NRI Banking Services

Top 10 Best Bank Accounts in GIFT City for NRIsTop 10 Best Bank Accounts in GIFT City for NRIs

Written by Shubham Jain

An NRI's NRE account loses its tax-free status in India as soon as their residential status changes from Non-Resident Indian to Resident in India as per the provisions of the FEMA (Foreign Exchange Management Act). A person is considered an Indian resident under FEMA when they return to India to stay permanently, such as for employment, to start a business, or a profession, etc. In this blog, we will learn about an NRE account, RNOR status, and when an NRE account loses its tax-free status.

An NRE (Non-Resident External) account is for NRIs to keep their foreign earnings in India. It is a rupee-denominated account where you can deposit money in foreign currency. However, withdrawals can be made only in Indian rupees.

An NRE account can be opened in the form of savings, current, recurring, or fixed deposits. Repatriation of both principal and interest amount from an NRE account to a foreign account can be done without any restrictions.

Under the FEMA (Foreign Exchange Management Act), the interest earned on an NRE account is tax-exempt for a Non-resident. You can keep holding an NRE account until you qualify as a non-resident under FEMA, and not beyond that.

You will be deemed an Indian resident under FEMA after you move back to India for employment, business, profession, or to stay there for an indefinite period. When you move back to India permanently, you will be considered a resident starting from the day you arrive there. This is regardless of how long you stay there.

You must notify your bank about the residential status change, and the bank will then Redesignate your existing NRE account as a regular resident account. This change will help you in reporting tax accurately because interest earned on the account will be subject to taxation in India once you move back.

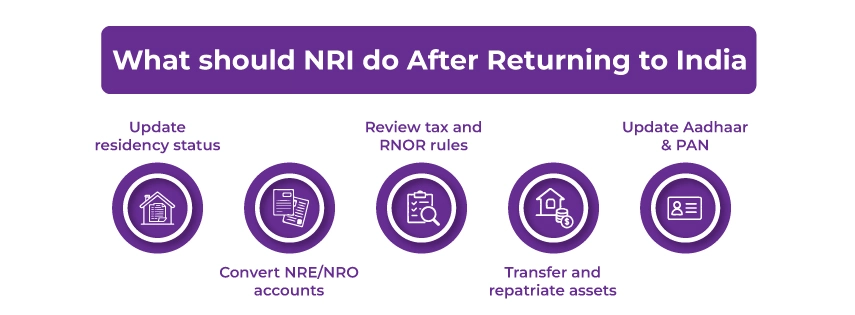

Follow these steps after arriving in India to ensure compliance and a smooth transition to India:

Inform your bank promptly about the change in your residential status. The bank will help you to:

An RFC (Resident Foreign Currency) account permits the NRIs returning to India to hold funds in foreign currencies, such as USD, GBP, or EUR.

The interest earned on an NRE deposit will be taxed at the applicable slab rates upon becoming an ROR (Resident and Ordinarily Resident). You can still avail the tax benefits available under the RNOR status for 2-3 years after moving back to India.

Suppose, after spending 10 years abroad, you came back to India in October 2025:

The RNOR status is a special residency status category under the Indian tax law, specifically for individuals coming back to India after spending years abroad. This status provides them with limited exemptions from tax on their global income during the transition phase. Also, ensures that your foreign income is not taxed immediately in India. You will be considered an RNOR if:

Here are some tips to help NRIs who are returning to India after spending years abroad:

The NRE account loses its tax-free status in India from the moment you become an Indian resident under FEMA. NRE account remains tax-free in India only until you qualify as an NRI. You need to either convert your NRE account to a resident account or repatriate the funds to a Resident Foreign Currency (RFC) account.

If you still have any more questions or are confused about understanding the status, consider the experts at Savetaxs. We have an entire team of experts who will guide you in understanding the complexities of transitioning to India.

They will help you determine your tax obligations and help you with NRI financial planning when you move back to India. Contact us right away, as we are working 24*7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784120197435.webp&w=828&q=75)

_1783598615351.webp&w=828&q=75)