What is the Double Tax Avoidance Agreement (DTAA) Between India and Singapore?

Read More

_1752921287.webp&w=3840&q=75)

NRI selling property in India is a complex process, but with the proper understanding and professional guidance, it's a win-win. There is no doubt that the growing Indian real estate market is a lucrative investment opportunity for NRIs, offering strong rental yields and capital appreciation.

NRIs choose to sell their property in India for various reasons, such as diversifying their investment portfolio, meeting financial needs abroad, repatriating funds, and more.

In this guide, we will discuss the key steps, strategies, and actions NRIs must take to liquidate their real estate assets effectively.

Non-resident Indians (NRIs) are permitted to own and sell the following types of properties in India.

Please note that as an NRI, you are not permitted to invest in plantation properties, agricultural lands, farmhouses, and more. However, if you happen to inherit any such property, then it can be sold only to an Indian resident and not to NRIs/PIOs.

The following are the documents that NRIs require to sell property in India:

Passport: Any non-resident Indian who wishes to sell a property in India must hold a valid passport. This will serve as their proof of identity.

Similarly, for PIOs and Overseas citizens of India, a passport will serve the same purpose.

PAN Card: Having a PAN card is important for NRIs with property in India. As for the process, you might be required to apply for a tax exemption certificate after the sale of property.

If you don't have a PAN Card, please apply for it well in advance of the property sale process.

Power of Attorney: For NRIs who can't be physically present in India to sell their properties, they can grant a Power of Attorney (PoA) to a close relative, family member, or friend to complete the transactions on their behalf.

Any individual with the power of attorney has the authority to sign official documents and other agreements on your behalf. The PoA can be specific or general about he rights the person representing you can exercise.

Tax Returns: When an NRI holds a property for a certain period and earns income from renting it, the transaction becomes taxable. The tax returns for the entire property ownership must be prepared.

Address Proof: During the sale of a property, the NRI must provide documents supporting both the Indian and overseas addresses. The documents include a ration card, electricity bills, telephone bills, life insurance policies, political settlements, and more.

Sale Deed: A sale deed is a legal agreement that serves as the primary proof of property ownership.

Documents From The Society: These documents are needed when the property to be sold is in a particular society. These documents inform the buyer that the seller has no outstanding liens to the city.

Encumbrance Certificate: This certifcate ensures that the buyer of the property or land they are about to purchase has no dues to any legal authority. An encumbrance certificate is important when selling an apartment, house, or even land.

Additionally, apart from these documents, if an NRI can provide property tax receipts from over the years, that would be helpful.

Whenever a nonresident Indian NRI sells a property in India, the property generated is taxed as capital gains. The nature of the gains depends solely on how long the priority has been held.

The holding period of property is either long-term or short-term:

NRI capital gain for property sale applicable tax rates are.

Whenever a property is purchased or sold in India, the TDS is deducted. It is the buyer's responsibility to deduct the TDS amount when paying the seller for the property. The deducted amount by the buyer must then be deposited with the Income Tax Department.

For NRIs selling property in India, the same rule applies. Let us understand the applicable TDS rates for NRI property sales under LTCG and STCG.

Unlike Indian resident sellers, where the TDS deduction rate is 1% under section 194-IA, the TDS on the sale of property by NRIs is higher. This is because the TDS is deducted from the capital gains tax liability.

The TDS is deducted when the buyer is making the payment to the seller.

In case of NRIs claiming a refund of excess Tax Deducted at Source (TDS), you have to file an Income tax refund. This is the only way to recover the extra tax deducted, even if your total income is below the taxable limit.

Here's how to claim the NRITDS Refund.

Step 1: Gather the necessary documents.

Please keep the following documents in order, as they will help you claim the TDS refund.

Step 2: Apply for a lower TDS Rate (Optional)

To avoid excessive TDS being deducted in the first place, you must apply for a lower or NIL TDS certificate. To apply for NE, you must submit Form 13 to the Income Tax Assessing Officer (AO).

The AO will review your application and, if satisfied, issue a certificate that will allow the deductors to withhold tax at either a lower or zero rate for future transactions.

Step 3. File Your Income Tax Return (ITR)

To file the income tax return, register on the portal by logging in to the income tax e-filing portal at incometax.gov.in.

Choose the appropriate form for NRIs: use Form ITR-2 if you do not have business income in India, or Form ITR-3 if you do.

Accurately report all income earned in India and the total tax deducted at source as per your Form 26AS.

Lastly, file the return and e-verify it.

Step 4. Receive the refund

After processing your income tax return, the ITD will credit your excess tax to your designated NRO bank account. Now this process can take a few weeks.

