Filing ITR with CA vs Online Platform: What's Better in 2026?

Read More

_1780663424300.webp&w=3840&q=75)

The AI-driven system of the Income Tax Department cross-checks every ITR form against data from 50+ sources. The source includes banks, mutual funds, stockbrokers, property registrars, foreign remittance records, and more. For NRI taxpayers in India, this created a unique mismatch risk: NRO interest reported on the accrual basis by the bank. TDS entries made with old PANs, overseas income data shared under FATCA/CRS, rental income reported by tenants, and more.

An unresolved income error generally triggers automatic income tax notices, delays refunds, and, in worst-case scenarios, results in a full security assessment. However, there is nothing to worry about, as this in-depth guide will show NRIs exactly how to identify, fix, and resolve any type of income mismatch.

An income mismatch generally occurs when either the income or tax credit figures that you have declared on your ITR do not match the data the income tax department has independently collected about you from third-party sources. Under Section 143(1), the ITD uses a simple automated processing system that compares every ITR information you have filed in the form against its own database, and if any discrepancy or unexplained information is found, it triggers an automatic communication or demand.

Talking specifically about NRIs, for your income matches are more frequent than they are for resident indian because of your multi-source nature of income. For example, TDS is deducted by banks, mutual fund houses, buyers, and tenants, and each of them requires filing a separate TDS return. The multi-source nature of NRI income includes income that accrues in India while an NRI lives abroad, as well as foreign assets generating data through international information exchange. Any gap between what these sources report and what NRIs declare on their income tax return is flagged.

As a taxpayer in India, before you reconcile, you must understand the three documents the Income Tax Department uses to track your income. Each of them serves a different purpose and must be checked separately before you file your ITR.

The following table clearly demonstrates the differences among the three essential documents.

| Document | What It Contains | Where To Access | Use For ITR |

|---|---|---|---|

| Form 26AS | The TDS deducted by employers, tenants, banks, and buyers, TCS collected; advance tax and self-assessment tax paid, and details of high-value transactions. Form 26AS is now being replaced by Form 168 from AY 2026-27. | incometax.gov.in - My Account - View Form 26AS (via Traces). | Use this form to verify all TDS credits you plan to claim in your ITR and ensure that your PAN number is quoted correctly in each entry. |

| Annual Information Statement (AIS) | This is a comprehensive record of all financial transactions and income sources - interest, dividends, MF transactions, foreign remittances received, property sales, salary, capital gains, and much more. This is more detailed and broader than Form 26AS. | incometax.gov.in - Services - AIS (Annual Information System). | Use to ensure you have reported all of the income sources. AIS can catch the omission that Form 26AS misses. |

| Tax Information Summary | A simplified, category-wise summary of the AIS data, including salary dividends, interest, capital gains, and more. The income tax portal will auto-populate the ITR fields using TIS data. | Same as AIS, TIS is available on the AIS portal on incometax.gov.in | You must cross-verify the auto-populated fields and their figures, and correct any incorrect TIS entries before filing. |

Note: If your Form 26 AS and AIS show different income figures from the same source, go ahead and investigate the AIS figure, as it is a more detailed and complete document. AIS encapsulated the income even where no TDS was deducted, for example, NRO savings interest below the TDS threshold, mutual fund distributions, and more. Experts recommend using the Annual Information Statement to ensure all income is reported, whereas you must use Form 26AS to verify the TDS credits and claims.

Filing ITR without checking both documents is the primary cause of automated mismatch notices.

Both NRIs and residents filing ITR in India often face general mismatch issues; however, NRIs often have a different set of mismatch triggers due to their multiple-source information profiles, non-resident status, and the way Indian financial institutions process NRI-specific transactions.

NRO FD interest - Accrual vs Receipt Basis Mismatch: Bank repeats FD interest on an accrual basis, meaning year by year as it accrues, whereas most NRIs declare it on a receipt basis only when the FD matures. This is the single most common NRI mismatch because assume that the bank reports Rs 50,000 in AIS for year 1, but the NRI declares Rs 0 (waiting for maturity). The income tax department saw this Rs 50,000 discrepancy and issued a notice.

