_1770208774564.webp&w=828&q=75)

NRI Home Loan Vs Normal Home Loan

Read More

_1770034387593.png&w=3840&q=75)

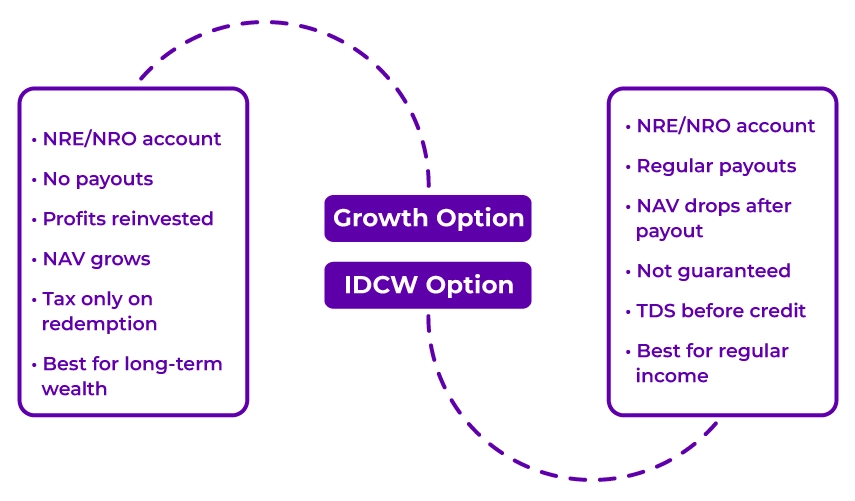

Between Growth vs IDCW mutual funds, NRIs often remain confused. Opting between Growth and IDCW options in mutual funds significantly impacts your returns from long-term investments. It is because in the Growth options, your profit is reinvested into your investment to create capital. In contrast, in the IDCW options, you get regular payouts that might involve your invested money.

In this blog, learn about the key differences between growth and IDCW mutual fund options for NRIs. Additionally, know how these investments work, their tax implications, and more, and maximize your tax returns by choosing the right investment.

Before moving on to the key difference between Growth vs IDCW mutual funds, let's first understand their meanings.

The Growth option in mutual funds is straightforward. In this investment option, all your profits stay invested in the funds. Additionally, during the holding periods, you do not get any payouts.

Considering this, when the fund obtains dividends from the stocks it holds, capital gains from selling securities, or interest from bonds, all of these are reinvested. This, over time, increases the Net Asset Value (NAV) of the funds.

Further, let's know the key features of the Growth option:

IDCW stands for Income Distribution cum Capital Withdrawal. Before April 2021, it was known as the "Dividend Option." This investment option provides your earned profits at set times. You can get the distribution yearly, quarterly, or monthly, based on what the investment scheme offers to you.

Additionally, these investments pay you either by selling some of its securities or from its collected profits. Further, let's know the key features of the IDCW option:

This was all about Growth and IDCW mutual funds. Moving ahead, let's look at the key differences between these investment options.

The table below, detailed comparison of Growth vs IDCW options in mutual funds:

| Basis | Growth Option | IDCW Option |

|---|---|---|

| Payment of Profits | Profits are reinvested, over time, allowing full compounding. | Profits are paid out as dividends, reducing compounding. |

| NAV Impact | Since no money is taken out over time NAV increases. | After every payout, NAV falls, so it stays lower. |

| Return Potential | In the long run, returns are higher because of the uninterrupted growth. | Due to interrupted compounding, generally, returns are lower. |

| Risk | Since the complete capital stays exposed to market fluctuations, the growth option contains a higher risk. | IDCW consider as lower risk as regular payouts offer an income cushion. |

| Liquidity | Liquidity only happens during redemption. | Through periodic payments, it provides higher liquidity. |

| Payout | With long-term appreciation potential, it directly showcases the market performance. | Payouts depend on fund performance. Additionally, these are not guaranteed. |

| Tax Efficiency | Growth provides better tax benefits as taxes are imposed only when you sell securities. | In IDCW, tax is imposed immediately as per your tax slab before payout. |

So, this was all about the key difference between Growth vs IDCW mutual funds. Moving further, let's know how the Growth option works for NRIs.

To start mutual fund investments, NRIs need the correct banking infrastructure. Considering this, first, to manage your investments, you will need an NRE or NRO account. Furthermore, let's explore the investment process.

