NRI Banking Services

Difference Between Remittance and RepatriationDifference Between Remittance and Repatriation

Written by Hatim Dudhiyawala

_1771851103775.webp&w=3840&q=75)

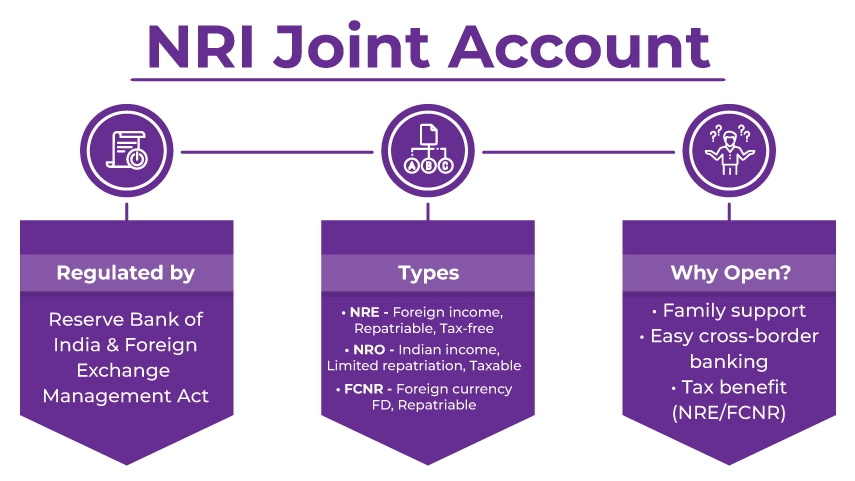

For NRIs who support their families in India or maintain financial ties back home, managing finances across borders can be challenging. An NRI joint account is an important financial tool designed to address such needs efficiently.

Joint accounts allow NRIs to hold accounts jointly with other NRIs, OCIs, PIOs, and resident Indians — subject to the regulatory framework of the Foreign Exchange Management Act (FEMA) and Reserve Bank of India (RBI) guidelines.

In this blog, we will discuss NRI joint accounts, their types, eligibility rules, documentation requirements, operational conditions, taxation aspects, and how to open one correctly.

NRIs can open three primary types of accounts depending on their income source and financial objective.

Joint Holding Rules:

Joint Holding Rules:

Joint Holding Rules:

Under RBI guidelines (aligned with Companies Act definition), close relatives include:

Friends, cousins, business partners, and distant relatives are not considered close relatives for NRE/FCNR joint holding purposes.

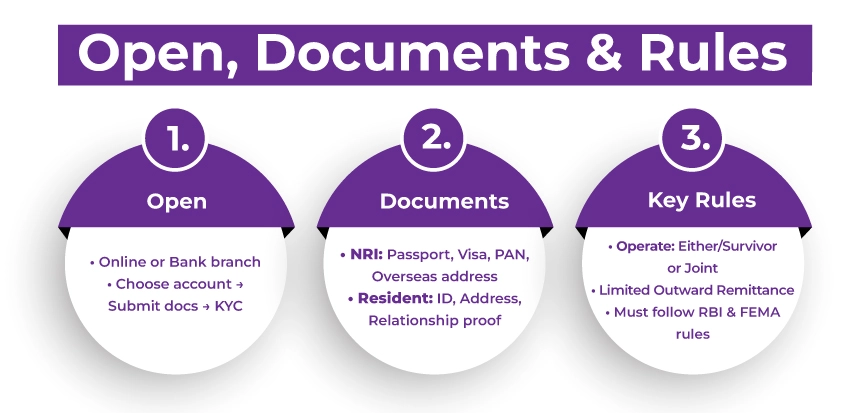

Documentation may vary by bank, but generally includes:

Note: Banks may request additional KYC documentation depending on compliance requirements.

Opening an NRI joint account can be done either online or offline.

Processing timelines typically range between 7–15 working days, depending on documentation completeness.

The mode of operation determines how the account functions:

Important Operational Restrictions:

The following conditions ensure that the NRI joint account complies with FEMA guidelines and meets the financial objectives of both NRIs and resident joint holders.

Tax liability typically follows the primary holder status unless income attribution rules apply.

Professional tax advice is recommended for correct reporting in India and abroad.

NRI joint accounts offer an array of advantages that make them a preferred choice for cross-border financial management.

The following benefits of NRI joint accounts make them an essential financial tool for NRIs seeking to maintain financial stability and convenience in India.

Expert help from Savetaxs NRI banking experts for hassle-free compliance.

NRI joint accounts are a structured financial solution for managing cross-border responsibilities while remaining compliant with Indian regulations. When set up correctly, they offer security, operational convenience, and tax efficiency.

However, the rules differ significantly based on:

Understanding these distinctions before opening the account can prevent operational restrictions, tax complications, and regulatory issues later.

As an NRI, if you are seeking professional guidance to open a joint accout account in India that is right for your financial goals, Savetaxs is the name to trust. Our banking experts provide end-to-end assistance in onboarding procedures for NRIs, handling KYC compliance, key documentation, and product guidance for NRE NRO accounts.

We have been helping NRIs across 90+ countries open their NRI-designated bank accounts. Connect with us as we serve our clients 24/7 across all time zones.

Sources: Income Tax Department, ICICI Bank, Reserve Bank of India, HDFC Bank, Axis Bank, State Bank of India, The Economic Times, Times of India, ClearTax

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1781767087029.webp&w=828&q=75)