_1782391419380.webp&w=828&q=75)

US Tax Filing and Compliance

Missed the Tax Deadline? 3 Reasons to File Your Late Tax Return TodayMissed the Tax Deadline? 3 Reasons to File Your Late Tax Return Today

Written by Hatim Dudhiyawala

Social security was introduced in 1935. However, it was never intended to be the primary source of income for retirees; rather, its sole purpose was to serve as a safety net for those unable to accumulate sufficient savings for retirement. Post-introduction, for the next several decades, the majority of Americans and non-resident aliens gave little thought to Social Security because life expectancies were short and reliance was on guaranteed pensions.

However, today things are very different. Social security benefit planning is now an essential means of securing sufficient income in retirement. In this blog guide, we will discuss strategies to maximize your Social Security benefits.

Charlotte A Dougherty, CFP, Founder of Dougherty & Associates, Cincinnati, Ohio, says that "Given today's longevity, it is more important than ever to maximize your Social Security Benefits. Think of this as an annuity for your lifetime." Along with this, David Hunter, CFP, Horizons Wealth Management, Inc., Asheville, North Carolina, says, "Social Security is the only 8% guaranteed investment around. Not only that, it is backed by the federal government."

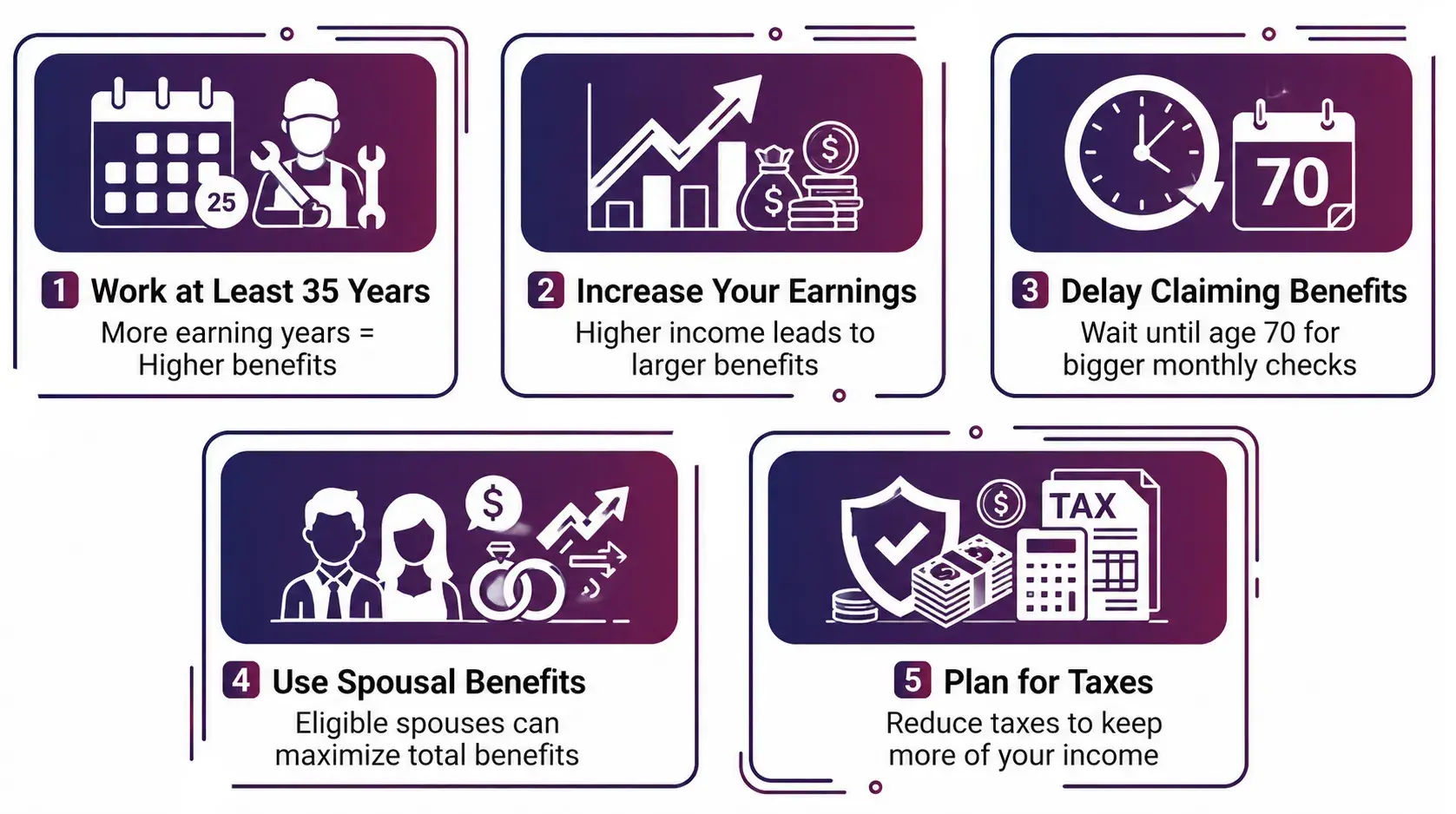

However, there are various planning options to enhance the social security benefits; they can be complicated and are only applicable in certain circumstances. The following five planning types are the ones you must know about to increase the size of your Social Security Checks.