To get started, you need to submit some documents to complete your KYC. These include:

Using the online platforms, you can start investing.

By reinvesting capital gains back into the funds, growth plans generally offer higher returns. So you can enjoy the compounding impact on your investments.

Growth plans offers wealth build options to NRIs. These are also tax-efficient as taxes are paid at the time of redemption. Additionally, over time, your returns compound get better.

This is how growth investment plans work for NRIs. Moving ahead, let's know how the IDCW option works for NRIs.

Under the IDCW option, a part of the profits from mutual funds, instead of reinvestment, is distributed to investors. For NRIs, investing in IDCW mutual funds can be made through NRE or NRO accounts after KYC. Additionally, the income is directly credited to their linked bank account after applicable tax and TDS deduction as per Indian tax laws.

In the IDCW investment options, there are no guaranteed payouts. Its payments depend on the fund's performance and the decisions of fund houses. These payouts are made from the scheme's distributable surplus. Additionally, it may include both capital and income.

Considering this, NRIs can either:

So this is how the IDCW option works for NRIs. Moving on, let's look at the tax implications for NRI investors.

With Savetaxs, file your ITR with 100% accuracy and get help for capital gains, income, and compliance.

Taxation is where IDCW and Growth split dramatically, specifically for NRIs.

In India, payouts from IDCW are treated as "Income from Other Sources." They are added to investors' total income and taxed at the applicable slab rate.

Additionally, under section 196A of the Income Tax Act, for NRIs, before paying the IDCW, the fund house deducts 20% TDS. For instance:

Further, if your actual tax liability is less than 20%, by filing an ITR, you can claim a refund. However, this needs some extra effort and a wait for a refund.

With growth investments, you only pay tax when you redeem units. In this, the tax rate depends on your fund type and holding period. Considering this, for equity funds for the Financial Year (FY) 2025-26, the tax rate is:

| Holding Period | Tax Type | Rate |

|---|---|---|

| Less than 12 months | STCG | 20% |

| More than 12 months | LTCG | 12.5% (more than INR 1,25,000) |

Additionally, as per the changes in the Union Budget 2024, regardless of holding period, all capital gains will be taxed as per your slab rate.

Further, with growth mutual funds with annual tax drag, your full capital keeps compounding. However, with IDCW mutual funds, every time a payment is made, you pay tax. It decreases the amount of future growth.

Moreover, for an NRI who is in the tax bracket of 30%, obtaining INR 1,00,000 in IDCW annually, each year INR 30,000 is gone. Over 10 years, this amount outcomes into a significant sum.

So, this was all about the taxation difference NRIs face in Growth and IDCW mutual funds. Moving ahead, let's discuss the NRI-specific considerations for Growth vs IDCW.

When deciding between Growth and IDCW, NRIs faced unique factors. These are as follows:

So, this was all about NRI-specific consideration for Growth vs IDCW. Moving further, let's know how NRIs should choose between these two mutual fund investments.

Among the Growth and IDCW mutual funds, NRIs should choose the one that matches their investment goals, risk appetite, and time horizon. Further, let's know about this in some detail:

Moreover, for most NRIs, the Growth mutual fund is clearly a suitable investment option. The tax efficiency and compounding benefit make this investment a perfect choice for wealth building.

Lastly, the Growth vs IDCW mutual fund choice is not so complicated. For the majority of investors, specifically for NRIs, Growth is the superior option. These options over long runs offer better returns, especially through NRE accounts that allow you to transfer funds without restriction. In contrast, IDCW plans are a good option if you prefer getting a regular income more than increasing your returns. Additionally, compared to IDCW, these plans generally provide tax and compounding benefits that create more value.

Furthermore, if you are still confused about choosing the right investment, connect with Savetaxs. Our financial experts will help you in opting for the correct NRI investment option as per your investment goals, time horizon, and risk appetite. Additionally, if you want, they can also assist you with your tax planning in India.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Manish is a financial professional with over 10 years of experience in strategic financial planning, performance analysis, and compliance across different sectors, including Agriculture, Pharma, Manufacturing, & Oil and Gas. Mr Prajapati has a knack for managing financial accounts, driving business growth by optimizing cost efficiency and regulatory compliance. Additionally, he has expertise in developing financial models, preparing detailed cash flow statements, and closing the balance sheets.

Want to read more? Explore Blogs

_1770293198608.webp&w=828&q=75)

_1770382757472.webp&w=828&q=75)