_1783600706732.webp&w=828&q=75)

US Tax Filing and Compliance

Can You Keep a US Green Card After Moving to India?Can You Keep a US Green Card After Moving to India?

Written by Shubham Jain

While living in the US, many Indian origin green card holders reach a point where they decide to move back to India permanently for family, retirement, career, or simply a change of life. The emotional and logistical sides of that decision often get a lot of attention, but the taxation side? Far too little.

Surrendering a US green card is not just an immigration formality. Depending on how long you have held it and your financial profile, it can trigger a significant US tax event commonly called the exit tax. Getting this wrong will definitely result in the unexpected tax bills, penalties, and compliance problems that are going to follow you across the oceans.

In this blog, we will discuss the green card surrender tax, what happens after moving to India, and more.

The green card surrender tax is also formally known as the US expatriation tax or the exit tax. This is a kind of tax that the United States imposes on individuals who give up their US permanent residency status.

When you surrender your green card and meet a certain set of criteria, the IRS (Internal Revenue Service) treats you as having sold all your worldwide assets on the day before your expatriation date at their fair market value. Any gains above the annual exclusion amounts will be subject to US taxes, even if you haven't actually sold anything.

And this is not a penalty for leaving the country; it is the US government's mechanism to collect tax on unrealized appreciation on your assets before you exit the US tax system permanently.

These exit tax rules are governed by Section 877A of the Internal Revenue Code, enacted in the Heroes Earnings Assistance and Relief Tax Act of 2008 (HEART Act).

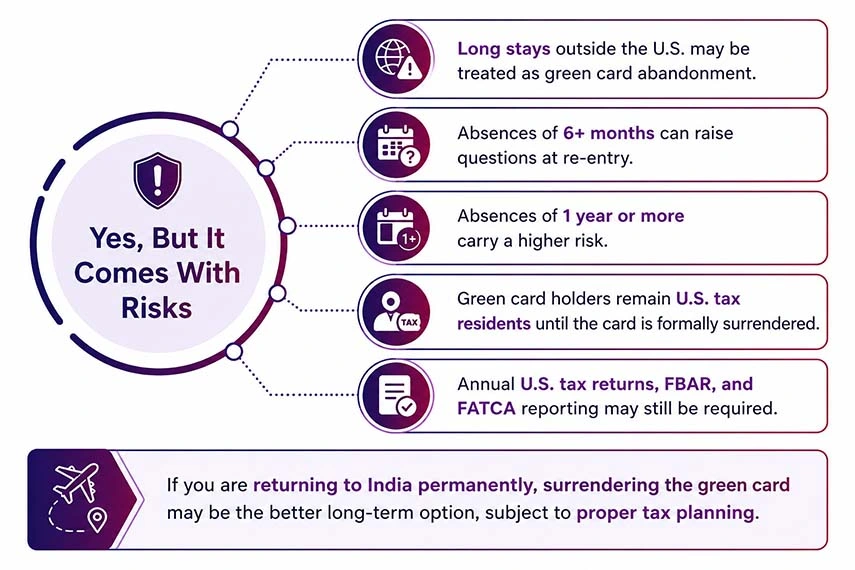

Technically, yes, you can hold your green card while you move back to India and live there, but practically it is complicated and should not be done.

A green card provides you with the right to live and work permanently in the US. Now, if you move to India and stay there for the long term without surrendering green card, US Customs and Border Protection (CBP) can determine that you have abandoned your permanent resident status when you try to re-enter. A long absence, typically for six months or more, will trigger questions at the border, and the absence of one year or more is particularly risky.

That aside, some green card holders try to maintain their status by periodically returning to the United States or by obtaining a re-entry permit (which specifically provides some protection for absences of up to two years). But here is another layer most people tend to overlook: US tax obligations.

As long as you have your green card, you remain a US tax resident, which means you are required to file the annual US tax returns, report worldwide income, and comply with FBAR and FATCA reporting for foreign financial accounts. Many green card holders living in India do not realize that they are still legally required to file the US returns, and the consequences of non-filing can be extremely severe.

In a nutshell, if you have permanently moved back to India and have no intention of returning to the US, surrendering your green card is generally better and the best approach because, both legally and from a tax compliance standpoint, it is important. However, ensure that the timing and the manner of the surrender matter significantly.

Savetaxs helps NRIs file their taxes in India under expert guidance and with 100% accuracy.

The US exit tax is applicable when you formally choose to expatriate, meaning you surrender your green card or renounce US citizenship. Not every individual who expatriates owes the US exit tax. It generally applies only to individuals classified as covered expatriates.

If you are not a covered expatriate, your expatriation will not trigger the exit tax, though you still have final year filing obligations.

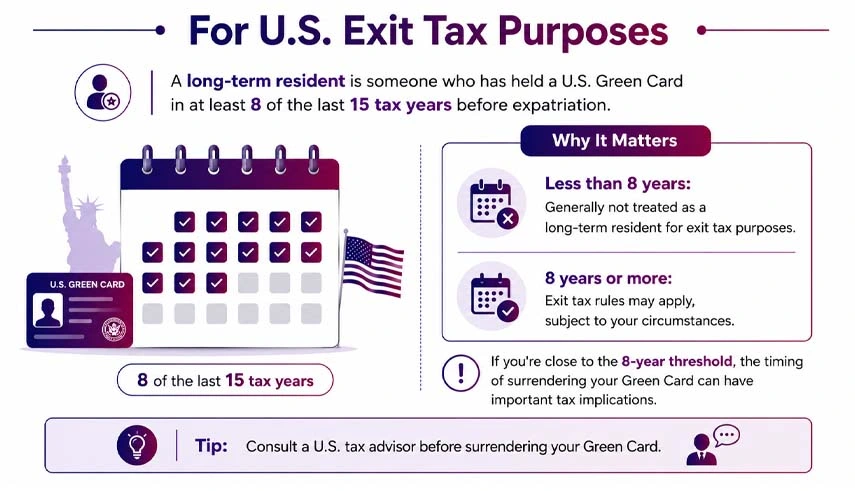

For exit tax purposes, a long-term resident is someone who has been a lawful permanent resident (green card holder) in at least 8 of the last 15 tax years ending with the year of expatriation.