TDS Deducted with the Wrong PAN or an Old Resident-era PAN: Buyers, banks, or tenants sometimes use an incorrect PAN (for example, due to digit transposition) when filing TDS returns. Which is why the TDS appears in someone else's Form 26AS or does not appear in yours, creating a TDS mismatch.

Rental Income Received by the Tenant But not Declared in the ITR: The tenant should deduct TDS at 31.2% under section 195 and file Form 27Q quarterly. The AIS system captures this rental income. Now, if the NRIF fails to declare it or tries to under declare it, the AIS will trigger a mismatch.

Mutual Fund Transactions Reported by RTAs (CAMS/KFintech): Mutual fund buy/sell/SIP transactions are reported to the IT department by the Register and Transfer Agents. The Redemption might appear in the AIS even if no TDS was deducted below the threshold. NRI taxpayers who forgot to declare those small redemptions generally face mismatch issues.

The Property sale proceeds reported by the Sub-Registrar: As an NRI, when you sell a property in India, the registration of your share proceeds is with the Income Tax Department. If the capital gains you have declared in the ITR do not match the sale consideration that the register returns, an income mismatch has occurred.

The foreign remittances received are reported under FATCA/CRS/FEMA: The bank received large inward remittances from abroad. If the ITR department is unable to match this remittance to a declared income or an existing source, then I may query the transactions.

Dividends From Listed Companies: Dividends from Indian companies are reported to the AIS by the company (RTA). NRIs who received dividends from indian stocks are required to declare them as they are taxable at the same rate with 20% TDS. If you miss this, it will create an AIS mismatch.

Capital Gains from Debt Mutual Fund-Section 50AA: After April 2023, debt fund gains are taxed at the same rate as income. AMCs generally replicate these transactions in AIS. NRIs who do not have a Consolidated Account Statement (CAS) and miss our reporting of these small gains will face this mismatch.

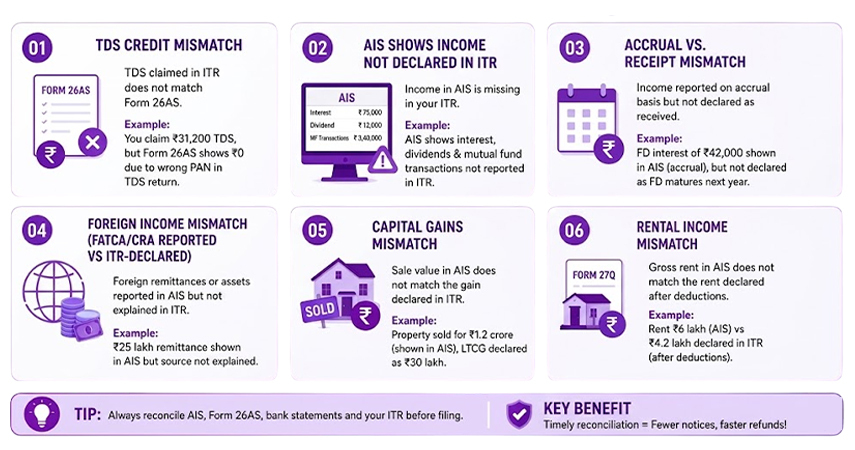

The following are the types of income mismatch that you, as an NRI, can fall into. Each mismatch has an example to help you understand it more easily.

The TDS Credit Mismatch: This generally occurs when the TDS claimed in the ITR does not match the TDS in Form 26AS. For example, you claim Rs 31,200 TDS on NRO interest in your ITR, but Form 26AS shows Rs 0 because the bank filed Form 27Q with an incorrect PAN. In such a case, you cannot claim TDS that is not in 26AS without first correcting the TDS return.

AIS shows income not declared in ITR: Also known as the income omission mismatches. Assume that your AIS shows Rs 75,000 in NRO interest, Rs 12,000 in dividend income, and Rs 3,40,000 in mutual fund transactions, but your ITR shows only Rs 75,000 in interest. The dividends and the mutual fund gains are missing from your ITR and are flagged automatically.

