Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

Yes, NRIs can invest in mutual funds from abroad. For many, this is one of the most efficient ways to maintain a financial footprint in India and build their long-term wealth. However, the rules, tax treatment, account requirements, and other practical considerations are certainly different from what a resident investor would experience.

In this blog, we will explore the complexities NRIs face when investing in Indian mutual funds and provide you with a practical, expert review that covers everything from the legal framework to accounting and tax obligations.

Generally, NRI mutual fund investments in India are regulated by two primary bodies: the Foreign Exchange Management Act (FEMA) and the regulations issued by the Securities and Exchange Board of India (SEBI). Together, these regulatory frameworks define who can invest, what types of funds they can invest in, through which accounts they invest, and on what terms.

The SEBI mutual fund regulation generally permits NRIs to invest in all categories of mutual funds available to residents of India, including equity, debt, hybrid, index, ETF, and sectoral funds, subject to KYC compliance, with investments routed through NRO and NRE accounts.

Generally, there are no specific SEBI restrictions on how much an NRI can invest in mutual funds, nor on the number of folios or the AMCs. However, individual AMC-level policies, specifically those derived from US/Canada FATCA compliance costs, might impose their own restrictions.

| The parameter | Rules and Regulations | Details |

|---|---|---|

| Governing Law | FEMA 1999 + SEBI MF Regulations | Both frameworks must be complied with simultaneously. |

| Permitted Account types | NRE or NRO bank account | Regular savings or a current bank account cannot be used. |

| Repatriation - NRE Route | Fully Repatriable | Both the gains and the funds can be easily repatriated. |

| Repatriation - NRO route | Up to USD 1 million FY | Subject to applicable taxes being paid and CA certification through Form 15CB. |

| Fund categories allowed | All SEBI-regulated categories. | Equity, debt, hybrids, indices, ETFs, ELSS, and more. |

| US? Canada NRI Restriction | AMC-level policy (FATCA) | Many AMCs refuse; however, the SBI MF, UTI MF, and PPFAS are exceptions. |

| KYC Compliance | Mandatory | NRI-specific KYC through KRA; POA may be required. |

Savetaxs helps NRIs file their ITR in India under expert guidance and with 100% accuracy.

As an NRI, before placing your first mutual fund investment, you have to have the following elements in place. If not, and you missed out on any of them, your investment application will be rejected by the AMC or the RTA (the registrar and transfer agent).

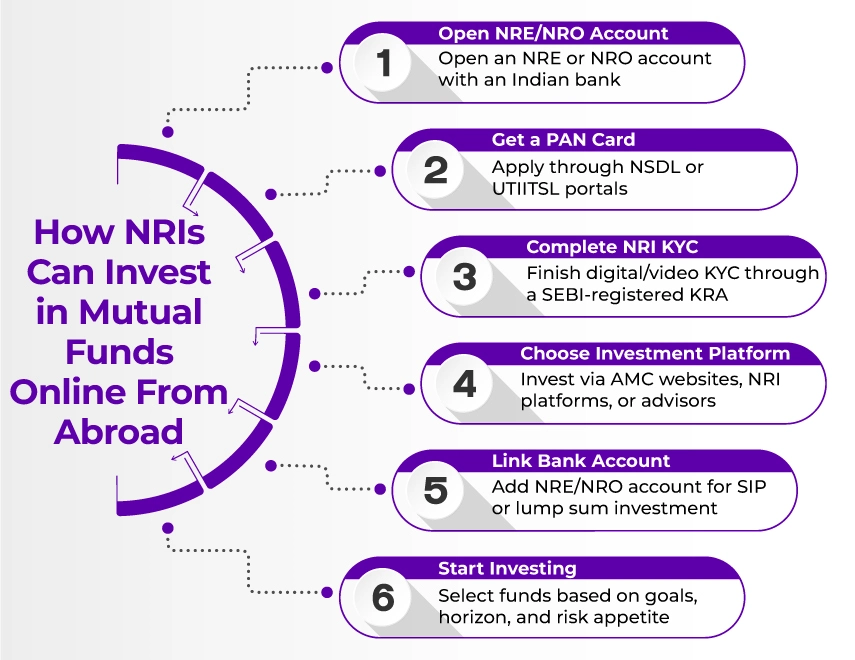

As digital-first platforms and direct plan portals have emerged, the entire process of investing in India for NRIs has become significantly streamlined. NRIs can now complete the entire process, from SIP setup to KYC, without coming to India.

