_1784547039242.webp&w=828&q=75)

NRI Income Tax Compliance

30+ Important Income Tax Terms in India You Need to Know30+ Important Income Tax Terms in India You Need to Know

Written by Shubham Jain

Generally, it happens that we might miss out on details and make some errors while filing income tax returns. These errors make your return "defective.". This is when you are issued a notice of defective return under section 139(9).

Section 139(9) of the Income Tax Act, 1961, explains that when your return is found defective, the assessing officer generally grants you a period of 15 days (or the time specified in the notice) to rectify such errors. It is like a warning to taxpayers, allowing them to rectify errors and ensure accurate reporting. You need to respond to such notices quickly to avoid penalties, interest, or issues with refunds.

In this blog, we will understand the different reasons why you might get a defective return notice. Also, we will walk you through how to respond to a defective return under Section 139 (9).

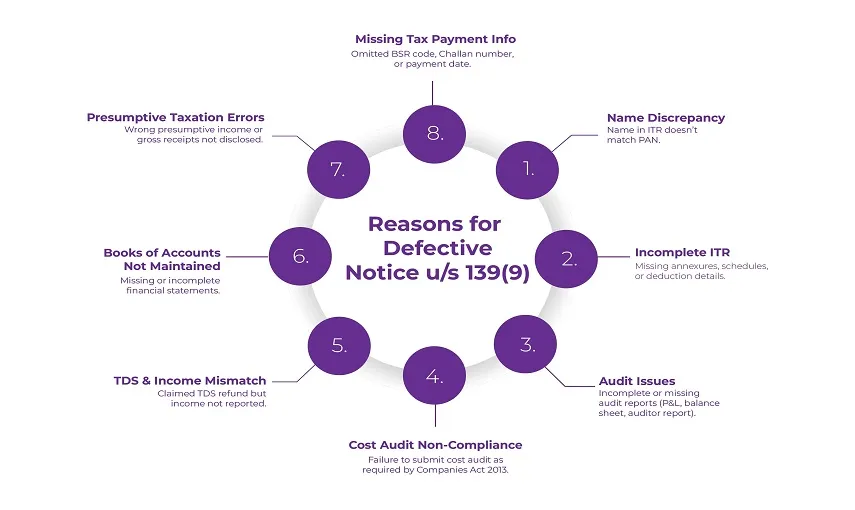

An income tax defective return notice is issued when the Income Tax Department finds errors or inconsistencies in your ITR. The main aim behind issuing this notice is to ensure that your ITR contains accurate and complete information. Some common errors could include:

In any of the above-mentioned cases, the income tax department will issue an income tax defective return notice u/s 139(9) to the taxpayers. The notice will inform them about the same and ask them to rectify the errors made in the return.

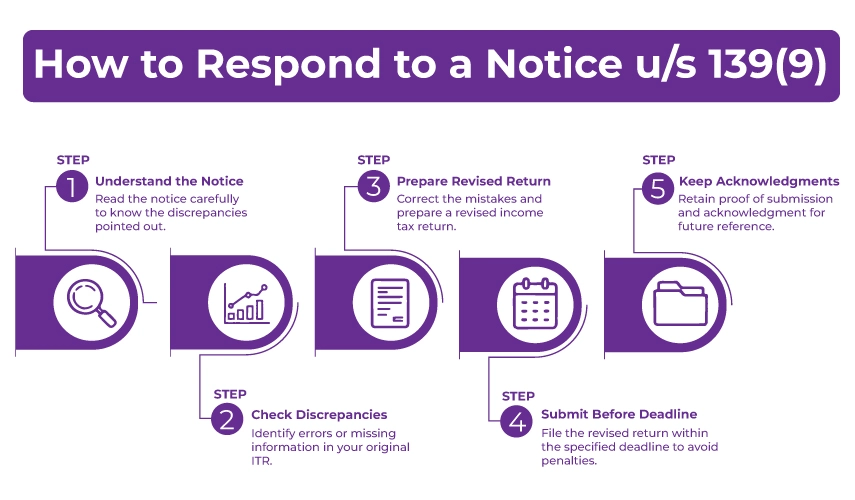

The notice will be sent to your registered email ID and can also be accessed through the Income Tax e-filing portal. After receiving the notice, you need to correct the defects and re-submit the return within 15 days (or the time allowed in the notice). In case you fail to rectify the errors on time, you might face consequences later.