To repatriate the funds from the sale proceeds abroad, follow the steps below.

Step 1: Deposit the proceeds

Deposit the sale proceeds of the property in your NRO bank account.

Step 2: Gather all the necessary documents

Keep the following documents in order:

Step 3: Submit the documents to the Bank

Ultimately, the gathered and recorded documents are submitted to your authorized bank. The bank will review the documents and then process the funds transfer to your foreign bank account.

Step 4: The Limits and Rules

As an NRI, you can repatriate up to one million USD in a financial year from your NRO account.

In case of repatriation of additional funds, you can seek approval from the Reserve Bank of India.

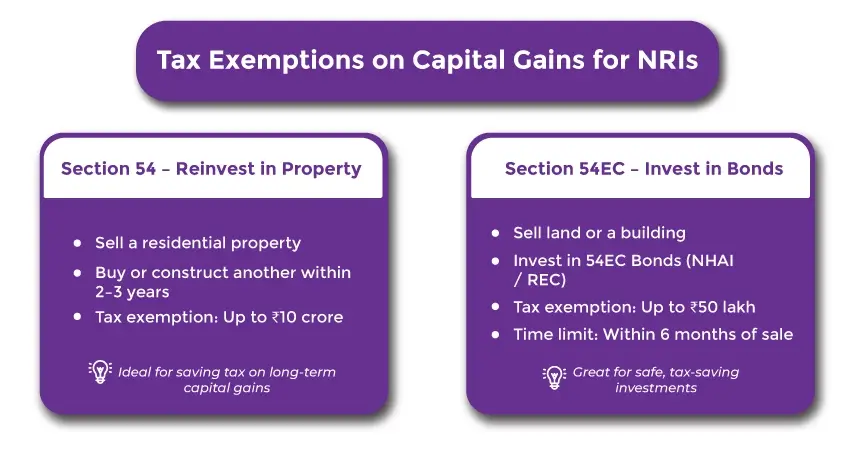

NRIs can claim tax exemptions under Sections 54 and 54EC on long-term capital gains from the sale of residential property in India.

Section 54 of the Income Tax Act provides an exemption from the long-term NRI capital gains tax if an individual plans to reinvest their capital gains in another residential property.

In terms of reinvesting, you can either purchase another residential property within two years or construct one within the time frame of three years from the date of sale. Tax exemption up to 10 crore can be claimed.

Doing so helps the taxpayer save taxes by reinvesting the proceeds in a new home, provided all the conditions under the Act are met.

Whenever a long-term immovable asset, such as land, building, or both, is sold, the profits earned are taxable. However, the taxpayer can avoid or reduce the tax liability by claiming a tax exemption under section 54EC of the Income Tax Act.

Under this section, you invest the capital gains in the specified bonds notified by the central government within 6 months from the date of sale. Such bonds are also known as capital aid bonds or 54EC bonds, and investing in them allows the taxpayer to avoid paying taxes.

Non-resident indian use a power of attorney to appoint an attorney or agent to help them sell their properties in India. NRIs do so because they find it challenging to be physically present in India.

A POA authorizes the holder to make decisions on behalf of the owner of the property. You can choose a close relative or a trusted legal professional to hold power of attorney for the NRI property sale.

As an NRI, if you are selling a property in India, here are a few legal and practical tips to consider.

As aforementioned, selling a property in India as an NRI can be a tedious task, especially if you lack an understanding of the Indian real estate market and Indian taxation. Hence, it is advisable to seek the help of a professional with expertise in both Indian and foreign taxation and the Indian real estate market for NRIs.

Savetaxs is one such expert and the emerging name in the taxation industry for NRIs. When it comes to selling a property in India as an NRI, Savetax will help you with all documentation, including assisting with Form 15CA/15CB, obtaining lower TDS certificates, consultations on repatriation of funds, drafting a power of attorney, and more.

Our experts bring over 30 years of experience to the table, hence you can rest assured that they will help you navigate the complexities of NRI property transactions and more.

So, if you are an NRI planning to sell a property in India, connect with Savetaxs today and enjoy the benefits we bring for you. Savetaxs is serving its clients 24/7 across all time zones. Get in touch with us, and our experts will help you with a personalized sales strategy for your property.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Shaw brings 8 years of experience in auditing and taxation. He has a deep understanding of disciplinary regulations and delivers comprehensive auditing services to businesses and individuals. From financial auditing to tax planning, risk assessment, and financial reporting. Mr Shaw's expertise is impeccable.

Want to read more? Explore Blogs