_1779454749573.webp&w=828&q=75)

NRI Returning to India

Managing Money Before Returning to IndiaManaging Money Before Returning to India

Written by Hatim Dudhiyawala

An NRI must understand how US Social Security benefits are taxed in India, particularly those who are seeking to return to India and change into a new residency status. In this blog, we will walk you through everything you must know about the taxation of US Social Security benefits for returning NRIs. Additionally, we will learn about the India-US DTAA and effective tax strategies to help you stay compliant.

Your tax liability is determined based on your residential status in India under the Indian Income Tax Act, 1961. The three primary categories of residency are as follows:

For individuals with ROR status, global income, including US Social Security benefits, is taxable in India under the "Income from Other Sources" category. There are no specific tax exemptions for social security benefits under the Indian tax law, meaning the entire amount will be taxed.

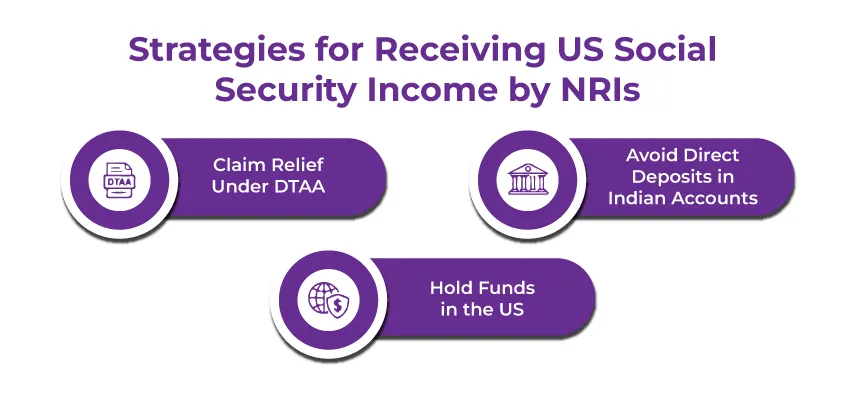

If the amount for social security benefits is credited directly into an Indian bank account, like NRE, NRO, or resident savings. Then, the amount becomes taxable in India. You must plan the receipt mode to prevent any unintended tax liabilities

Under the India-US DTAA, taxpayers can avail relief from a significant tax amount:

If you are an NRI receiving US Social Security income, here are some strategies that you must consider:

Follow the steps below if you are an ROR and need to report US Social Security benefits:

If you are an NRI returning to India, you need to understand the tax implications of US Social Security benefits in India to stay compliant. You need to understand DTAA also to claim tax benefits and reduce a significant tax amount. Additionally, ensure to report the US social security benefits in the correct ITR form, which is ITR-2 or ITR-3.

Furthermore, if you need more assistance with navigating taxation for US social security benefits, understanding DTAA, or tax compliance for NRIs. Then, contact the experts at Savetaxs. We have a team of experts with years of experience in this field. They will offer personalized guidance to ensure you stay compliant while returning to India and make this transition easier. Contact us whenever needed, as we are working 24*7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1778504462654.webp&w=828&q=75)

_1777726294138.webp&w=828&q=75)

_1771668297202.webp&w=828&q=75)