Accrual vs. Receipt Mismatch: To understand this mismatch, read the following example. Your bank reports Rs 42,000 of FD interest in AIS for FY 2024-25 on an accrual basis. But you then declare Rs 0 because the FD matures in FY 2025-26. Now the IT systems see those Rs 42,000 as the unreported income. Hence, the correct approach here is to recognize interest on an accrual basis.

Foreign Income Mismatch or the FATCA/CRA-reported vs ITR-declared: Assume that your NRO account received Rs 25 lakh in inward foreign remittances. The AIS will show this as a transaction, and your ITR does not explain the source. Further, if the IT department enquires about you, you will need to demonstrate that it was a capital transfer, non-taxable, and not income.

Capital Gains Mismatch: To understand capital gains mismatch, consider this example: you sold a property for Rs 1.2 crore. The sale deed is registered, and the Sub-Registrar reports Rs 1.2 crore as consideration in AIS. Now your ITR shows Rs 30 lakh as LTCG on a cost basis. The system requires matching the sale value, and your calculation worksheet must support the difference.

Rental Income Mismatch- Assume that the tenant deducts the TDS of 31.2% on Rs 6 lakh annual rent and files Form 27Q. The AIS captured Rs 6 lakh paid to you. Your ITR shows Rs 4.2 lakh (after 30% standard deductions). The mismatch is in the comparison of gross rent to the NAV figure in AIS. You must reconcile gross rents, then deductions.

With Savetaxs, get personal insight from financial experts and complete your tax obligations on time.

As a taxpayer, you must reconcile your accounts at least 3-4 weeks before filing your ITR. This allows you time for corrections at the source (deductors are correcting TDS Returns) if needed.

The following is a step-by-step approach to reconciling AIS with your income records.

From incometax.gov.in, download: (a) Form 26AS, (b) AIS PDF and JSON export, (c) Tax Information Summary (TIS), and (d) your AIS feedback report if you have submitted any of the previous corrections. Having all four essential documents in the same session will prevent confusion caused by version differences.

Gather All Source Income Documents Independently

You must collect all the source income documents, such as NRO/NRE bank statements and interest certificates; Form 16A from all TDS deductors, such as bank, mutual fund houses, bank, CAMS/KFintech CAS (Consolidated Account Statements) for all mutual fund transactions; stockbroker capital gains statement; rental agreeement and receipts; property sale deed and cost bias documents; any dividend statement from the Indian companies.

Category-Wise Comparison: Match each income head

Avoid comparing the total; compare category by category. Check: salary income, if any; NRO interests for AIS accrual vs. your records; NRE interests must not appear in the taxable AIS; dividends from each company separately; mutual fund redemption and gains; property sale consideration; rental income; and any other AIS entries. Create a spreadsheet with three columns: AIS figure, your records, and the difference.

For each mismatch, determine who is correct:

Whenever you spot a difference, you will have a question such as: Is the AIS correct, or are your records incomplete? For this, you must include the income in your ITR. Might you also think the AIS is wrong due to data entry errors in the source? For this submit the AIS feedback is to flag the errors and contact the concerned deductor to make the necessary corrections. Is the difference explainable, for example, on an accrual vs. a receipt basis? For this, you must use the accrual basis, as required by the Income Tax Act, for the interest income.

Submit AIS feedback for incorrect entries

If the AIS shows incorrect income (not your income, a duplicate entry, or incorrect amounts), you can submit feedback via the AIS portal at incometax.gov.in. Select the entry, click on "Submit Feedback", and choose the appropriate reason (for example, "Income not received" or "Amount is incorrect") and submit the feedback.

The source (bank or the deductor) must be notified. Until the AIS figures are corrected, you can file your ITR with your own accurate income and figures, but retain the documentation supporting your position.

Contact deductors of TDS return correction if needed

If TDS was deducted but does not appear in Form 26AS due to an incorrect PAN or non-filing of the TDS return, contact the deductors right away. And ask the deductor to file a correction TDS return (with Form 27Q/26Q revision) with the right PAN details. The corrections made by deductors generally appear in Form 26AS within 7-10 working days after the revised TDS return is processed by the TIN NSDL.

