_1784547039242.webp&w=828&q=75)

NRI Income Tax Compliance

30+ Important Income Tax Terms in India You Need to Know30+ Important Income Tax Terms in India You Need to Know

Written by Shubham Jain

A taxpayer's income is divided into five heads of income as per the Income Tax Act. For accurate calculation of taxes, you must classify your earnings correctly under these five income heads at the end of each financial year. It becomes important for you to understand which earnings belong to which head of income. This blog will give you a clear overview of the five heads of income.

According to Section 14 of the Income Tax Act, 1961, every income subject to taxation under the Income Tax Act, and for calculating the total income, must be classified under the following five heads:

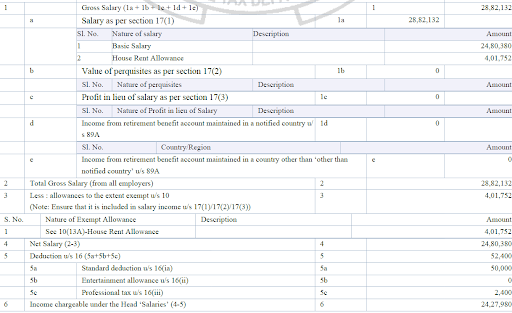

Income received in return for the services you provide under an employment contract is taxed under this head. It includes salary, advance salary, gratuity, commission, perquisites, annual bonus, and pension. The following sections govern salary income:

Some necessary exemptions under this head include:

You must report salary income details in Schedule S of your ITR form.

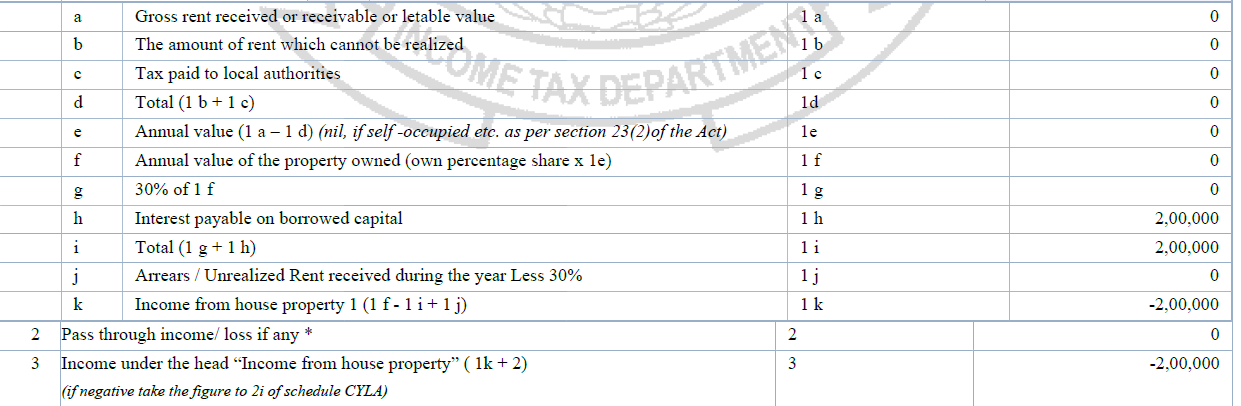

Any income received from a residential or commercial property is taxed under this head. Primarily, this includes rental income. House property income is classified into:

If you own more than two self-occupied houses, only two will be treated as self-occupied. The remaining will be considered deemed let-out property (correct spelling updated).

Income from both commercial and residential properties rented out is taxable under this head. You must mention these details in Schedule HP of your ITR.

Under this head, profits or gains you earn from any business or profession are taxable. You can deduct expenses incurred to earn such income.

The following types of income are chargeable under this head:

Individuals and HUFs earning income from business or profession must file ITR-3 or ITR-4.

Profits you earn by selling or transferring a capital asset held as an investment are taxed as capital gains. Capital assets include gold, mutual funds, stocks, bonds, and real estate. Capital gains are classified as:

Below is the updated table showing holding periods and tax rates:

| Asset Nature | Holding Period | Short-Term Tax Rate (Sold before 23-Jul-2024) |

Short-Term Tax Rate (Sold on or after 23-Jul-2024) |

Long-Term Tax Rate (Sold before 23-Jul-2024) |

Long-Term Tax Rate (Sold on or after 23-Jul-2024) |

|---|---|---|---|---|---|

| Immovable property (Land / House / Flat) |

24 months | Slab Rates | Slab Rates | 20% after indexation | 12.5% (no indexation)** |

| Unlisted equity shares | 24 months | Slab Rates | Slab Rates | 20% after indexation | 12.5% (no indexation) |

| Listed equity shares / Equity mutual funds | 12 months | 15% | 20% | 10% | 12.5% (no indexation) |

| Other capital assets | 36 months | Slab Rates | Slab Rates | 20% after indexation | 12.5% (no indexation) |

| Non-equity mutual funds (Debt funds purchased after 1-Apr-2023) |

— | Slab Rates | Slab Rates | Slab Rates | Slab Rates |

Note:

You need to include the details of capital gains in Schedule CG of your ITR. If you are an individual, you need to choose ITR-2 or ITR-3.

Any income not covered under the above four heads is taxed here. These fall under Section 56(2) and include:

According to the Income Tax Act, a head of household classifies an individual’s earnings for tax purposes. The five heads include:

On the other hand, sources of income refer to where the income is actually earned from.

The five features of tax are:

This blog will help you understand the five heads of income with sections. You can now easily classify your income under the proper heads, which is mandatory. However, if you want to compute your overall tax liability accurately and eliminate unnecessary penalties, you can either use an Income tax calculator or contact the experts at Savetaxs.

We are a team of Chartered Accountants, Company Secretaries, and legal experts with more than 30 years of experience, helping NRIs with tax-related matters for over two decades. Whether you need help filing ITR or handling any tax issue, our experts are available 24×7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784546974133.webp&w=828&q=75)

_1784376356528.webp&w=828&q=75)

_1784375756402.webp&w=828&q=75)