Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

_1778590821795.webp&w=3840&q=75)

Yes, NRIs can invest in Indian mutual funds. Under the Foreign Exchange Management Act (FEMA), 1999, mutual fund investments by NRIs are permitted and well-regulated. However, there are certain rules for NRIs regarding which bank account to use, how taxation applies after the Finance Act 2023 changes, how TDS is deducted on NRI investments in mutual funds, and more, which they must follow when investing.

In this guide, we will cover all these segments and why NRIs from the USA and Canada face additional restrictions while investing in Indian mutual funds.

The mutual funds industry in India grew to over Rs 65 trillion in assets under management as of early 2026. This has made India one of the world's largest and most dynamic financial markets. When it comes to NRI status, Indian mutual funds offer a compelling combination of professional management, growth potential, currency diversification, regulatory transparency, and more.

Savetaxs helps NRIs file their ITR in India under expert guidance and with 100% compliance.

The FEMA regulatory framework permits the NRIs to invest in Indian mutual funds. The following category of persons qualify:

As an NRI, you can invest in Indian mutual funds across all SEBI-regulated categories, including equity, debt, hybrid, liquid, and thematic. There are no fund categories exclusively reserved for NRIs by regulation, as the restrictions are generally AMC-specific rather than SEBI-mandated.

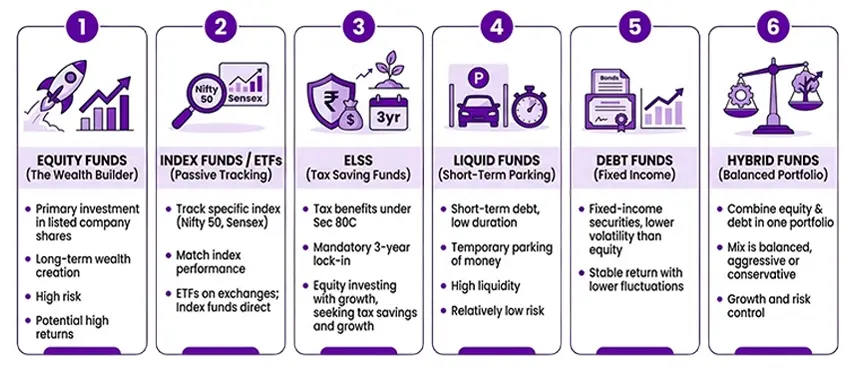

The following are the types of mutual funds an NRI can invest in:

Equity Funds: You can think of an equity mutual fund as a "wealth builder." Equity mutual funds are the funds that invest primarily in shares of listed companies. They are designed for long-term wealth creation and generally carry a high market risk. But with higher risk comes potentially higher returns over time.

Index Funds/ETFs: These are passive mutual funds that track a specific market index, such as the Nifty 50 or the Sensex. These funds do not try to beat the market; instead, they aim to match the performance of the chosen index. ETFs are bought and sold on the stock exchange, while index funds are purchased directly from the mutual fund house.

ELSS (The Tax Saving Funds): These are equity funds that offer certain tax benefits under Section 80C, subject to applicable tax rules. This comes with a mandatory 3-year lock-in period and involves investing in equity-related securities, making it appropriate for investors seeking tax savings alongside long-term growth potential.

Liquid Funds: These are the short-term debt mutual funds that invest in low-duration money market and fixed-income instruments. Liquid funds are generally intended for temporary parking of money and are known for their high liquidity and relatively low risk.

Debt Funds: These mutual funds invest in fixed-income securities, including corporate bonds, government bonds, treasury bills, and other money market instruments. The sole objective of these funds is to generally provide a stable return with lower volatility than the equity funds.

Hybrid Funds: These are mutual funds that combine equity and debt investments in a single portfolio. This mix is balanced, aggressive, or conservative depending on the fund's objective, making it suitable for investors who want both growth and some risk control.

The following is the step-by-step investment process for NRIs in India.

Confirm your AMC eligibility for your residential country: Before you start, check that the AMC you're planning to invest with accepts investors from your country of residence. This is because NRI investors from the USA and Canada face restrictions at most AMCs, and other residential counties are generally capped. Henceforth, check the AMC's key information number (KIM) on the scheme information documents (SID) for country-specific restrictions.