This is one of the most critical thresholds. If you have held your green card for fewer than 8 years and you are surrendering it, you will not be classified as a long-term resident for exit tax purposes, and covered expatriate rules are not applicable to you, though other final year filing requirements still do.

In case you are approaching the 8-year mark and considering surrendering, the timing of your surrender could have significant tax implications. Surrendering before completing the threshold of eight years may eliminate the exit tax purpose entirely, but only if your specific situation supports it. Confirm this with a US tax advisor before you act.

The following are the tax consequences of surrendering a green card:

You are classified as a covered expatriate if you meet any one of the following three tests.

The tax compliance test often catches many people who assume that they are fine because net worth is below $2 million. If your US tax filing history has gaps, you become a covered expatriate regardless of your wealth.

If you are a covered expatriate, the IRS applies the mark-to-market rule, treating you as if you sold all your worldwide assets at the fair market value on the day before your expatriation date.

Any net gain above the annual exclusion amount, such as $866,000 for 2024, which is adjusted annually, is subject to US capital gains tax. This certainly means.

There are certain exceptions and deferrals available; for example, certain deferred compensation items and specified tax-deferred actions are not subject to any mark-to-market rules and are instead tracked very differently when the distributions are actually made. You must consult a US CPA who is well-versed in cross-border taxation to determine how to apply these to your specific asset mix.

The covered expatriates must file:

Even non-covered expatriates are generally required to file Form 8854 to certify their tax compliance and report expatriation information. If you fail to file Form 8854, it will straightaway result in the expatriate being treated as a covered expatriate, regardless of their actual financial profile.

The formal process to surrender your green card involves both immigration and tax steps, and both must be completed correctly.

This is an official form for surrendering your green card voluntarily. It can be filed at the US embassy or consulate in India, or even at the port of entry. You have to submit your physical green card along with the form.

After filing Form I-407, you will receive a confirmation that your status has been abandoned. Keep this document with you, and it establishes your expatriation date for tax purposes.

Your expatriation date is the date you file your Form I-407. This date determines which tax year is your final year as a US tax resident and when the deemed sales rules are applicable to you.

To do so, file Form 1040 for the year of expatriation, covering income from Jan 1 to your expatriation date. This is a dual-status return; you were a US resident for part of the year and a non-resident for the rest.

You shall attach Form 8854 to your final return and send a copy directly to the IRS address specified in the form instructions. This step is certainly mandatory for everyone who expatriates, covered or not.

If you are a covered expatriate with gains above the exclusion, calculate and pay the exit tax with your final tax return; installment payment options may be available for illiquid assets, but only if you file a bond or security with the IRS and make the election on time.

Let us understand this with an example:

Sunita is an Indian born engineer who has obtained a US green card in the year 2010. She worked in the United States for at least 12 years and has accumulated significant assets, including a US brokerage account worth $350,000 and a US retirement account (401 (k)) worth $280,000. Along with this, she currently has a flat in Hyderabad valued at approximately Rs 1.2 crore (roughly $145,000 at current rates). In 2024, she has decided to move back to India permanently.

Since Sunita has held her green card for more than 8 years now, she is a long-term resident. Her worldwide net worth is around $800,000 short of the $2 million threshold. Her average annual tax for the past 5 years was well below $201,000. She has filed the US returns every year without gaps.

Sunita does not meet the net worth or any income tax tests. So whether she is covered as an expatriate depends entirely on her tax compliance certificate on Form 8854. Since she has been compliant, she is not a covered expatriate. The exit tax deemed-sale rules do not apply to her.

She filed her final Form 1040 for 2024 (covering from Jan to her expatriation date), attached Form 8854 certifying her 5-year compliance, and filed her final FBAR for the year. She has no exit tax liability no matter what.

Savetaxs provides NRIs with end-to-end expert-level CA and CPA consultation for their tax matters.

The following are the common mistakes when surrendering a green card.

As an NRI, for you to surrender a US green card after moving to India is a significant legal and financial decision and not just an immigration formality. The exit tax rules under section 877A can impose real tax costs on covered expatriates, defined broadly to include more people than most expect, particularly through the tax compliance test.

However, the good news is that with appropriate planning, many people can surrender their green card without triggering exit tax at all. The sole key is that you must ensure your US tax filing history is clean for the last five years; you must understand your net worth position relative to the $2 million threshold; and you must time your surrender strategically around the 8-year long-term resident mark, and complete all of the required tax filings, specifically Form 8854, correctly on time.

If you are planning to move back to India without any intention of returning to the US, start planning the green card surrender process at least 12 months before your surrender date. This is because the tax and financial analysis will take time, and the decisions you make before surrendering are far more powerful than anything you can do after.

In case you are seeking professional assistance to help you figure out your exit tax or maybe a team that has the expertise of both a CPA and a CA to help you plan your Indian return better while simultaneously ensuring all your US tax obligations are met, Savetaxs is the name to trust.

Connect with us as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1783512660762.webp&w=828&q=75)

_1782391419380.webp&w=828&q=75)

_1782129946793.webp&w=828&q=75)