NRI Banking Services

Difference Between Remittance and RepatriationDifference Between Remittance and Repatriation

Written by Hatim Dudhiyawala

An NRI's (Non-Resident Indian) regular resident savings account becomes invalid when they obtain the NRI status. They are required to open an NRI bank account to manage their financial transactions within India, such as a Non-Resident External (NRE) account.

An NRE account is a bank account for NRIs that allows them to manage the income that is earned outside India. This account offers several benefits, including providing tax-free interest income in India and full repatriation of both principal and interest back to the resident country. It also allows you to manage and hold your foreign earnings in Indian Rupees.

Given the benefits of an NRE account, finding the best NRE accounts in India from a huge number of banks can be a task. To make it easier, in this blog, we have compiled a list of the 5 best NRE accounts in India for NRIs.

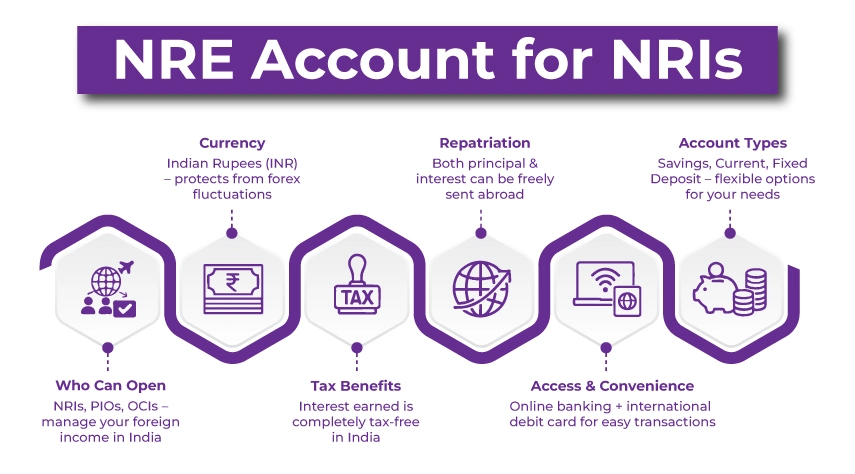

An NRE (Non-Resident External) account is a bank account for NRIs (Non-Resident Indians), PIOs (Persons of Indian Origin), and OCIs (Overseas Citizen of India) to manage their foreign income in India. It is a rupee-denominated account that an NRI can open to deposit their foreign currency earnings.

One primary benefit of an NRE account is its high liquidity, which permits the full repatriation of funds to their country of residence. Here are some key features of an NRE account:

NRE (Non-Resident External), NRO (Non-Resident Ordinary), and FCNR (Foreign Currency Non-Resident) are various types of NRI accounts. The table below shows the difference between an NRE, an NRO, and an FCNR (B) account based on the account features:

| Account Features | NRO | NRE | FCNR (B) |

|---|---|---|---|

| Account Maintained In | Indian Currency | Indian Currency | Foreign Currency |

| Tax Implications on Interest Earned in India | Taxable in India | Tax-Free in India | Tax-free in India |

| Currency Deposit | Indian Rupee | Indian Rupee | Any permitted foreign currency |

| Withdrawal Currency | Indian Currency | Indian Currency | Foreign Currency |

| Power of Attorney (PoA) | Permitted | Permitted | Permitted |

| Account Types |

|

|

|

| Joint Holding | It can be held by two or more NRIs/PIOs. Also, it can be held on a 'former or a survivor' basis* with a resident. | It can be held by two or more NRIs/PIOs and can be held by a ' former or survivor', *based on a resident relative** | It can be held by two or more NRIs/PIOs. It can also be held on a 'former or survivor' *basis with a resident relative.** |

| Allowed Payments and Transfers |

|

|

|

| Repatriation |

|

|

|

**The term 'former' or 'survivor' basis refers to the condition where only one of the two joint account holders, that is, the former account holder, can mainly manage the account. Once the 'former' passes away, the 'Survivor' can manage the account.

**A relative is defined under Section 2 (77) of the Companies Act, 2013. It includes their parents (including stepparents), son (including stepson), son's wife, daughter, her husband, siblings (including stepsiblings), and children.

Here is a list of the top five NRE bank accounts in India and the key features offered by them for NRIs:

The HSBC Bank NRE account is one of the best NRE bank accounts for NRIs. It is known for its amazing features and benefits. Here are some of the key features and benefits:

Axis Bank NRE account offers easy repatriation, tax-free interest, and global access for NRIs. Below are the key features and benefits of the Axis Bank NRE account:

HDFC NRE account offers personalized services and higher withdrawal limits. It is preferred by NRIs because of the benefits and features mentioned below:

ICICI NRE bank account offers 24*7 digital banking options, global money transfers, and other benefits. It is one of the most chosen savings bank accounts by NRIs because of the following features and benefits:

SBI NRE account has a wide branch network and provides several benefits and features, which are as follows:

When choosing an NRE account, you must consider the following factors to choose the best NRE account:

You need to gather and provide some documents to open an NRE account. These include:

Follow the steps below to open an NRE account:

Choosing the best NRE account in India can be a big game-changer for NRIs who wish to manage their funds from abroad. You can use an NRE account to deposit your foreign earnings. It is a rupee-denominated account, ideal for expenses and investments in India. An NRE account offers several benefits to an NRI, including tax-free interest income in India and the option to repatriate funds with no limits freely.

Furthermore, if you wish to open, operate, and manage your NRE bank account with utmost convenience, connect with Savetaxs. We have ties with the top banks in India, ensuring that the processing of your application is done quickly. With a team of expert CAs carrying more than 30 years of experience, you can stay confident that there are no mistakes or rejections during the process.

NRIs from around the world trust us for our exceptional services. So connect with us 24*7, as we are working around the clock across all time zones to provide you with comfort and peace of mind.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1781767087029.webp&w=828&q=75)