NRI Income Tax & Compliance

Income Tax Notice to Salaried EmployeesIncome Tax Notice to Salaried Employees

Written by Hatim Dudhiyawala

Imagine you are an NRI who has fulfilled your Indian tax obligations and is waiting for your claimed tax refund to be credited to your account. However, instead of that, you got a notice that the income tax refund was used for debts. In this situation, you get confused and tense about where your refund amount goes. If this happened to you, then do not worry, as you are not alone in this.

Like you, many taxpayers and NRIs face this situation every year, in which their claimed tax refunds are adjusted against their outstanding dues. It is known as a tax offset or tax adjustment. Yes, it is frustrating, especially when you are waiting for the money to be credited.

Confused and want to know more about the income tax refund adjustment notice and what the consequences of it are? Read the blog and get your answers.

A notice received from the income tax stating "Refund Used for Debts" simply means your tax refund is used to pay off your outstanding dues. These dues could be:

In India, a refund used for debts is done under Section 245 of the Income Tax Act 1961. Considering this, when the Income Tax Department processes your return and finds out you have an outstanding tax demand, it has the authority to adjust the refund amount against your old tax demand.

However, before they process this adjustment, they send an intimation notice under section 245 informing you about the proposed adjustment, providing you with an opportunity to express your opinion. It is not the final order of the tax official, but a communication asking whether you are okay with the adjustment or not.

This notice is available in your e-filing Income Tax Portal inbox and your registered email. So, in case you did not get the tax refund, check the mentioned things. Additionally, you can also check the refund adjustment status by clicking on "view filed returns" available on the portal. To see the full details, you can also opt for the income tax notice PDF download from the portal.

This was all about "refund used for debts," meaning. Moving ahead, let's know why your income tax refund was adjusted.

Let's be practical. Not always you will get your income tax refund into your bank account. It is because, as mentioned earlier, if you have pending tax obligations, the tax officials can adjust them. Considering this, common reasons for adjusting income tax refund are as follows:

Sometimes, even small errors such as missed interest calculations under section 234A 234B or 234C also trigger a tax demand. Apart from this, refund adjustments can also arise from reprocessed returns or rectification orders where previous underreporting has been corrected. In some cases, demands raised during scrutiny or reassessment proceedings also lead to partial or full refund adjustments.

These are some of the most common reasons why your income tax refund is adjusted. Moving further, let's know what the refund adjustment under section 245 is.

Section 245 of the Income Tax Act, 1961, gives the tax officials the power to set off a tax refund of the taxpayer against any outstanding tax demand from a previous financial year. However, they can make such an adjustment after sending an intimation notice to the taxpayer and allowing them to respond.

It is an essential procedural safeguard. Considering this, the tax department cannot simply adjust your refund without informing you. If the adjustment is made without sending an intimation notice under section 245, it is considered invalid, and on those grounds, you can raise a grievance on the e-filing portal.

Key points about Section 245 of the Income Tax Act:

Further, this income tax notice after ITR is processed, generally contains the following information:

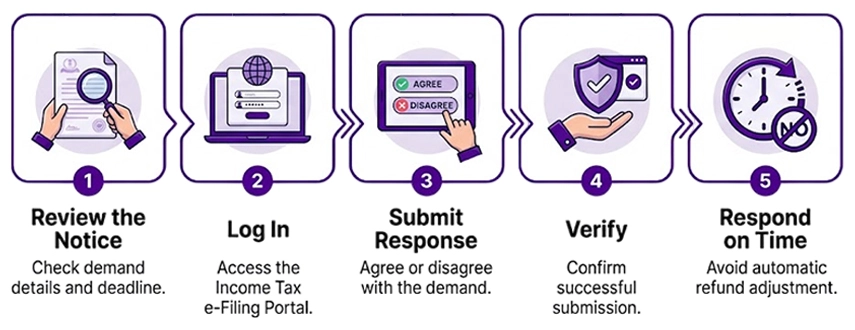

This was about a refund adjustment under section 245. Moving forward, let's know how to respond to the intimation notice sent under this section.

Under section 245, once you receive the intimation notice, carefully read it and check all the mentioned details along with the time stated to respond to the notice. It is generally 30 days from the date of issue. It is because if you do not take action on time, then the tax official considers it as if you agree with the adjustment and processed further.

Here are two possibilities: either you agree with your refund adjusted with your outstanding tax demand, or you do not.

Follow the steps below if you agree to a refund adjustment with the outstanding demand notice:

In case you do not agree/ partially disagree with the refund adjustment for the outstanding demand, follow the mentioned steps:

*For NRIs: If the outstanding tax demand relates to a year when your residential status was not clear, or if, under section 195, TDS was deducted at a higher rate than what the DTAA offers. In this situation, clearly explain why you do not agree with the adjustment and submit important documents like the Tax Residency Certificate (TRC), passport travel records, Form 10F, or details about your DTAA benefits. It is also advisable to consider taking help from a Chartered Accountant to handle this situation easily.

This is how you should respond to an income tax refund adjusted notice. Moving ahead, let's know the consequences of not responding to the section 245 intimation notice.

Not responding to the section 245 intimation notice is the most costly mistake you made. It is because the Income Tax Department treats your silence as agreement and proceeds with the refund adjustment. Additionally, beyond not getting the refund, here is what else you can face:

These are the consequences you face when you do not respond to a section 245 notice.

Let experts review your case and assist you in recovering your tax refund. Connect with Savetax and resolve it easily.

Lastly, an income tax refund adjustment notice may feel daunting, but it is simply a process where the tax department adjusts your outstanding dues. The key behind it is to know the reason, check your returns, and answer the notice on time. In many cases, you can correct the issue if you handle it properly. Additionally, ignoring may result in one of your costly mistakes.

Furthermore, if you are facing an issue in responding to the notice, connect with Savetaxs. We will provide you with expert guidance and draft an accurate response as per your situation. Our team ensures your response aligns with Indian tax law, which further removes the chances of more queries. So connect with us, and resolve your income tax issue confidently and quickly.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence.

Want to read more? Explore Blogs

_1782219386740.webp&w=828&q=75)