_1771419038394.webp&w=828&q=75)

Difference Between Luxury Real Estate and Traditional Investment

Read More

_1777034893472.webp&w=3840&q=75)

The Indian market offers multiple investment avenues, mutual funds, real estate, equities, and more to NRIs. But when it comes to steady returns with minimal risk, bond investments for NRIs are a good option. In light of this, on April 1, 2020, the government of India introduced the Fully Accessible Route (FAR). It allows NRIs without any investment ceiling to invest in certain government bonds.

To help you out, this blog provides all the aspects that one needs to know about NRI bonds in India. So let's gather all the information about it.

Key Takeaways

NRI bonds refer to debt instruments in which NRIs put their money. These include public sector bonds, government securities, corporate bonds, and other fixed-income products.These investments are generally considered low to moderate risk and provide relatively stable and fixed income returns.

Under this, when you buy a bond, you pay money to the government-linked companies (PSUs). When the loan is paid off (maturity), along with your investment amount, you receive some interest income. Furthermore, compared to high-risk investments like equities, NRI bonds offer more stable but relatively moderate returns.

This was all about NRI bonds. Moving ahead, let's know whether NRIs can also invest in bonds in India.

Yes, NRIs are allowed to invest in Indian bonds. With the introduction of the Fully Accessible Route (FAR) on April 1, 2020, the Indian government permitted NRIs to purchase certain government bonds. This helps NRIs to buy government bonds as per their desire.

However, not all bonds are available for NRIs for investment in India. Considering this, let's know in the next sections what bonds are available for NRI investments in India.

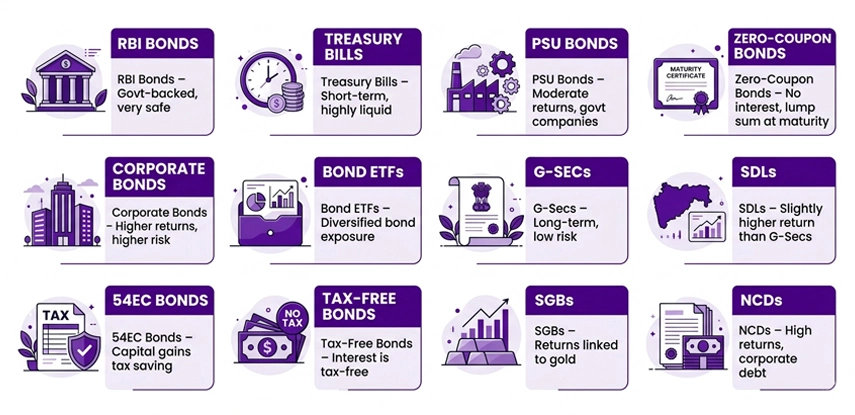

Here is the list of different types of bonds NRIs can invest in India:

These bonds are issued by the Reserve Bank of India. These are savings bonds backed by the government of India. The RBI bonds offer investors a stable and steady source of income.

The Indian government issues treasury bills for borrowing money for a limited period. It is a safe option for NRIs to keep their additional money safe for a short time. Also, treasury bills are on sale for less than their original price.

Government-owned companies such as REC, NHAI, IRFC, and PFC issue PSU Bonds. These bonds receive funding for large infrastructure and public sector projects. PSU bonds are relatively safe when highly rated and generally offer moderate returns depending on market conditions

These bonds are sold for less than their face value, and you get paid at face value. Considering this, Zero-Coupon bonds do not pay regular interest. However, when they mature, they do offer a lump sum amount. This investment option is ideal for NRI investors who aim to earn long-term returns.

These bonds are issued by infrastructure and private companies. To invest in these bonds, NRIs need to follow specific rules. These funds help in the growth of business and infrastructure development.

With bond Exchange-Traded Funds (ETFs), with a single investment, you get access to a group of bonds. It is because these ETFs invest in bonds issued by the public sector and government entities.

The Indian government, to finance its infrastructure and other needs, issues marketable, long-term bonds known as Government Securities. These are one of the safest investment options available in India.

These are bonds that are issued by the state government to fund infrastructure and development initiatives at the state level. They generally pay a little more return than central government bonds.

Certain government agencies issue Section 54EC Capital Gain Bonds. These are tax-saving bonds that let investors save their money on taxes when they sell property for a long time.

Under the tax-free bonds, you are not liable to pay tax on the earned interest. These are not issued anymore. Considering this, investors still trade in older bonds. These bonds push for long-term funding for infrastructure.

These were government bonds connected to gold. These were issued to lower the physical demand for gold.

These bonds are issued by companies as long-term loan instruments that do not turn into shares. The NCD bonds help businesses to get money for a long time.

