US Tax Forms

IRS Form 8865: Foreign Partnership ReportingIRS Form 8865: Foreign Partnership Reporting

Written by Hatim Dudhiyawala

As an NRI in the United States, if your parents, relatives, or family back in India have given you a significant gift- money, property, or assets. There is a US tax form you need to know about: Form 3520.

Many NRIs assume that because gifts from family are not taxable income, there is nothing to report. The assumption is wrong, and it is one of the most common and costly compliance gaps among Indian-origin taxpayers in the US. Form 3520 is not about you paying the taxes; instead, it is about the disclosure, and slipping on it might carry some of the harshest penalties in the entire US tax code.

This structured guide will explain everything about the Form 3520 foreign gift reporting instructions, including documentation, reporting requirements, and the filing process.

The IRS Form 3520 is officially an "Annual Return To Report Transactions with Foreign Trusts and Receipt of Certain Foreign Gifts". This form is an informational return that US persons file to report specific transactions involving foreign entities and individuals.

The IRS reviews this form to ensure and maintain transparency in foreign trusts, foreign assets, and international transactions for tax purposes. It further helps the IRS track money, assets, and property received from foreign persons, corporations, partnerships, or estates.

The form covers three broad categories:

For most NRIs, the relevant trigger is the first category: receiving a significant gift from their family in India.

The critical thing to understand here is that Form 3520 does not create any tax liability; a gift received from an individual in India is generally not treated as taxable income to the recipient under US law. Form 3520 is purely a reporting requirement because the IRS wants visibility into the large cross-border financial movements, even when no tax is owed on them.

With Savetaxs, you get expert insight into your tax situation from the best CAs and CPAs, ensuring your taxes are filed accurately.

You must file Form 3520 if you are a US person, meaning a citizen of the US, green card holder, or someone who has met the substantial presence test, and during the tax year you must.

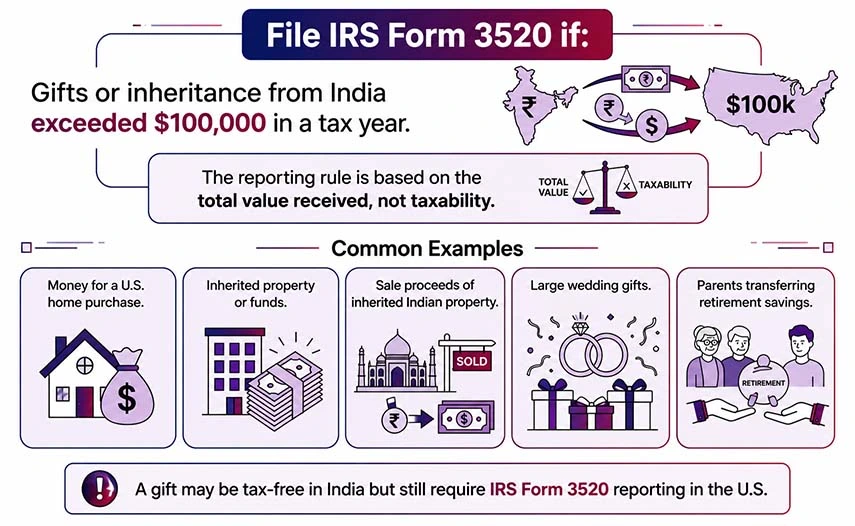

For NRIs specifically, the most common situation by far is the first one: receiving money or property from parents, grandparents, or other close relatives in India that crosses the $100,000 threshold in a single tax year.

An important aggregation rule: In case you end up receiving multiple gifts from different individuals who are related to each other, for example, Rs 50 lakh from your father and Rs 40 lakh from your mother in the same tax year. This way, the IRS might require you to aggregate gifts from related persons while determining whether or not you have crossed the $100,000 threshold. You must confirm the specific aggregation rules with a US CPA, as they affect whether reporting is triggered.

The reporting trigger is based on the value of gifts received during a single tax year, not on whether the gift itself is taxable.

Here is a quick answer: If you are a US tax resident and received gifts or inheritance from individuals in India totaling more than $100,000 in a year, you must file Form 3520 with your annual tax return even though the gift itself isn't taxable.

Common situations that trigger this for NRIs:

A common misunderstanding is that many NRIs often believe that because the first was already taxed in India (or wasn't taxed because gifts from specified relatives are exempt under the Indian tax law), there is no US obligation. This is an incorrect notion. The Indian tax treatment and US reporting obligations are entirely separate. A gift can be completely tax-free in India and still require disclosure on Form 3520 in the United States.

The following is a detailed breakdown of how to complete the Form 3520 accurately. However, for NRIs, it is highly advisable to seek help from a tax professional and let them handle this crucial part.

You will need your

To begin with, enter the basic details:

If your filing involves a foreign trust, complete the following details.

If you have received a foreign gift or inheritance, complete this section.

This ensures complete and transparent reporting of the foreign gifts.

Summarise your totals.

This section helps to clarify the complex transactions and supports your figures.

Before you submit the 3520 form,

The Form 3520 is filed separately with your Form 1040 by the assigned deadline.

Although most NRIs use Form 3520 for gift reporting, the form also covers transactions involving foreign trusts, a category that often affects NRIs with family wealth structured through Indian trust arrangements.

If you are the grantor of a foreign trust, or if you transfer property to a foreign trust or receive distributions from a foreign trust, you should report this on Form 3520. This is applicable when the trust is a family trust established in India for estate planning, rather than a typical commercial trust.

