeably, they have different legal and taxation implications.

NRIs receive several banking and taxation benefits under Indian regulations.

Interest earned on:

is generally tax-free in India while maintaining valid NRI status.

DTAA agreements also help NRIs avoid double taxation on the same income.

NRIs can invest in:

subject to FEMA, RBI, and SEBI regulations.

Funds held in:

are fully repatriable outside India.

NRO balances may generally be repatriated up to USD 1 million annually after prescribed tax formalities.

NRIs can generally invest in:

However, NRIs are generally restricted from purchasing:

Certain small savings schemes may also have restrictions for NRIs.

One of the first things NRIs should do after moving abroad is redesignate resident savings accounts into proper NRI accounts.

An NRE (Non-Resident External) account is used to deposit foreign income in India.

Key Features

NRIs earning income outside India.

An NRO (Non-Resident Ordinary) account is used for managing Indian-source income such as:

Key Features

NRIs receiving income from India.

An FCNR (Foreign Currency Non-Resident) account allows NRIs to maintain deposits in foreign currency.

Key Features

Many NRIs unintentionally create compliance issues because they are unaware of changing regulations after moving abroad.

Common mistakes include:

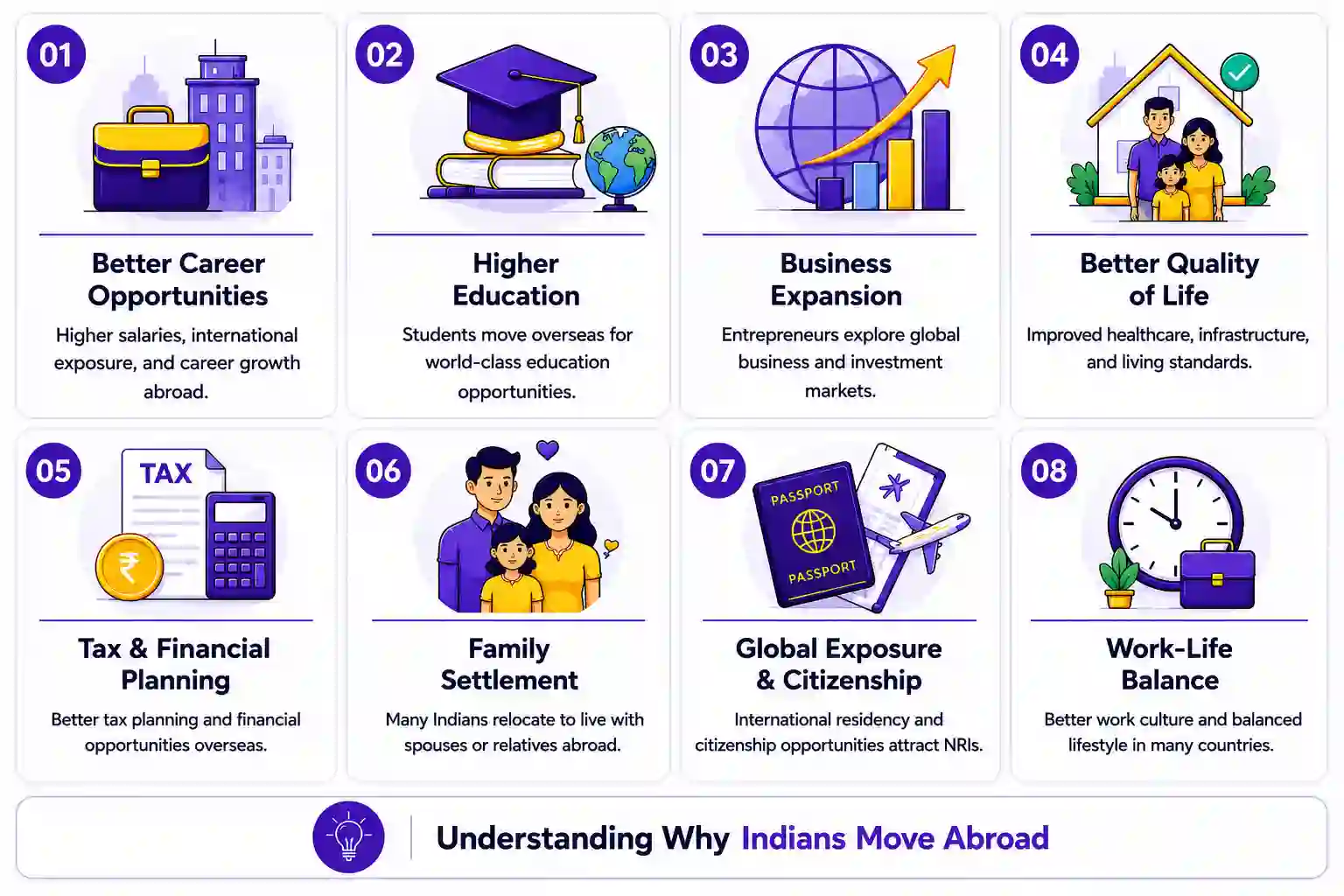

People become NRIs for several personal and professional reasons.

Many professionals move abroad for:

Students pursuing international education often become NRIs during their long-term stay abroad.

Entrepreneurs may relocate overseas to expand businesses or access international markets.

Some individuals move abroad to join spouses or family members settled overseas.

Many NRIs relocate for:

NRIs are generally taxed in India only on:

Foreign income earned and received outside India is generally not taxable in India for NRIs.

The following income is generally taxable in India for NRIs:

However:

| Income Type | Taxable in India? |

|---|---|

| Salary earned abroad | Generally No |

| Salary earned in India | Yes |

| Rental income from Indian property | Yes |

| Capital gains from Indian assets | Yes |

| NRE account interest | Generally No |

| FCNR deposit interest | Generally No |

| NRO account interest | Yes |

| Income Range | Tax Rate |

|---|---|

| Up to ₹3,00,000 | Nil |

| ₹3,00,001 – ₹7,00,000 | 5% |

| ₹7,00,001 – ₹10,00,000 | 10% |

| ₹10,00,001 – ₹12,00,000 | 15% |

| ₹12,00,001 – ₹15,00,000 | 20% |

| Above ₹15,00,000 | 30% |

Additional surcharge and cess may apply depending on taxable income.

DTAA (Double Taxation Avoidance Agreement) is a treaty signed between India and another country to prevent the same income from being taxed twice.

DTAA helps NRIs:

To claim DTAA benefits, NRIs may require:

RNOR (Resident but Not Ordinarily Resident) is a transitional residential status available to certain returning NRIs.

This status may provide temporary tax relief because certain foreign income can remain exempt from Indian taxation during the transition period.

RNOR planning is particularly important for returning NRIs with:

This article is based on:

Understanding NRI status is essential for managing taxation, banking, investments, and financial compliance across countries.

From selecting the right NRI account to understanding DTAA benefits and taxation rules, proper planning can help NRIs avoid compliance issues and manage finances more efficiently.

Whether you recently moved abroad or have been living overseas for years, staying informed about NRI regulations can help you make smarter financial decisions in both India and your country of residence.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784624729370.webp&w=828&q=75)

_1784547039242.webp&w=828&q=75)

_1784546974133.webp&w=828&q=75)