_1778504462654.webp&w=828&q=75)

NRI Returning to India

Final Checklist For NRIs Return To IndiaFinal Checklist For NRIs Return To India

Written by Hatim Dudhiyawala

_1779454749573.webp&w=3840&q=75)

After living years abroad, planning to return to India? You will probably be very emotional, excited, and overwhelmed. However, here is something that most of the NRIs like you realize too late: moving to India is not only about relocation but also an essential financial transition in your life.

Apart from focusing on logistics such as housing, flight, or schools, it is also important to consider moving money to India before returning. It is an important factor that most of the NRIs ignore, and it further results in costly mistakes, such as freezing a bank account, losing lakhs in avoidable taxes, and more.

So instead of struggling, let's simplify this with smart financial strategies. Want to know what they are? Read the blog and get your answers.

Financial analysis, like lifestyle planning, is an important factor that you need to consider when moving back to India. It determines whether you have a smooth financial transition or face challenges during the experience. Here are some points that tell you why financial planning is required when moving money to India before returning.

When transferring money to India, exchange rate risk for NRIs an important factor that they need to consider. Against foreign currencies like the USD, EUR, and GBP, the rupee often loses its value over time. Considering this, if you exchange all your foreign savings at one time, you rely on the exchange rate of that day. The currency exchange rates impact whether you receive big gains or losses. So instead of it, plan and exchange your money in smaller amounts. It will reduce the risk of getting a lower exchange rate.

The tax rules for NRIs returning to India depend on their residential status, i.e., it depends on how many days they live in the country in a financial year. Considering this, in the year you move back to India, you may still be classified as an NRI or RNOR (resident but not ordinary resident). You become RNOR if:

If you hold RNOR status, you are exempt from paying taxes on your global income. Many returning NRIs overlook RNOR status, and this results in paying more taxes.

This flexibility of tax planning is available only to individuals with RNOR status and is valid for up to 2–3 financial years, depending on your past residential status and number of days stayed in India. Additionally, once your residential status from RNOR changes to ROR, you are liable to pay tax on your global income.

Do not plan a last-minute money transfer before returning to India, as you will not get enough time to compare rates, properly manage your foreign bank accounts, and plan your tax positions. The rushed decision will result in costly mistakes. So instead, take at least 2-3 months to transfer money to India before returning, and plan accordingly.

These are some of the key reasons why NRI financial planning is important for moving money to India before returning. Moving ahead, let's know the smart NRI money transfer strategies you can implement when transferring your money.

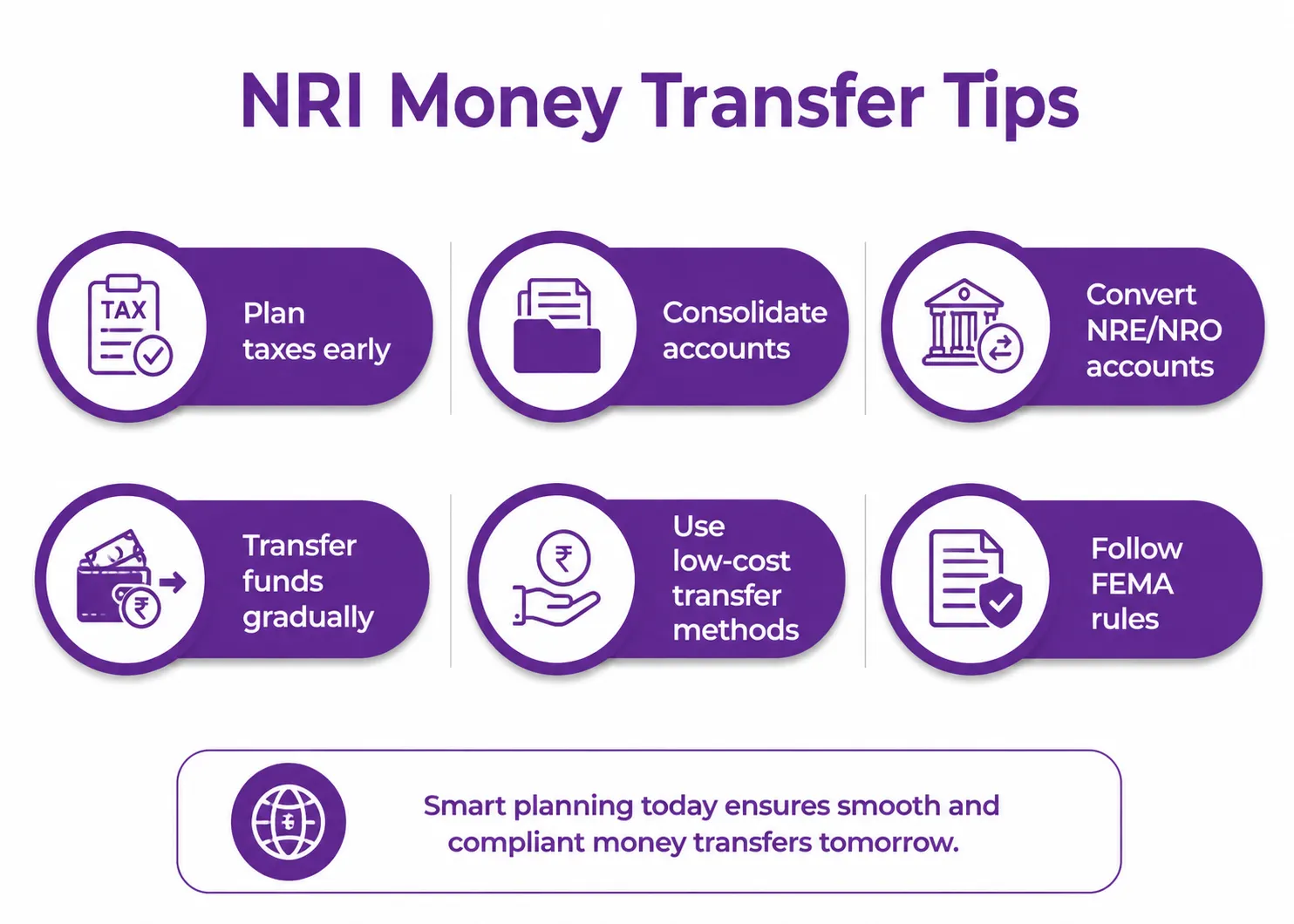

Financial planning is an essential step when you are moving money to India before returning. It helps you in avoiding legal complications after settling back in the country. Here are some smart NRI money transfer strategies that you can implement:

Take your proper time to review your foreign accounts, check the maturity date of fixed deposits, and understand how your residential status changes after returning to India. For instance, if you move back to India between January and March for that financial year, you will be considered as an NRI and from the second year you will get RNOR status, Your tax residency depends on the number of days you stay in India during the financial year, so planning your return date carefully can help optimize your tax position.

The first thing you need to consider before returning to India is reviewing all the financial accounts you hold in other countries. Combine all your foreign accounts before moving back. Additionally, to simplify management, liquidate all your non-essential assets and consolidate your scattered investments.

When you permanently move to India, change your NRE/NRO accounts to resident accounts. Considering this, convert your NRO account to a resident savings account. You can either convert your NRE account to a resident savings account or move your funds to a Resident Foreign Currency (RFC) account. RFC accounts provide you with a great benefit- without conversion to Indian rupees, you can keep foreign currency.

Rather than transferring all your foreign money in one go, move it in smaller amounts. This way, you will not be dependent on a single exchange rate. It is an effective and simple way to reduce currency exchange rate risk without predicting where the market is moving.

Choosing the right money transfer route is also an essential step when permanently returning to India. Considering this, for smaller amounts, use platforms like Remitly or Wise, as compared to bank wire transfers, these platforms offer better currency exchange rates. Additionally, for a large amount transfer, take help from a forex broker. Furthermore, whatever transfer method you use, make sure it complies with FEMA rules and is fully documented.

These are some smart strategies for transferring money to India before returning as NRIs. Moving further, let's know things NRIs should consider before returning to India.

Here is the list of things NRIs need to consider before returning to India:

Before making any financial decision, ask yourself, "How much money do you need to secure financially in India?" You have a different life in India from what you have overseas. Healthcare, lifestyle expectations, expenses, and schooling will change. So, according to your financial goals, build a realistic structure that includes:

This financial clarity helps you in avoiding the common mistake, i.e., emotionally moving back and later doing financial planning.

Create a detailed list of all your foreign financial assets. This should include:

According to Indian tax laws and guidelines from the Income Tax Department of India and the Reserve Bank of India, the tax obligations on these assets depend on your residential status in India.

Considering this, many NRIs assume that after returning to India, their foreign assets remain tax-free. Well, it is not always true. Once you become a resident in India, you are liable to pay tax on your global income, including your foreign assets and income. So, know that transition matters.

This account is specifically for individuals who were NRIs and have now become residents in India. Unlike regular resident bank accounts, in an RFC account, you do not need to convert your foreign currency into Indian currency.

In this account, you gain the flexibility to decide when and how much you want to convert based on market conditions and your financial requirements. An RFC account is particularly useful for NRIs with sizeable foreign currency savings accumulated during their employment abroad. With an RFC account, you get the following benefits:

In simple words, an RFC account works as a bridge between your financial life overseas and your future in India.

Returning NRIs often do not understand the importance of compliance. Considering this, once your residential status from NRI changes to resident, you need to report all your foreign assets in Schedule FA of your tax returns. This includes:

If you fail to disclose these assets, heavy penalties are imposed on you under the Black Money Act. For future compliance, it is vital to have records of your global financial holdings by your side.

Once you return to India, update your PAN card details with your new residential status. Additionally, to comply with Indian tax rules after returning to India, link your PAN card to your Aadhaar card.

Considering this, NRIs who have lived in India for 182 days or more in the previous financial year can apply for an Aadhaar card. Once you become eligible for an Aadhaar card, book an appointment through the UIDAI website. You can also visit your nearby Aadhaar Seva Kendra. You will need the following documents by your side:

This preparation makes everything easy, from banking to property deals, when you move back to India.

To prevent double taxation of income, India has signed a Double Taxation Avoidance Agreement (DTAA) with 90 countries. With DTAA, you get three key tax benefits:

However, to claim DTAA benefits, you need a Tax Residency Certificate from your previous country of residence. Additionally, need to file Form 67 with proof of overseas taxes paid to claim the foreign tax credit.

Note: Once you become ROR, the DTAA benefits become more beneficial for you as you are liable to pay tax on your global income in India.

Connect with Savetaxs and get expert assistance for NRI ITR filing, tax compliance, and refund claims.

Lastly, moving back to India after being abroad is a big life change. However, financial clarity determines whether moving money to India before returning will be smooth or stressful. The key is simple: start early, strategically plan, and make informed decisions. With a well-structured financial transition, you can save taxes, save your wealth, and have the confidence to enjoy your journey in India.

If you are planning to move back to India, know that every NRI has a unique situation. Your assets, income, timelines, and family goals are different. So your financial strategy should also be personalized. At Savetaxs, we assist NRIs in designing tax-efficient plans so that they can return to India with confidence and clarity. Connect with us anytime; we are available 24/7 to help you.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1777726294138.webp&w=828&q=75)

_1771668297202.webp&w=828&q=75)