US grantor rules can be overwhelming if you have created or contributed to a trust in India (at times done as part of family estate planning); you might be considered the owner of that trust for US tax purposes, with the annual reporting obligations that just go beyond the simplest gift disclosure. This is the area where the line between gift and trust transactions often blurs, and the guidance of a tax professional matters.

The Form 3520 is often confused with the similarly named Form 3520-A. The following table differentiates between the two forms.

| Topic | Form 3520 | Form 3520-A |

|---|---|---|

| Primary Filer | US individual or estate executor | The foreign trust, signed by the trustee. |

| Main Purpose | Reports the trust transactions, ownership, and certain large cross-border transfers. | Provides the annual trust information and the required statements. |

| Typical Trigger | Receipt of reportable foreign gifts or bequests, transfers to foreign trusts, and distributions from foreign trusts. | Ongoing US ownership of a foreign trust under the IRC 671-679. |

| Timing Focus | Based on the taxpayer's filing calendar (4th month after year-end with expat timing rules and applicable due dates). | Based on the tax year of the trust (3rd month after the trust year-end with its own extension form) and its own deadline. |

| Penalties | Start at $10,000 up to 35% of unrepatriated income or 25% of unrepatriated gifts. | $10,000 or 5% of the assets attributable to a US owner. |

Understanding the different matters is important because missing either form can result in penalties when the underlying transaction is not taxable.

This is where Form 3520 becomes genuinely high-stakes. The penalty structure is among the most severe in the US tax code.

Other penalties may apply after 90 days if you did not respond to the IRS notice sent to you. Demonstrating reasonable cause can help reduce these fines. That is, if you have missed filing Form 3520 for a gift received in a prior year, the IRS Streamlined Filing Compliance Procedures may offer a path to catch up with reduced penalty exposure, but eligibility does depend on the noncompliance being nonwillful. It is highly advisable to speak to a US CPA before attempting any late or diligence filing on your own.

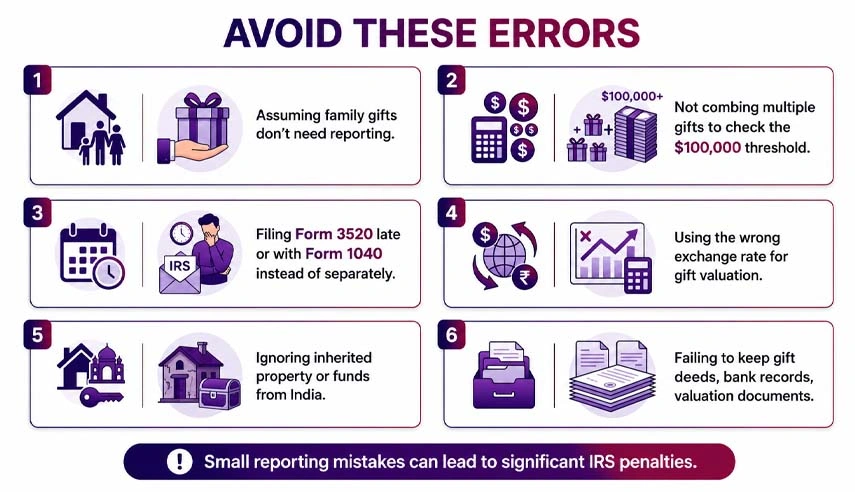

The following are the common mistakes that NRIs must avoid at all costs.

Priya moved to the US on an H-1B visa in 2019 and obtained her green card in 2022. In 2024, her father in Pune sold an ancestral property and transferred $180,000 to her US bank account to help with the home down payment. Now that same year, her mother separately gave her $15,000 from her own savings.

Priya just assumed that because the money came from her parents and the gifts from the family are tax-free in India, there is nothing to report in the US as well. Well, later on, her CPA flagged that the combined gifts from both her mother and father, who are also related parties, total $195,000, which is well above the threshold that would trigger Priya to file Form 3520.

Priya then filed Form 3520 for the 2024 tax year, reporting both the transfer with her father and the mother's details, the transfer date, the USD value using the exchange rate on the transfer date, and supporting bank wire documentation. No tax was owed on the gift; Form 3520 was purely a disclosure filing that was mailed separately to the IRS by the October 15 extended deadline alongside her Form 1040.

If Priya had not filed the form and the IRS later discovered that the underreported transfers were there through the routine bank reporting, she could have faced steep penalties of up to 25% of the gross value for a gift that is completely tax-free.

Connect with Savetaxs and easily claim your treaty benefits with the top tax experts and maximize your tax refunds.

Form 3520 often catches most NRIs off guard more than any other U.S. compliance requirement, specifically because the underlying transaction may seem harmless. A gift from your parents in India is not taxable, and most people reasonably assume that this also means they do not have to report anything. The IRS views it differently: large cross-border transfers require disclosure even when no tax is due.

The overall rule is simple: if you are a US tax resident and you receive more than $100,000 in gifts and inheritance from individuals in India during a single year, count the related donations together and file Form 3520, mail it separately to the IRS, and meet the same deadline as your Form 1040.

In case you have already received a large gift from family in India and are not sure whether you have crossed the set threshold or that you have missed out on the prior year's filing, talk to a US CPA who has cross-border experience before the next filing deadline. The cost of proper guidance is always lower than the penalty for a missed disclosure on money that was never even taxable to begin with.

Savetaxs helps US-based NRIs with complete CPA assistance. Right from data collection to form preparation, threshold verification, to record maintenance and more, our experts provide end-to-end assistance. Connect with us as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1783487960318.png&w=828&q=75)

_1783488079086.webp&w=828&q=75)

_1783341462243.webp&w=828&q=75)