Business Setup

Difference Between a LLP and a Partnership FirmDifference Between a LLP and a Partnership Firm

Written by Hatim Dudhiyawala

A change in your residential status can affect everything, be it your tax obligation or compliance requirements. If you are an NRI owning a business in India, a change in your residential status under Indian laws can significantly trigger major changes. Whether you are a freelancer, startup founder, or investor, you must understand these changes to avoid non-compliance issues and significant consequences.

In this blog, we will walk you through everything you need to know after NRI status changes as per Indian tax rules. We will also cover the FEMA compliance rules for NRIs and the actionable steps you need to take.

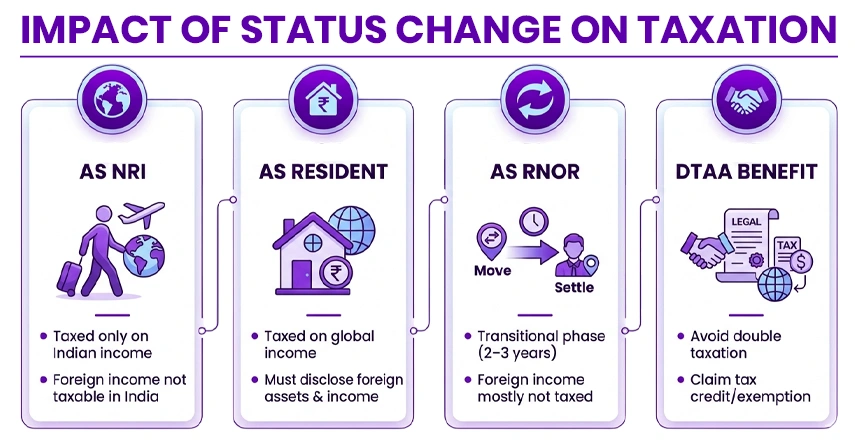

To determine your tax liability in India, the Income Tax Act 1961 considers your residential status instead of your citizenship. Based on your physical presence in India, your residency status can fall into three categories:

Get expert guidance every step of the way.

As per the Income-tax Act, 1961, your NRI status is not permanent; it depends mainly on the duration of your stay in India during a financial year. You will be considered a resident for tax purposes if you spend 182 days or more in India. This change can happen even if you didn't want it.

Mostly, people don't plan for a change in status, and it usually happens because of real-life situations, such as:

Returning to India permanently

Managing or Expanding a Business in India

Staying Longer than Expected

Even if your extended stay is unplanned, it can trigger a change in your residential status. This change can directly affect your tax obligations and business compliance.

A change in NRI status has an immediate and wide-ranging impact on business. Apart from affecting your personal tax liability, it also impacts how your business operates both legally and financially. Here's what changes immediately when your NRI status changes after starting a business:

These changes can happen within the same financial year, leading to many NRIs being unprepared. Moreover, you must inform your bank and update your Tax Filings and business records about your status change immediately. Failing to do so can attract penalties and issues with compliance.

One major factor that the change in NRI status affects is tax implications. Here's how you will be taxed when you are an NRI and after you become a resident:

To prevent paying taxes twice, India has signed an agreement with several countries. This agreement is known as the Double Taxation Avoidance Agreement (DTAA). You can claim a tax credit or exemption and ensure the same income is not taxed in both countries.

In short, NRIs have limited tax liability (India only), RNOR gets partial relief, and ROR is liable to pay tax on global taxation. Moreover, if you have paid tax in one country, you can claim relief in India by using the DTAA provisions.

Once your status changes, your banking structure will change significantly. Let's understand how a status change affects your banking and repatriation:

As an NRI, you can usually hold:

After becoming a resident:

Repatriation refers to sending money abroad. The biggest change happens here:

As an NRI:

As a Resident:

So, after transitioning to a resident, you face some restrictions and regulatory issues while moving funds abroad. You may also need approvals or fall under limits set by the RBI (Reserve Bank of India).