The Social Security Administration (SSA) computes your benefit amount based on your lifetime earnings. The SSA then adjusts your earnings by indexing them to account for changes in average wages since the year you earned them. Then the SSA calculates your running total from your 35 highest-earning years and uses an average indexed monthly earnings (AIIME).

If you entered the workforce later or had periods of employment, those years will be counted as zero and incorporated into the formula, lowering the average. Once you have worked 35 years, each additional year of earnings will replace an earlier year of your lower earnings. This way, your overall average will increase and hence, your benefit.

The SSA will calculate your benefit amount based on your earnings, so the more you earn, the higher your benefit amount will be. Some pre-retirees look for ways to increase their income, such as taking on part-time work or generating business income. Others, however, are unaware of the impact on their benefits and may scale back their work or semi-retire, which can lower their Social Security income.

Marguerita Cheng, CFP, CRPC, RICP, CSRIC, CEO of Blue Ocean Global Wealth in Gaithersburg, Maryland, says, "The money earned after the age of 60 is not indexed, which means that the income earned in your 60s can replace a year in which there was a zero or a year in which you had lower earnings."

An Important Note: Earnings above the annual cap of $176,100 in 2025 and $168,600 in 2024, indexed to inflation each year, are excluded from the calculations. Ensure that your goal is to maximize your peak earnings years, striving to earn at or above the cap.

Savetaxs helps NRIs file their ITR in India under expert guidance and with 100% accuracy.

A lot of people know their full retirement age (FRA), the age at which they will receive their full Social Security Benefit. For most people retiring today, the FRA age is 67.

Now, very few people know that if they delay their Social Security Benefits until they reach the FRA, they can earn an 8% annual return on the benefits they receive. The amount of benefit increases by 8% each year if it is delayed until the age of 70. This depends on the delayed retirement credits earned for each year Social Security Benefits are delayed.

Let us understand this with an example:

Assume you are eligible for primary insurance of $2,000 or $24,000 at age 66; by waiting until age 70, your annual benefits will increase to $31,680. In other words, you will increase your total benefits from $378,000, based on your life expectancy at age 82, to $411,000.

However, this example does not fully account for COLAs (cost-of-living adjustments). For instance, a 2.5% COLA, and your deferred benefit will grow to $38,599 after four years. Thanks to compounding, you will reach $584,000 by age 82. Just keep in mind that COLAs fluctuate, going up or down. Between 2009 and 2020, there were three years when the COLA was near zero.

The COLA for 2025 is 2.5%, which is, however, lower than the 3.2% increase in 2024.

If you and your spouse were born before January 2, 1954, and have both reached full retirement age, you are eligible to claim spousal benefits while your own benefit continues to grow. And when you reach age 70, you can switch to your higher benefit. But here is one caution: which is that you cannot claim your own benefit if you want to use the "restricted application".

Savetaxs Tip:

Only the spouse and the ex-spouse born before Jan, 2 1954, are eligible to defer collecting their own benefits when they first claim the spousal benefits. For everyone else, an application for spousal benefits is treated as an application for their own benefits as well.

If you plan to supplement your retirement income by working after you start receiving Social Security Benefits, you need to be aware of the tax consequences of increasing your income. Between 50% and 85% of your benefit payment is subject to federal taxes.

To know how much of your Social Security benefits will be taxed, the IRS will add your nontaxable interest and half of your Social Security income to your adjusted gross income (AGI). If that total for single filers is $25,000 to $34,000, or $32,000 to $44,000 for joint filers, up to 50% of your Social Security Income is subject to tax. Now, when this amount exceeds $34,000 for single filers or $44,000 for joint filers, up to 85% of your benefits are subject to taxes.

You might be able to avoid paying taxes on Social Security income by considering the ways to omit information from different sources to prevent any increase that could trigger a higher tax.

James B Twining, CFP, a wealth manager at Financial Plan, Inc., Bellingham, WA, says, "Many investors have a tax penalty period between retirement and age 72. They have no earned income and are not required to withdraw from their IRAs yet. If they have a non-qualified account, they can withdraw tax-free principal. In this situation, it is quite possible that Social Security beneficiaries will be tax-free".

Savetaxs helps NRIs in the US with expert consultation on maximizing their Social Security Benefits.

These few steps will get you a long way towards her, as long as you make the most of your Social Security benefits and provide greater financial security in retirement.

It is important that investors review the changes to retirement accounts resulting from the SECURE Act. From there, you can easily analyze how to plan for your Special Security needs and the overall financial plan.

That aside, it is always helpful to review any changes in this matter with a financial professional. Such a professional is Savetaxs they will help you get the best in town to max out your Social Security checks with tailored strategies aligned with your financial and work profile.

Connect with us as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1782129946793.webp&w=828&q=75)

_1781527634459.webp&w=828&q=75)