These are the different types of bonds for NRIs in India. These offer varied levels of returns, risks, and time lengths. Additionally, from time to time, the bond rules can be modified by the RBI, which may affect eligibility. Apart from this, NRIs, according to their investment choices, can opt for 5-year, 10-year, and long-term bonds.

Now, moving further, let's know the benefits of NRI bonds.

With the expert guidance of Savetaxs, fulfill your tax obligations on time without any hassle.

The key benefits for NRIs to invest in Indian bonds include:

These are some of the benefits of Indian bonds for NRIs. Further, Compared to equity investments, bonds are generally considered safer, though risk levels vary across different debt instruments. Now, moving forward, let's look at the credit ratings of NRI bonds in India.

Credit ratings showcase the possibility that a debenture or bond will offer on its principal and interest payments. The higher the rating, the safer the investment. Considering this, before investing in Indian bonds, NRIs should first verify their ratings from reputable agencies like CARE, CRISIL, or ICRA. To help you out, the table below provides you with an idea of how to check credit ratings.

|

Rating |

Safety Level |

Risk |

|---|---|---|

|

AAA |

Highest |

Lowest |

|

AA |

High |

Very low |

|

A |

Adequate |

Low |

|

BBB |

Moderate |

Moderate |

|

BB/B |

High default risk |

Avoid buying it for safety reasons |

Further, for safer investment returns, purchase AAA and AA-rated bonds. It is especially beneficial when you want to rely on steady interest income or send money home.

Moving ahead, let's know how NRIs can invest in bonds in India.

Here is how NRIs can invest their money in securities or bonds in India:

This is how NRIs can invest in bonds in India. Moving further, let's know how interest from these bonds is taxed in India.

For NRIs, purchasing bonds in India, the tax rules on interest rated depends on three things. These are:

Considering this, the table below showcases tax rates on capital gains and interest rates.

|

Type of Bond |

Taxation on Interest |

TDS |

Simple Example (INR 10,00,000) |

|---|---|---|---|

|

Tax-free bonds (NTPC 5.6%) |

Under section 10(15) fully exempt from taxes |

No |

INR 56,000 interest is fully tax-free |

|

Government Bonds/ T-Bills |

Taxed as per your income slab rate |

20% + surcharge + cess, |

TDS deducted on earned interest |

|

Specified PSU bonds (REC/ PFC) |

if listed, tax exempt under section 10(15)(iv)(h) |

No |

INR 70,000 interest tax-free |

|

Corporate Bonds (NRI-eligible) |

Fully taxable |

20% + surcharge + cess, |

After TDS deduction, interest is taxed; DTAA relief is also available |

This is how interest from NRI bonds is taxed in India. Moving forward, let's know what the capital gains tax on NRI bonds is.

If you sell or redeem the bond before maturity, any profit you receive from that is considered capital gains. The capital gain taxation depends mainly on how long you hold the bond.

This was all about the capital gains tax on NRI bonds. Moving ahead, now let's know how 54EC bonds help in saving capital gains tax.

Investing in 54EC bonds helps NRIs save long-term capital gains from property sales. However, for this, they need to meet the following conditions:

If the above-mentioned conditions are fulfilled, the entire capital gains become tax-free for NRIs. Now, moving further, let's know the repatriation rules for NRI bonds.

The repatriation rules depend on the NRI account you used for NRI bond investments in India. Considering this:

|

Account Type |

Principal Amount Repatriation |

Interest Amount Repatriation |

Annual Limit |

|---|---|---|---|

|

NRE |

Fully |

Fully |

No specific limit |

|

NRO |

Restricted |

After taxation |

Up to USD 1 million per financial year |

|

FCNR |

Fully |

Fully |

No specific limit |

Additionally, if you are repatriating funds more than INR 5,00,000 using an NRO account, you need to fill out Form 15CA and 15CB.

Moving forward, let's know the compliance and filing for investments in NRI bonds.

Once invested in Indian bonds and securities, NRIs should fulfill these compliances:

These are compliance and filing requirements that NRIs need to consider when investing in bonds in India.

At Savetaxs, our experts provide complete consultation on NRI bonds and investment-related matters.

Lastly, for NRIs looking for a long-term, more reliable investment option in India, bonds provide steady income, flexibility, and safety. Additionally, with the introduction of FAR, bond investment for NRIs in India has become more accessible. Also, in the Indian debt market, it has increased the transparency.

Further, if you need help in choosing the right NRI bond for investment, connect with Savetaxs. We provide personalized services that match your financial goals and risk appetite. So, contact us today and begin your investment journey in India.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs

_1771591706438.webp&w=828&q=75)