US Tax Forms

IRS Form 8865: Foreign Partnership ReportingIRS Form 8865: Foreign Partnership Reporting

Written by Hatim Dudhiyawala

As a US-based NRI, if you hold any Indian mutual fund, ULIPs, ELSS, or any other Indian investment that qualifies as a PFIC, you are almost certainly required to file Form 8621 with your US tax return every year. The Form 8621 is the IRS information return for the shareholders of a Passive Foreign Investment Company.

In this blog, we will walk you through each part of the Form 8621 for NRIs, which tax method applies to your holdings, and the filing mistakes that keep your tax return open to an IRS audit indefinitely.

IRS Form 8621 is officially titled "Information Return By a Shareholder Of A Passive Foreign Investment Company or Qualified Electing Fund". This is a tax form that US taxpayers must file for each Passive Foreign Investment Company (PFIC) they own.

This form is filed as an attachment to your annual Form 1040 (or 1040-NR for non-resident aliens). There is no separate submission; it goes with your tax return.

Form 8621 serves two major purposes: firstly, it informs the Internal Revenue Service that you must hold a PFIC, and secondly, it reports how the PFIC income will be taxed, which depends on which tax method you have elected or defaulted into.

The IRS form must be filed for each PFIC you hold, so if you own five different Indian mutual fund schemes, you need to file five separate Form 8621s.

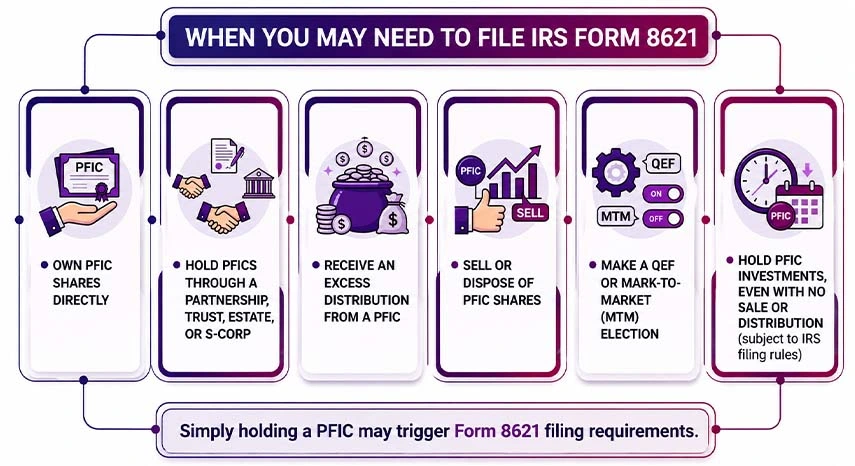

IRS Form 8621 filing must be done by you if you are a US person, meaning a U.S. citizen, green card holder, or someone who has met the substantial presence test.

This last point surprises a lot of people, meaning you may be required to file Form 8621 even if you made no sale, received no distribution, and did nothing with the investment during the year. Merely holding a PFIC can directly trigger a filing requirement in certain situations.

A Quick Note: There is a specific filing exception for NRIs who hold PFICs with a combined value below $25,000 (or $50,000 for married filers filing jointly) at the end of the tax year, provided no election has been made, and no excess distributions are received. Although these exceptions have certain limits and conditions, you can confirm with a US CPA whether it applies to your specific situation before relying on it.

Savetaxs provides extensive CPA support to help you file your taxes.

Every Indian mutual fund scheme, whether debt, hybrid, equity, or index, is almost certainly classified as a PFIC under US tax law.

Indian mutual funds are structured as trusts under SEBI regulations, but the IRS treats them as foreign corporations for tax purposes. Since their primary activity is investing in securities and generating passive income dividends, interest, and capital gains, they satisfy both the PFIC income test (75% + passive income) and the asset test (50% + passive assets) easily.

This straightaway means

Each one of these is a separate PFIC requiring its own Form 8621.

The Form 8621 must mandatorily be filed for every investment that qualifies as a PFIC, including your Indian mutual funds, Indian ETFs, and ULIPs. Each qualifying fund requires a separate Form 8621 filing, regardless of whether any transactions occurred during the year. Just holding a PFIC is more than enough to trigger the reporting obligations in most cases.

And this is what catches many NRIs off guard: they assume that because they did not receive any distributions from their Indian mutual fund during the year, there is no need to report. And this assumption is incorrect. The IRS will require you to make an annual disclosure of your PFIC holdings, and each of the Indian mutual fund schemes you hold is treated as a separate PFIC, requiring its own form.

