Best Index Funds For NRIs In India 2026

Read More

Thematic funds are a category of mutual funds that focus on specific themes or trends in the market. Unlike traditional classification methods like market capitalization or investment styles, thematic mutual funds focus on companies that are tied by a specific idea or concept.

It can include clean energy, digital India, or broader rural development themes spanning multiple sectors. These funds carry moderate to high risk based on the assets and sectors in which they invest. In this blog, we will cover everything that an NRI needs to know before investing in thematic mutual funds.

Thematic mutual funds are mutual fund schemes that focus on specific themes or trends, such as clean energy or technology. It invests in companies from different sectors that are all connected by a specific theme. The investment strategy of these funds depends on factors such as economic conditions, industry outlook, and emerging market trends.

Fund managers of thematic funds monitor changes in consumer behaviour, the regulatory environment, and technological developments to align with the fund's strategy and capitalize on future growth.

Thematic mutual funds offer several benefits that are tailored to the needs of an NRI. Here are some of the benefits of a thematic mutual fund, which makes them a preferred choice amongst NRIs:

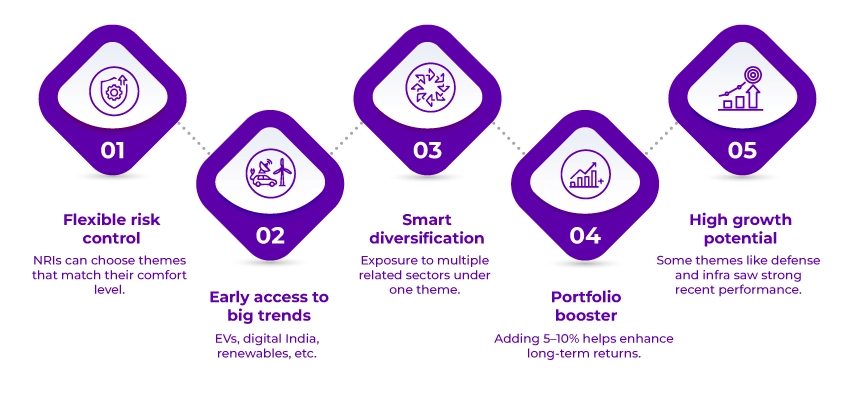

The Investor has the option to adjust their risk exposure within the themes depending on their comfort level. It gives NRIs control over their portfolio risk within themes.

These funds allow you to invest early on emerging trends before they reach mainstream adoption, like renewable energy, digital transformation, or electric vehicles. This will help you in positioning your portfolio to benefit from the developing market trends that may take several years to mature completely.

Thematic mutual funds offer exposure to multiple related sectors, helping in reducing dependence on a single industry's performance while also providing targeted investment. A manufacturing-themed fund might include stocks from the construction, chemicals, and engineering industries.

Allocating 5-10% of your portfolio to thematic funds can create better returns without risking core diversification. This allows you to maintain a core diversified approach while adding focused exposure to specific growth areas.

You can enjoy exceptional returns if you opt for the right themes. Recent funds focused on defense, infrastructure, or technology have returned 60-77% every year. (Such high returns may not be consistent or guaranteed).

NRIs get a variety of thematic fund options to choose from. These options are aligned with the current Indian economic priorities. Here are some of the popular thematic fund themes for NRI investors:

Yes, there are risks associated with investing in thematic funds. The following are some situations where thematic investing can be a bad idea for NRIs:

We offer expert services to ensure easy NRI ITR filing.

Thematic funds follow equity taxation rules as they are equity-oriented funds. Here is how it is taxed:

Let's understand this clearly with the help of an example:

In January 2023, you invested Rs. 15 lakh in the Solanki Infrastructure Fund. Since it has a holding period of 26 months, by March 2026, your investment will grow to Rs. 22 lakh.

So, your long-term capital gain will be Rs. 7 lakh. If we calculate the tax,

Since the first Rs. 1.25 lakh is tax-free, the remaining Rs. 5.75 lakh will be taxed at 12.5%.

