NRI Banking Services

Top 10 Best Bank Accounts in GIFT City for NRIsTop 10 Best Bank Accounts in GIFT City for NRIs

Written by Shubham Jain

NRIs who wish to maintain a fixed deposit account in India can opt for an FCNR account. The account enables you to park money earned abroad in foreign currency in India. Most banks in India allow FCNR deposits in permitted foreign currencies such as US Dollars (USD), Pound Sterling (GBP), Euro (EUR), Japanese Yen (JPY), Australian Dollars (AUD), and Canadian Dollars (CAD).

For a Non-Resident Indian, an FCNR account is an efficient investment option if they wish to retain their money in foreign currency and earn returns without exposure to Indian rupee exchange fluctuations. Since deposits are maintained in foreign currency, there is no currency conversion risk during the deposit tenure.

In this blog, we will explore how income from FCNR accounts is taxed in India, the impact of residential status on taxation, and compliance considerations.

FCNR stands for Foreign Currency Non-Resident Account. It is a fixed-term deposit account, not a regular savings account. NRIs can deposit foreign income in this account, and the funds remain in the same foreign currency denomination.

This protects the deposit from exchange rate fluctuations between foreign currency and the Indian rupee during the tenure of the deposit.

Key features:

Tenure: 1 to 5 years

If a deposit is withdrawn before completing one year, no interest is payable.

Savetaxs offers end-to-end guidance in opening an FCNR account online in India.

As per the provisions of the Foreign Exchange Management Act (FEMA), 1999, the following individuals are eligible to open an FCNR account:

The account can be opened:

In case of joint accounts, the joint holder must also qualify as a non-resident under FEMA regulations. However, nomination can be provided in favor of a resident relative.

Funds can be credited to an FCNR account through:

Account opening can be completed from overseas by submitting KYC documents such as passport copy, visa/residence proof, overseas address proof, and foreign bank account details.

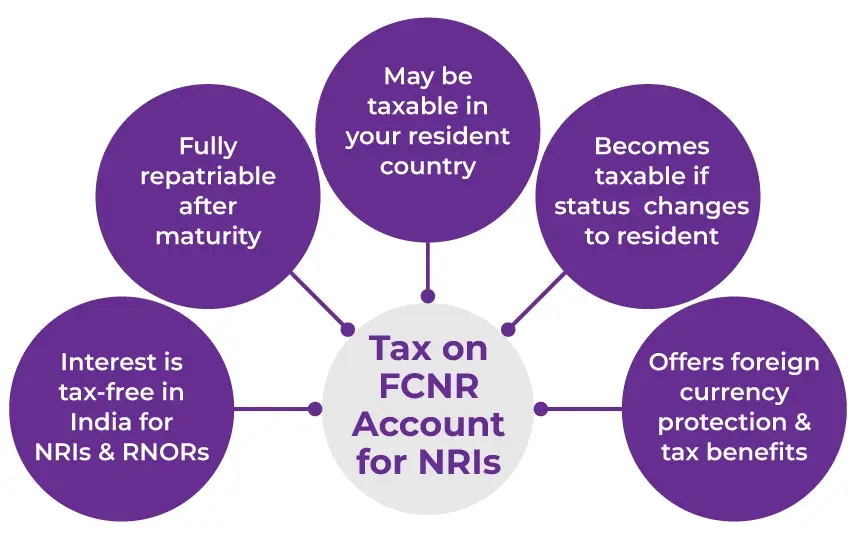

Interest income earned on an FCNR deposit is exempt from tax in India under Section 10(4)(ii) of the Income-tax Act, 1961.

This exemption is available provided the account holder qualifies as:

During this period:

The exemption is status-dependent. It is not account-dependent but person-dependent.

Residential status under the Income-tax Act determines taxability.

Once your status changes to Resident (Ordinary Resident):

However:

It is critical to understand that residential status under FEMA and residential status under the Income-tax Act are determined separately. Taxability is governed strictly under the Income-tax Act.

While FCNR interest is exempt from tax in India (subject to status), it may be taxable in the country where the NRI resides. The taxability depends on:

NRIs should evaluate foreign reporting requirements carefully, especially in countries with worldwide income taxation systems.

Interest rates on FCNR deposits:

Generally:

Interest income, along with the principal amount deposited, is fully repatriable outside India without requiring prior approval from the Reserve Bank of India, subject to regulatory compliance.

In the unfortunate event of the death of the primary NRI account holder, the funds can be transferred to the nominee’s account in accordance with banking regulations and tax provisions.

Interest earned may be credited to an NRE or NRO account, depending on instructions provided to the bank.

The following table compares the taxation of FCNR, NRE, and NRO accounts.

| Comparison Factor | FCNR Account | NRE Account | NRO Account |

|---|---|---|---|

| Interest Taxability | Exempt in India (for NRI/RNOR) | Exempt in India (for NRI) | Fully taxable in India |

| TDS | Not Applicable | Not Applicable | Applicable |

| Currency Risk | No (foreign currency maintained) | Yes (INR-based) | Yes (INR-based) |

| Repatriation | Fully Allowed | Fully allowed | Restricted and regulated |

From a tax efficiency standpoint, both NRE and FCNR accounts are advantageous for NRIs. However, FCNR accounts offer an additional benefit of eliminating exchange rate risk during the deposit tenure.

Although FCNR interest is exempt from income tax in India (subject to status), compliance obligations still exist.

NRIs and returning residents should maintain:

Proper documentation is essential for supporting tax positions during assessments.

Savetaxs offers expert-led, accurate NRI ITR filing on time.

FCNR accounts may offer relatively lower interest rates compared to certain resident deposits. However, they provide significant advantages, including:

The most critical factor while evaluating taxation is your residential status under the Income-tax Act, 1961. Tax treatment changes immediately when your status changes.

As an NRI, misclassification of residential status can result in incorrect tax treatment and potential compliance issues.

If you are unsure about:

Professional guidance is strongly recommended.

Savetaxs provides expert-led NRI tax advisory, residential status determination, and end-to-end NRI ITR filing services. We assist NRIs across multiple jurisdictions with structured compliance support aligned with Indian tax laws.

Connect with our team for accurate, compliant, and timely NRI tax assistance.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1784120197435.webp&w=828&q=75)

_1783598615351.webp&w=828&q=75)