Let's now discuss the reasons for receiving a defective notice 139 (9) in detail.

Section 139(9) of the Income Tax Act applies to both residents and NRIs when their income tax return (ITR) is considered defective due to errors or omissions. Common causes include mismatches in income and tax details, missing audit reports where applicable, or incomplete disclosure of income. Taxpayers generally get a 15-day window after receiving the notice to correct these defects, helping them avoid penalties and ensure accurate tax compliance in India.

The assessing officer may consider the following reasons, mistakes, or omissions while issuing an income tax defective return notice under Section 139(9):

Upon receiving a notice of an income tax defective return notice u/s 139(9), you need to revise your return within 15 days of the notice's receipt by the Income Tax Department. Alternatively, you can request an extension by submitting a written application to the Assessing Officer (A.O.). You can ask for more time to file a revised return.

It is often observed that even if a taxpayer rectifies the defect after the 15-day duration, the AO may still condone the delay and treat the return as valid. It applies if it is done before the assessment is finalized.

However, if you don't respond within 15 days, you can request an additional extension to make the revisions. If your extension request is denied, the original return will be considered invalid. This situation could lead to consequences like accruing interest, not being able to carry forward losses, facing penalties, and losing specific exemptions.

If you fail to respond to a defective return notice under Section 139(9) or to revise your income tax return (ITR) within the specified timeframe. Then, it will result in your defective return being classified as a non-filed or invalid return. The Income Tax Department will view this as if you have not submitted a return for that year. Consequently, it means that any potential refund you are due will not be processed.

If your original ITR is deemed invalid, you can still file a belated return. However, this will incur a penalty fee to minimize further repercussions.

You will get the notice u/s139(9) from the Income Tax Department via the email address you provided while filing your ITR. These notices typically come from the CPC. Also, the subject line will read "Communication u/s 139(9) for PAN AWZXXXXXXX for the A.Y. 2024-25".

The notice is attached to the email and is password-protected. To open it, the password is your PAN in lower case, and your birth date in the format DD/MM/YYYY.

For example,

If your PAN is ABCDE1234F and your birth date is 01/01/2001, then the password to open the defective return notice will be abcde1234f01012001.

To respond to an income tax notice, you can visit the income tax department's website and log in using your credentials. Here is a quick guide on how to address Income Tax Notices:

When you receive a defective notice, you have 15 days from the date of receipt. Also, you have the time frame specified in the notice to rectify the mistakes in the return you have filed.

Previously, it was possible to withdraw a response submitted for a defective notice under Section 139(9). However, this option is no longer available. Now, you cannot withdraw your response; however, you can either update or view it.

It is essential to respond promptly and accurately to a defective return notice. You can seek advice from an expert regarding the same.

According to Section 139(9) of the IT Act, taxpayers have the right to revise their ITRs. This provision allows for the rectification of unintentional errors or omissions, even after a notice under Section 139(9 of the Income Tax Act) has been issued.

Revisions can take place before the one-year mark from the end of the relevant assessment year or before the completion of the assessment year, whichever comes first. This flexibility enables taxpayers to address discrepancies and ensure accuracy in their tax filings.

You need to understand that receiving a tax notice is not a cause to panic or worry. Instead, you must see it as an opportunity to correct any errors made in your original income tax return. Taking action on time can protect you from facing potential penalties, loss of benefits, and scrutiny.

However, if you are someone who finds tax and tax-related issues complicated, seek assistance from a professional like Savetaxs. At Savetaxs, we have a team of experienced CAs and tax professionals carrying years of experience. They actively work 24*7 across all time zones to ensure timely and satisfactory assistance.

Our team ensures to provide you with personalized assistance as per your situation. No matter which country you are in and what tax issues you are facing, contact us right away.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784546974133.webp&w=828&q=75)

_1784376356528.webp&w=828&q=75)

_1784375756402.webp&w=828&q=75)