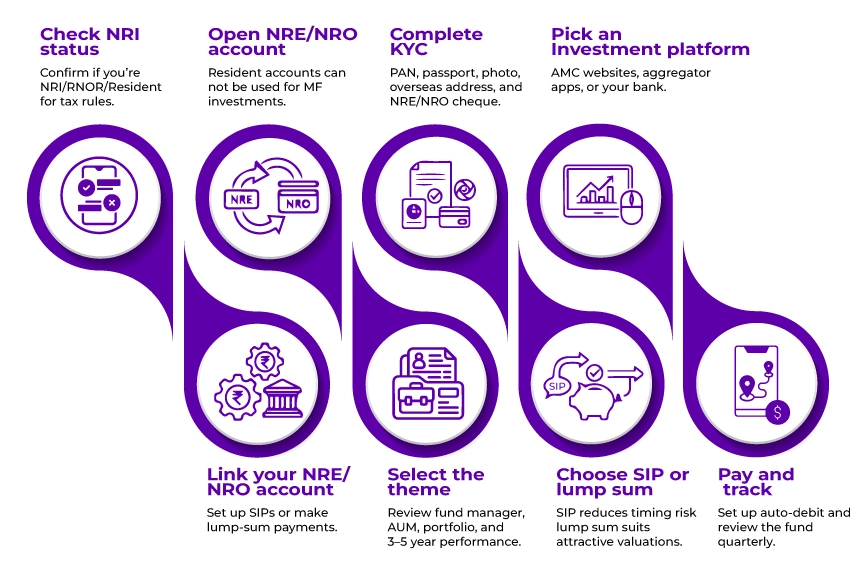

An NRI can invest in thematic mutual funds by following the steps mentioned below:

Check your Residential Status and determine if you are classified as NRI, RNOR, or resident for tax purposes. Your residential status will affect your tax liability and ITR filing requirements.

You need either an NRE or an NRO account, as you are not allowed to invest in thematic funds through your old resident savings account.

For completing KYC, you will need the following documents:

The following are three options that you get to invest in a thematic mutual fund, along with their benefit and drawbacks:

| Option | Where to Invest | Benefit | Drawback |

|---|---|---|---|

| Direct Fund House Website | Invest directly on AMC websites such as ICICI Prudential, HDFC, and SBI Mutual Fund by registering as an NRI investor. | Lower expense ratio (direct plans vs. regular plans). | You must manage multiple fund houses separately. |

| Aggregator Platforms | Platforms like Zerodha Coin, ET Money, INDmoney, and Groww (Groww accepts most NRIs except those in the US & Canada). | Single dashboard to manage multiple funds. | Some platforms apply FATCA-related restrictions. |

| Through Your Bank | Invest via wealth management portals of banks where you hold an NRE/NRO account—ICICI, HDFC, Axis, SBI. | Convenience of managing investments within your existing banking relationship. | May have higher charges or limited fund options. |

Once you have selected the platform, the next step is to link your NRE or NRO account. You will receive a small test transaction from the platform for verification.

Upon verification, you can set up:

You can research the best option using:

To research, check the following things:

Ease your tax burdens and minimize deductions with the help of professionals.

Ensure to authorize an auto-debt mandate for SIPs. The funds will be transferred automatically by your bank every month.

For a lump sum, you can make the payment through:

You need to keep monitoring your fund every day or week, as thematic funds are volatile and daily monitoring can be stressful. Instead of keeping track every week, review it quarterly and check the following things:

Thematic mutual funds are types of equity funds that invest in a specific theme, such as ESG investing, green investing, or infrastructure development. Thematic funds are ideal for experienced investors who can tolerate high risk and have a long-term investment goal. Additionally, to avoid any kind of confusion, it's ideal to contact the experts at Savetaxs. We have an entire team of experts who can help you understand the implications for your personal financial situation. Contact us anytime, as we are working 24*7 across the globe.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Want to read more? Explore Blogs

_1777034893472.webp&w=828&q=75)