A PFIC is any foreign corporation that meets either of these tests.

The Income Test: 75% or more of gross income is passive income, including interest, dividends, rents, royalties, and capital gains.

Asset Test: 50% or more of the assets are held to produce passive income.

A foreign fund will only need to satisfy one test to qualify as a PFIC; investment funds, by their nature, must satisfy both tests.

The Common PFIC Investments Relevant To NRIs

| The investment type | PFIC Status |

|---|---|

| Indian equity mutual funds | Yes-PFIC |

| Indian debt mutual funds | Yes-PFIC |

| Indian ETFs (listed on BSE/NSE) | Yes-PFIC |

| ULIPs - investment portion | Yes-likely PFIC |

| Indian Fund of Funds | Yes-PFIC |

| PPF (Public Provident Fund) | Generally not a PFIC, but has a separate FBAR/FATCA reporting |

| NPS (National Pension System) | Uncertain; get specific advice. |

| US-listed Indian ETFs (NYSE/NASDAQ) | No, the US corporation, not a PFIC |

| Individual Indian stocks | No, Individual stocks are not PFICs |

Here is a practical implication: If you want Indian equity exposure without the PFIC complexity, investing through a US-listed India ETF (such as those available on US exchanges) is more tax-efficient for US residents than holding an Indian mutual fund directly.

Understanding the taxation method of a PFIC is essential for any investor in foreign mutual funds that qualify as PFICs.

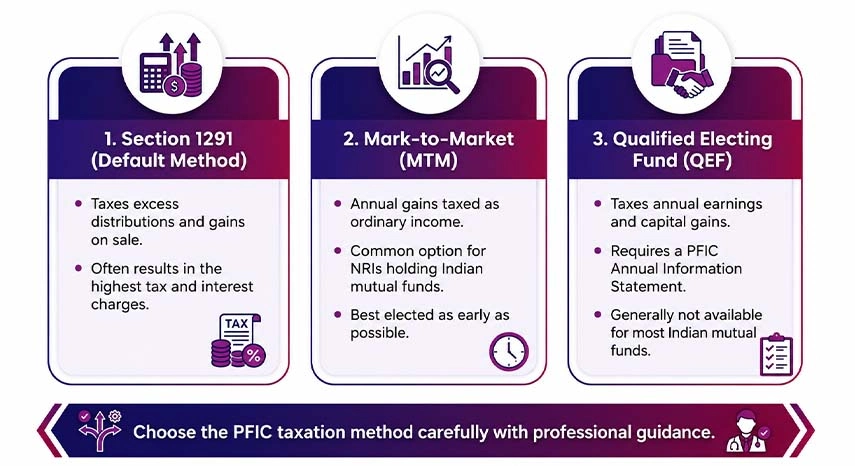

So, there are three ways a PFIC can be taxed: Excess Distribution, Mark-to-Market (MTM), and Qualified Electing Fund (QEF). Let us understand it:

The default taxation method is excess distribution as a $ 1,291 Fund. If you choose this route, you will be taxed on the excess distributions and will then realize a gain on the sale or disposition of stock holdings.

If you elect MTM, your PFIC's annual increases in value are taxed as ordinary gains. At the end of the tax year, the marketable securities you hold are then treated as if you sold or repurchased them at their fair market value on that last business day. The value on the last business day of the year will determine the fund's ordinary gains and losses. Something to note is that if you want to go down this route, although the MTM election can generally be made in a later eligible year, making it as early as possible usually produces better tax outcomes.

For NRIs holding Indian mutual funds who cannot access the QEF, MTM is the most practical and manageable approach, though it still results in less favorable tax treatment than standard US investment fund taxation.

Also ensure that the MTM election is typically irrevocable, meaning once you have made it, you cannot easily switch the methods. Hence, make this decision under professional guidance.

With a QEF election, your PFIC will be taxed based on your PFIC's pro-rata share of undistributed earnings for both the ordinary income as well as the long-term capital gains. However, this method is quite a tax to employ because of the complex documentation requirements associated with the making of the election.

Now, with NRIs holding Indian funds, the QEF election requires the fund to provide a "PFIC Annual Information Statement" with specific financial data. Almost no Indian mutual fund houses provide this. Without it, you cannot make a valid QEF election.

QEF is effectively unviable for NRIs holding standard Indian mutual fund schemes.