7: File the ITR with reconciled figures and keep full documentation

As an NRI taxpayer, file your ITR accurately and reconcile income figures. Ensure you keep a written reconciliation note in your ITR that explains every AIS entry and how it was managed, as this note will serve as your supporting document if the Income Tax Department issues a notice. Further ensure that you keep all income certificates, TDS certificates, and reconciliation records for the last 6 years from the end of the relevant AY with you.

In case of an income mismatch detection, the ITD will issue a notice. For NRIs, some of the most common notices are under Section 143(1), 143(2), and 139(9).

The following is the definition of each notice, what it means, and how to respond.

| Section | What it is | Why NRIs get it | Response Time | How to respond |

|---|---|---|---|---|

| Section 143(1) Intimation | This is an automated notice you receive after your ITR is processed. The notice states whether the tax is payable, a refund is due, or the income has been adjusted. This is not a scrutiny notice. | AIS income > ITR-declared income; TDS credit mismatch; arithmetic errors in the ITR. | 30 days from the date of intimation. | You can respond to this online through the IT portal under the "pending actions". If the demand is incorrect, you can raise an online rectification under Section 154 of the Income-tax Act. Whereas the income was genuinely missed, go ahead and file a revised ITR under section 139(5). |

| Section 139(9)- Defective Return | The notice implies that the ITR filed is defective. It's generally because mandatory schedules are incomplete, a wrong ITR form was filed, or the self-assessment tax was not paid. | NRIs receive this notice when they accidentally file ITR-1 instead of ITR-2, schedule CG for capital gains due to incompleteness, or have a residential status mismatch. | 15 days from receipt | You can file a correct return through the portal within 15 days. Just ensure not to miss the deadline. |

| Section 143(2) Scrutiny Notice | This notice is a full assessment notice, meaning the IT officer reviews your return in detail. It gets more serious when the notice is issued under Section 143(1). | NRIs generally receive such notices due to a large income mismatch arising from multiple income sources, unusual foreign remittances, high-value property transactions, or TDS mismatches on rental income. | Within the date that is mentioned in the notice. Generally, the time window is 15-30 days. | To respond, please engage a CA with experience in NRI taxation. Never ignore such a notice, as no response can lead to the best judgment assessment without your input. |

| Section 148 - Reassessment Notice | This is the notice to reopen an already completed assessment. This is issued when the IT officer has "reason to believe" income escaped assessment. | FATCA/CRA data showing unreported foreign accounts, unassessed sales shown in property registrar data, and large unexplained deposits. | As specified, it is typically 30 days. | You need CA involvement to respond to this notice, specifically a CA who is well-versed in NRI and cross-border taxation. |

If you come across an income mismatch either before or after receiving an intimation under Section 143(1), the direct solution is to file a revised return under Section 139(5). The revised return is filed to replace the original return entirely and is treated as a complete new filing.

| Feature | Details |

|---|---|

| Governing Section | Section 139(5) of the Income Tax Act, 1961. |

| Who can file | Any taxpayer who has filed the original ITR under section 139(1) or section 139(4). |

| Deadline for AY 2026-27 | December 31, 2026 ( or you can do it upon completion of the assessment, whichever is earlier) |

| Number of revisions allowed | There is no such statutory limit, which means multiple revisions are allowed before the deadline. |

| What it corrects | Any omission of income, including incorrect deduction claims, TDS credit errors, details related to incorrect tax payments, or any other mistake in the original ITR. |

| Penalty For Mistake | There is no penalty for filing a revised return. However, if additional tax is owed, interest under sections 234B and 234C applies from the original due date. |

| How To File |

To file it: Log in to incometax.gov.in - File Return - Select AY 2026-27 - Select "Revised Return" - Enter the original acknowledgment number and filing date - Complete all sections with corrected information - Verify, then submit. |

| Replaces Original | Yes, this fully replaces the original return as it is a definitive record. Ensure to keep the acknowledgment number of the revised return with you. |

Please note: File a revised income tax return proactively; do not wait for the notice to arrive.