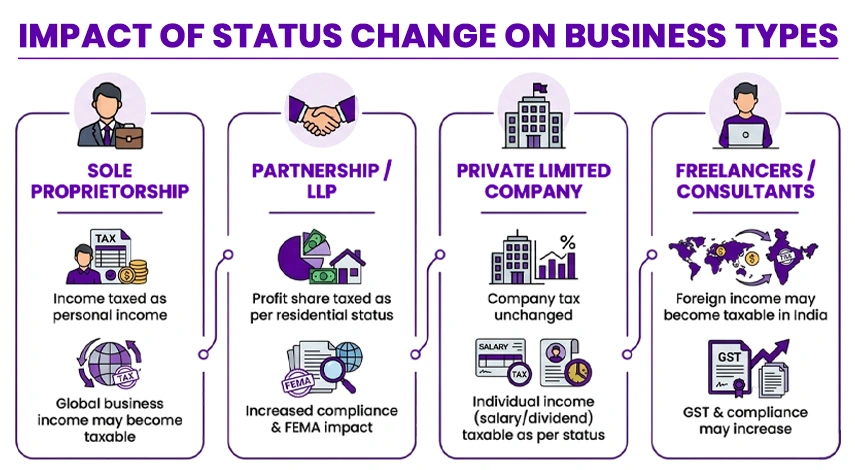

The impact of a change in status on your business will depend on the type of business you own.

A sole proprietorship is a business type where the business and owner are the same. In such a business type:

This business structure is impacted the most directly.

In partnership firms/LLPs, your share of profit is taxed based on your residential status. So, if any partner becomes a resident:

If foreign investments are involved, FEMA implications may also arise.

A company is a separate legal entity. Hence, the company's taxability remains unaffected. However:

For individuals:

Freelancers/consultants face major changes:

Due to global income being subject to taxation, many freelancers may face unexpected tax liabilities.

Once you become a resident, your status under the Foreign Exchange Management Act also changes. FEMA decides how your foreign money, investments, and transactions are managed. Here's what changes after your status changes:

For example:

The investments you made as an NRI will be treated differently now. Also, you may need approvals for certain transactions.

Once you become a resident, complying with FEMA becomes more rigid and regulated.

Your responsibilities related to compliance increase significantly when your status changes. Follow the steps below to ensure compliance:

Following these steps is crucial as non-compliance can attract income tax notices, hefty penalties, and increased scrutiny from the authorities.

To make this situation easier to understand, here are two examples of Amit and Priya:

Amit is an NRI who holds an NRE account with Rs. 50 lakh savings. He receives rental income in India and has investments in US stocks. Now, he decides to move back to India permanently, which means his NRI status will change. Hence,

To claim relief from double taxation, he can claim the double taxation avoidance agreement (DTAA). This will help him prevent taxation twice on US income.

Restructure your banking and investment structures right away after your status changes. Now, let's look at an example of Priya.

Priya lives in Singapore, but she owns a startup that is registered in India. Due to this, she frequently travels to India. However, she stayed in India for 190 days in a financial year unintentionally. It led to her NRI status changing to a resident. Now, this is how this transition will impact her liability and compliance:

In short, even unintentional long stays or unplanned travel can affect your residency. Also, it will directly increase your tax and compliance burden immediately.

A change in your NRI status brings a complete shift in your financial and regulatory matters. It affects your tax obligations, compliance, banking, and even business operations. One major challenge with NRI status change is that this transition often happens unintentionally. It makes many individuals unprepared to face issues. To address this, you must keep track of your duration of stay in India. Additionally, you must also be aware of the ROR transition benefits, restructure your banking setup, and ensure full compliance with FEMA and tax regulations.

Whether you are a freelancer, investor, or business owner, Savetaxs can help you be prepared for this transitions. At Savetaxs, we have a team of experts who can help you stay aware and knowledgeable of your residential status. Our team will ensure you avoid significant penalties and tax burden, and maintain smooth business continuity. Connect with us right away, as we are actively working 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1780491123033.webp&w=828&q=75)

_1778757638178.webp&w=828&q=75)