Open or active NRE/NRO Bank Accounts: If you don't already have one, open an NRE account (preferred for full repatriation of funds) with an authorized bank in India, such as ICICI, Axis, SBI, HDFC, Kotak, and so on. Most banks nowadays offer complete digital account-opening systems from abroad via their NRI banking portal. You can also make the investments via an NRO account, but it has restrictions on full repatriation.

Get A PAN Card: A PAN Card is mandatory for all mutual fund investments. Without PAN, TDS is deducted at 20% under Section 206AA. Apply online via the NSDL portal using Form 93 for Indian citizens and NRIs, and Form 95 for individuals who are not citizens of India.

Complete NRI KYC: Complete the NRI KYC through a trusted online portal. Provide documents such as PAN, passport, overseas address proof, FATCA/CRS declaration, and photocopies. Ensure that NRI KYC is a one-time process and is valid across all the AMCs once done.

Choose Your Fund & Investment Mode: Once your KYC is complete and you are ready to invest, decide on the type of fund you would like to invest in, such as equity, debt, hybrid, liquid, and so on. After deciding on the type of fund, choose your fund scheme and the investment mode. In investment mode, you can choose between a SIP, which allows regular monthly investments, and a lump-sum, one-time investment. You must compare the expense ratios, past performance, and the fund manager's track record.

Invest Online Via the AMC portal on the NRI investment platform: You can invest directly on the AMC's NRI banking portal or through SEBI-registered platforms or NRI-specific platforms. You just need to mention your NRI status, NRE/NRO bank account details, and your preferred options.

Monitor, Review & File ITR Annually: Once the investment is made, monitor your investments via the AMC portal or consolidated account statements (CAS). You can download your CAS annually before filing your Indian ITR. Report all the mutual fund capital gains (STCG and LTCG) in your ITR-2 schedule CG. Filing an ITR helps claim refunds for excess TDS deducted at the time of redemption.

In terms of rates, the taxation of mutual fund gains for NRIs is identical to that of residents. The difference here lies in how the TDS is deducted upwards and at what rate. Furthermore, for NRIs, understanding the post-Finance Act 2023 changes is critical.

| The holding period | Type | Tax Rate | TDS For NRIs |

|---|---|---|---|

| Up to 12 months | Short-term capital gains (STCG) | 20% (raised from 15% in Budget 2024). | 20% |

| More than 12 months | Long-Term Capital Gains (LTCG) | 12.5% on gains above Rs 1.25 lakh a year. | 12.5% |

| More than 12 months | LTCG exceeding ₹1 lakh annually | Nil - exempted | 12.5% TDS deducted; refund via ITR. |

| Holding Period | Type | Tax Rate | TDS For NRIs |

|---|---|---|---|

| Any Period | Treated as STCG (Section 50AA) | The Income tax slab rates are 5%, 10%, 15%, 20%, or 30%, depending on the taxpayer's income. | 30% TDS (at the highest slab rate). |

| Holding Period | Type | Tax Rate | TDS For NRI |

|---|---|---|---|

| Up for 24 months | STCG | Slab Rate | 30% |

| More than 24 months (for the mutual fund units purchased before April 1, 2023) | LTCG | 12.5% (without indexation) | 12.5% |

Note: NRIs must ensure that no indexation benefit is available for any mutual fund category from FY 2024-25 onwards.

Get an NRI business expert consultation for seamless business operations.

Yes, NRIs can invest in mutual funds in India under the FEMA regulatory framework. As an NRI, if you are planning to participate in the growth of the Indian economy, this is a great investment product. Investments can be made on a repatriable or non-repatriable basis. Along with this, you understand that the taxation applicable to capital gains for NRIs in India is essential. Furthermore, you must have your KYC completed, and NRI investors from the US/Canada must be extra careful, as they face additional restrictions.

At times, investment in India for NRIs can be overwhelming; hence, seeking professional assistance is advisable. And when it comes to NRI investment assistance in India, Savetaxs is the name to trust. Our experts have a dual-certified team of CAs and CPAs, ensuring your investment complies with both India and your home country's requirements.

From KYC compliance guidance to banking account setup, mutual fund selection, advisory, regulatory adherence, profile monitoring, transaction management, and more, our experts will help you with everything you need to make a successful mutual fund investment in India.

Connect with us as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)