NRI Income Tax & Compliance

What Is Section 54B Of The Income Tax Act?What Is Section 54B Of The Income Tax Act?

Written by Hatim Dudhiyawala

The National Pension Scheme (NPS) is a government-sponsored scheme launched in January 2004 for government employees. This is a long-term retirement plan for individuals under the purview of the Pension Fund Regulatory and Development Authority (PFRDA) and the Central Government. It is a flexible scheme that allows you to contribute to the government's pension account until your retirement. In addition, it provides you with complete control over your financial future.

The scheme is now available to all citizens of India, but the question is: can non-resident Indians (NRIs) also invest in it? Yes, NRIs are eligible to invest in the NPS scheme. Want to know more about the National Pension Scheme, its eligibility criteria, and benefits? Check out the blog below for detailed answers.

As mentioned, the National Pension Scheme was launched by the Indian government in 2004 to provide financial security for its employees after retirement. However, since 2009, the scheme has been available to all Indian citizens, including private-sector employees, self-employed individuals, and NRIs. In India, the NPS scheme is regulated by the Pension Fund Regulatory and Development Authority (PFRDA).

It is a regular investment scheme in which you contribute a fixed amount each year until maturity. Additionally, upon maturity, you receive a fixed pension for life, providing a regular income after retirement. Based on the last 10 years' performance (assuming no market disruptions), you can expect the following annual returns:

Investing in NPS also helps you claim up to INR 1,50,000 tax deduction under Section 80C while filing income tax returns if you choose the old tax regime. Moreover, the scheme offers partial withdrawals, subject to a 3-year minimum lock-in period.

The Indian government introduced the NPS Vatsalya Scheme under the Finance Act 2024. Under this scheme, parents can open an NPS account on behalf of their minor children and contribute monthly or annually until the child turns 18. The minimum annual contribution allowed is INR 1,000. After the child turns 18, the NPS Vatsalya account automatically converts into a standard NPS account. NRIs are also eligible to invest in this scheme.

To invest in NPS, both Indian residents and NRIs must fulfill the following eligibility criteria:

These are some of the eligibility criteria a person must meet to open an NPS account. Moving ahead, let's know how to log in to this account.

You can log into your NPS account using the following methods:

For many individuals, whether they are Indian residents or NRIs, keeping their financial future safe after retirement, NPS is an attractive option. To provide high returns on investment, the NPS scheme consists of flexible allocation features of assets and investment objectives. Some of the key features of NPS for Indians and NRIs are as follows:

1. Age Limit: 18–60 years. Parents can open accounts for minor children and manage them until the child turns 18.

2. Returns: Historically, 11–12% annual returns on investment. Returns are not fixed, but they are competitive with other tax-saving schemes.

3. Equity Allocation: Two options - Auto Choice (age-based risk allocation) and Active Choice (choose schemes and split investment). Equity exposure is capped between 50–70% depending on age and category.

4. Flexibility: Subscribers can add funds anytime, change investment options, switch fund managers, and manage accounts from anywhere, even when relocating or changing jobs.

1. Travel Agnostic: NRIs can maintain NPS benefits globally as long as they remain Indian citizens.

2. Portfolio Management: Active mode allows NRIs to choose asset allocation; the fund manager manages auto mode. Four options available:

3. Liquidity: Partial withdrawals up to 25% are allowed after 3 years of uninterrupted contributions. Withdrawals can be made up to three times for specific reasons (e.g., housing, marriage, education, critical illness).

These are some of the key features of the National Pension Scheme for Indian residents and NRIs. Moving on, let's look at the NPS withdrawal rules for Indians and NRIs.

To balance your fund needs while securing a certain amount for your retirement, the NPS withdrawal rules are in place. Whether you want to withdraw the full amount at retirement and need a partial amount for emergencies, understanding the rules and options can help you make the right decisions. Furthermore, let's look at the NPS withdrawal rules for Indians.