Honestly, the most cost-effective strategy is to identify and correct the mismatches before the Income Tax Department does it for you. In case you find an error or mistake after filing yur ITR, it is better to file a revised return immediately, well before the deadline passes and the assessment begins. When you file a voluntary correction, it demonstrates the taxpayer's good faith and significantly reduces the risk of a penalty. If you wait for a 143(1) demand and then respond, you are reacting to the department; if you proactively correct, everything remains under control.

When the revised return deadline (December 31) has passed, or whenever an error or omission is found after the assessment is done, filing an updated return under Section 139(8A) is the only way out. It was introduced in 2022 and further expanded. The updated return, or ITR-U, allows taxpayers to voluntarily disclose previously unreported income and pay any additional tax liability, even after years of filing the original return.

| Feature | Details |

|---|---|

| Governing Section | Section 139(8A) of the Income Tax Act, 1961, is the governing section. |

| Time Window | Can be filed up to 48 months from the end of the relevant assessment year (extended from 24 months in the Finance Act 2025) |

| For AY 2024-25 (FY 2023-24) | The updated return, or ITR-U, can be filed up to 48 months from the end of the relevant assessment year (extended from 24 months under the Finance Act 2025). |

| Additional tax payable | 25% of the additional tax (tax + interest) if filed within 12 months; 50% if filed between 12 and 24 months; 60% if filed between 24 and 36 months; 70% if filed between 36 and 48 months. |

| Can ITR_U claim a refund? | No, ITR-U does not result in a refund or reduce the previously assessed tax liability. It can only help you disclose additional income and pay additional tax. |

| Who cannot file an ITR-U | The taxpayer against whom a search/survey is conducted. Notice under section 148 has already been issued. Along with this, taxpayers who are under prosecution or whose income involves undisclosed foreign assets. |

| Best use case for NRIs | NRIs who missed reporting NRO FD interest for the past year (before the revised return deadline passed), failed to declare rental income, or forgot to include small dividend or mutual fund gains income in the prior year's ITR. |

Please note: Under the Finance Act 2025, the ITR_U window has been extended to 48 months.

The budget 2025 extended the ITR-U filing window from 24 months to 48 months. This marks a major relief for taxpayers with historic income errors or omissions. This also means that NRIs who missed income in FY 2022-23 (AY-2023-24) can file ITR-U until March 31, 2028. The 70% of the additional tax rate for filing in the 36-38-month window is steep; however, it is far less punitive than the consequences of a scrutiny assessment that uncovers the same omission.

The tax deducted at source credit mismatch occurs when you claim a TDS credit in your ITR (let us assume Rs 31,200 was deducted by your tenant), but Form 26AS shows a different amount or nothing at all. In such a case, the Income Tax Department's automated system will reject or reduce your refund to the extent of unverified TDS.

The following are common causes of TDS credit mismatches for NRIs:

The following are tips to help you fix the TDS credit mismatch.

The following is the pre-filing reconciliation checklist for NRIs. It is advisable to complete this checklist at least 3 weeks before filing the ITR.

Connect with Savetaxs today, and let our experts help you expand your business in India.

Income mismatches are more than just a filing inconvenience for NRIs; they trigger scrutiny notices, delay refunds, and impose hefty penalties. Hence, the smartest approach is always being proactive: reconcile your AIS, Form 26AS, and income records well before filing, correct errors at the source, and file a revised return if needed.

Savetaxs has a team of experts who guide you through complex NRI tax filing, respond to IT notices, and ensure 100% compliance across both jurisdictions, making the process stress-free and straightforward.

Connect with us as we serve NRIs 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Shaw brings 8 years of experience in auditing and taxation. He has a deep understanding of disciplinary regulations and delivers comprehensive auditing services to businesses and individuals. From financial auditing to tax planning, risk assessment, and financial reporting. Mr Shaw's expertise is impeccable.

Want to read more? Explore Blogs

_1779453671986.webp&w=828&q=75)

_1779453565706.webp&w=828&q=75)

_1779712585341.webp&w=828&q=75)

_1779713772515.webp&w=828&q=75)