The following table demonstrates all three methods with their tax rates, annual filing, India fund provides required data, best for, and more.

| Method | The tax rate | Annual Filing | Indian Fund Provides Required Data | Best For | Avoid If |

|---|---|---|---|---|---|

| Section 1291 (Default) | Highest historical ordinary rate + interest. | Only on the sale/excess distribution. | No such requirements | Nobody; this is the default only if no election is made. | You have a choice; always try to make an election. |

| QEF Election | Capital Gains Rates | Annual Income inclusion | Yes, rarely available. | Funds that provide the PFIC statements. | Indian fund does not provide any required PFIC statement. |

| MTM Election | Ordinary income | Annual unrealized gains | No requirements | Most NRIs with the Indian mutual funds. | You prefer to avoid the annual tax on unrealized gains. |

Form 8621 is a multipart form, and as a taxpayer, understanding its specifics will help you complete and file it correctly. The form is divided into six parts, each serving a different purpose. Which part of the form you complete depends on your specific situation and the tax election you and your CA/CPA choose.

The following table demonstrates the structure of Form 8621

| Section Of The Form | What It Covers | When You Complete It |

|---|---|---|

| Header | Your personal information, PFIC name, address, EIN, or reference ID number, tax year, and share ownership details. | Every Filing |

| Part 1 | Summary of the annual information (share class, fair market value at the end of the tax year, number of shares held) | Every filing when required under Section 1298(f) |

| Part 2 | Elections (QEF, Mark-to-market, Deemed Sale, Deemed Dividends, and other elections) | Only when making or maintaining an election. |

| Part 3 | Income from a QEF (Qualified Electing Fund) [ordinary earnings and net capital gains]. | Only if the QEF election is in effect. |

| Part 4 | Gains or losses from a Mark-to-Market election (year-end fair market value vs the adjusted basis). | Only if the MTM election is in effect. |

| Part 5 | Distributions from and dispositions of stock of a Section 1291 fund (the default "Excess distribution" method). | When you receive distributions or sell shares without a QEF or MTM election. |

| Part 6 | Status of prior year Section 1294 elections and termination of elections. | Only if you previously elected to defer tax on QEF income. |

As the form was revised in December 2025, a new requirement in Part V was added: filers must now enter a three-letter currency code above Line 15a to identify the currency in which distributions were received. This applies to expats who have received investment income in foreign currencies.

So, as an individual without extensive, detailed knowledge of taxation, filing Form 8621 is risky. It is so because the challenge is not simply filing the taxes; instead, it is knowing which parts of the form apply to your specific situation, which election produces the lower tax bill over time, and how to align the form with the rest of your expected tax return.

Now, a wrong election or failing to make one at all will trap you in punitive default tax methods for years. And because each PFIC requires its own form, errors multiply across your portfolio.

Filing Form 8621 is straightforward; the complexity lies in the calculations, not in the filing mechanics.

List every Indian mutual fund scheme, foreign ETF, or other foreign investment fund you hold as of the tax year-end. List each of the PFICs you hold as of the tax year-end. Each one requires a separate Form 8621.

Have you made any prior elections? If not, you are in Section 1291 by default. If you want to make an MTM or QEF election, it must generally be made on a timely filed return for the first year the fund qualifies as a PFIC while you are a US person.

For MTM, you need the fair market value of your fund holdings at the start and end of the tax year. You must use the year-end Net Asset Value per unit, multiply it by your unit count, and convert to USD using the Treasury exchange rate for December 31.

You must fill in the PFIC identification information in Part 1, mark your election in Part 2, and complete the relevant Part (3,4,5) depending on your tax method.

Include all the completed Form 8621 as attachments to your Form 1040; file all of these by the standard deadline, April 15 or October 15, with an extension. If you are abroad, the automatic June 15 extension applies to filing (not to payment).

Meera moved to the United States on an H-1B visa in January 2021 and became a US tax resident. She held three Indian mutual fund schemes at the time: an equity fund, a balanced advantage fund, and a liquid fund, with a combined value of approximately $18,000 at year-end 2021.

Her US CPA determined all three as PFICs and advised her to make the MTM election for each on her 2021 return. The first year she was a US tax resident. For 2021, the three funds had appreciated by approximately $1,200, which Meera recognized as ordinary income on her 2021 return under the MTM treatment.

She then filed three separate Form 8621s, each with a Part 2 MTM election marked and a completed Part 4 with unrealized gain calculations. These were attached to her Form 1040 and filed by October 15 with an extension.