Here are the withdrawal rules for NPS for Indian residents:

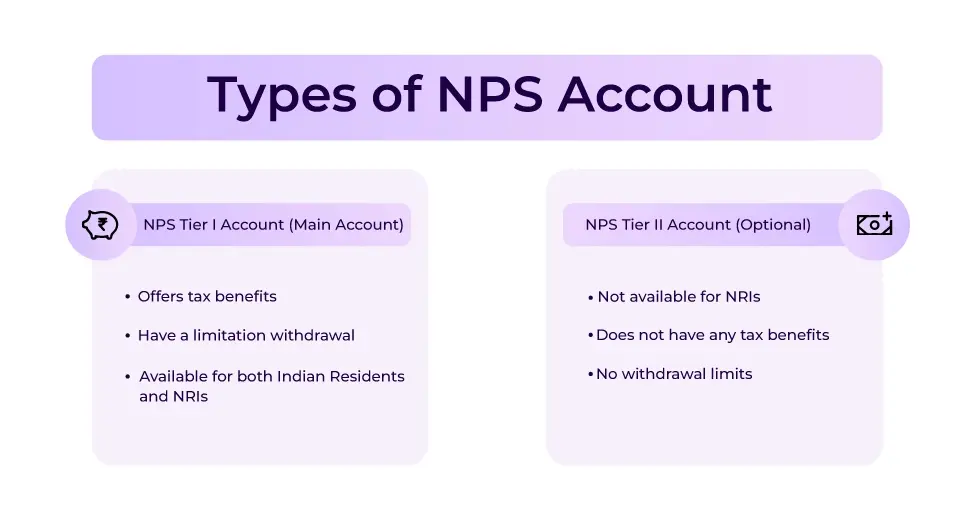

Note: A Tier II NPS account allows complete withdrawal at any time without lock-in.

*Note: In case the NRI dies, the legal heir or nominee is eligible to receive the whole investment amount.

The National Pension Scheme accounts are of two types, i.e., Tier I NPS Account and Tier II NPS Account. Let's know about them in detail.

Under section 80CCD(5), tax exemption is provided on the purchase of annuity or superannuation at 60 years. However, under section 80CCD(3), any subsequent income from an annuity is taxed.

These are the tax benefits Indian residents receive on a Tier I NPS account under section 80CCD. Moving further, let's know the tax benefits that Tier I National Pension Scheme Account NRIs receive under section 80CCD.

Do you know that, apart from providing a secure financial future, NPS also helps NRIs claim several tax benefits? Want to know what they are? Read the points below and get your answers.

Hence, through the NPS scheme, with tax benefits, NRIs build their retirement amount. Furthermore, after the scheme matures, 40% of the uncommuted amount provides lifelong pensions to NRIs, i.e., a regular source of income after retirement.

These are the tax benefits NRIs receive under section 80CCD after opening a Tier I National Pension Scheme Account. Moving ahead, let's know the tax benefit of a Tier II National Pension Scheme Account under Section 80C.

As mentioned above, a Tier II National Pension Scheme Account is only available to Indian residents. Considering this, the benefits will also be available to them. Moving on, let's look at a few perks of opening this account.

These are the benefits that you can get while opening a Tier II National Pension Scheme account under section 80C. However, these tax deduction benefits are not available under the new tax regime. To gain all these perks of NPS, you need to open an NPS account. Want to know how you can do so? Read the following section and get your answers.

Indian residents and NRIs can invest in the National Pension Scheme by opening an account on the NPS website or through any Indian bank that offers the NPS facility. The process of opening an NPS account is the same for NRIs and Indian residents, but it differs slightly. Let's first go over the steps to open an NPS account online for Indian residents.

The National Pension Scheme (NPS) allows both NRIs and Indian residents to secure their retirement with flexible investment options, attractive returns, and tax benefits. If you are looking for a long-term retirement plan that aligns with your financial goals, consider investing in NPS.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1782996918646.png&w=828&q=75)

_1782911003992.webp&w=828&q=75)