In the year 2023, Meera sold all three funds when she returned to India for the time being. Because she had been using MTM, the gain on the sale was quite straightforward, already taxed annually, with the basis stepped up each year for previously recognized MTM income. No complex Section 1291 lookback calculations were needed.

Had Meera not made the MTM election in 2021, the default Section 1291 treatment would have applied to the 2023 sale, requiring her to allocate the entire gains back to 2021 and 2022 and pay tax at the highest historical ordinary income rate, plus interest charges, for each prior year.

The cost of not making the election in a timely manner results in significantly higher tax and considerable complexity on the 2023 return.

The following are some common mistakes to avoid when filing Form 8621 for Indian mutual funds.

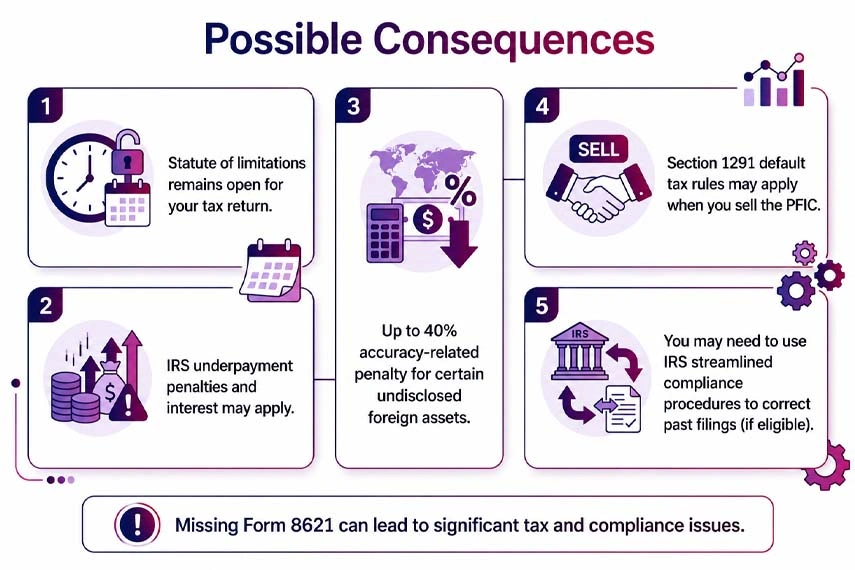

The consequences of missing Form 8621 are serious and compound over time.

If you have unfiled the Form 8621s from prior years, the IRS streamlined filing compliance procedures might be available to bring you into compliance with reduced penalties, given that the non-compliance was unintentional. It is highly advisable to consult a US CPA before attempting to ensure compliance procedures, as eligibility requires careful assessment.

Savetaxs experts help US-based NRIs with end-to-end professional assistance on Form 8621 filing and more.

As an NRI holding Indian mutual funds, for you, one of the most overlooked and most consequential IRS filing requirements has to be Form 8621. The perfect amalgamation of punitive default tax treatment under Section 1219, an open status of limitations for missing filing, and the compounding effect of interest charges makes ignoring this form quite costly.

The overall practical guidance is clear: if you are a US tax resident holding Indian mutual funds, identify each and every scheme you hold, make the MTM election for each in your first eligible year, file a separate Form 8621 for each fund annually, and work with a US CPA with specific experience in PFIC compliance.

If you are an NRI who has never filed Form 8621 and is reading this, it's not too late to fix it. The sooner you act, the better your options. The streamlined compliance path does exist specifically for situations like this and for catching up.

For multiple PFICs, an MTM election or prior-year corrections through the Streamlined Procedures, a CPA with cross-border experience will produce more accurate results than DIY software. In case you are paper-filing, please attach Form 8621 to the back of your 1040 package and send it to the same IRS address as your return.

As an NRI, if you are seeking any professional assistance with Form 8621 filing, Savetaxs is the name to trust. Our experts help you throughout the process from PFIC identification to data processing, calculations, election advice, reconciliations, and more. We help you with all of this and everything else you ask for.

Connect with us as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1783487960318.png&w=828&q=75)

_1783488079086.webp&w=828&q=75)

Yes, for the tax year in which you have held an interest in a PFIC and do not meet all three conditions of the de minimis exceptions.

If your fund grows past $25,000 in a year, or if you have received any distributions or made any disposition, the exceptions are no longer applicable for that year, and you need to file.