NRIs must begin by opening NRE and NRO accounts with any legitimate Indian bank, such as HDFC, ICICI, SBI, Axis Bank, Kotak Bank, and others. These banks offer great banking services with international digital onboarding capabilities.

If you do not already have a PAN, apply for a PAN Card via the NSDL or UTIITSL portals. NRIs can apply using their passport as proof of identity and their overseas address as proof of address. The PAN Card is issued within 15 working days and mailed to your Indian or overseas address.

You can complete your NRI KYC through a SEBI-registered KRA. Nowadays, there are platforms that offer digital NRI KYC using video-based verification.

As an NRI, you can invest either through an AMC website directly, through NRI-focused platforms, or through a SEBI-registered investment advisory or mutual fund distributor in India.

Then add your NRE or NRO bank account as the payment source. Most platforms generally support NACH (National Automated Clearing House) mandates for the SIP automation. However, ensure that the bank account is in the same name as your KYC registration to avoid transaction rejections.

As an NRI, you can select your funds based on your financial goals, investment horizon, and risk appetite. NRIs can invest in the mutual fund account via a lump sum or Systematic Withdrawal Plan (SWP).

Understanding mutual fund taxation for NRIs is crucial. With respect to mutual fund investments, two mechanisms apply: TDS (tax deducted at source) is automatically applied by the AMC at the time of redemption, and the capital gains tax is computed on the actual gains realised. NRIs are also eligible to claim the DTAA to reduce their overall TDS burden wherever applicable.

However, to understand and manage the taxation of mutual funds for NRIs, you need professional assistance.

Unlike resident investors, who pay taxes only when filing their ITR, AMCs are eligible to deduct TDS at the source on all redemptions by NRI investors.

| Fund Type | Holding Period | The Gain Type | TDS Rate |

|---|---|---|---|

| Equity Mutual Funds | For less than 12 months | STCG (Short-term capital gain) | 15% |

| Equity mutual funds | For 12 months or more | LTCG (long-term capital gain) [gains above Rs 1.25 lakh] | 12.50% |

| Debt Mutual Funds | Less than 24 months | STCG (added to the income) | 30% |

| Debt Mutual Funds | 12 months or more | LTCG | 12.50% |

| Hybrid or Balance Funds | Depends on the component of equity | The equity/debt rules are applicable | As applicable above. |

| ELSS (The tax savings funds) | Three-year lock-in | LTCG | 12.50% |

LTCG Exemption Threshold

For an equity mutual fund, the first Rs 1 lakh of long-term capital gains in a financial year is exempt from tax. This exemption applies to NRIs as well. Whereas gains earned above this threshold are taxed at 12.5% without the benefit of indexation.

Dividend Taxation

Dividends declared by mutual funds are added to an NRI's total income in India and taxed at the applicable tax rates. The AMC deducts applicable TDS on dividend income for NRIs before crediting it.

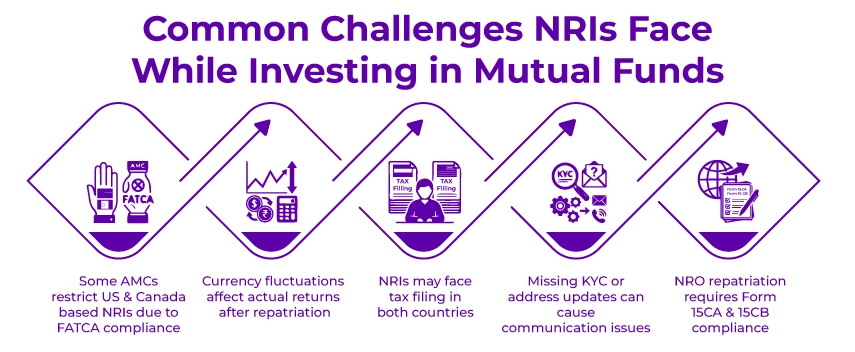

NRIs often face digital and regulatory hurdles that a resident Indian does not while investing in Indian mutual funds. Hence, understanding such challenges well in advance is the best way to address them without disrupting your investment plans.

This is the most frequently encountered obstacle for NRIs in Canada or the USA. Some major Indian AMCs do not accept investments from Canadian- and US-based NRIs due to the high legal and operational costs associated with FATCA and FINRA compliance. Henceforth, always verify your current acceptance status directly with the AMC before investing, as policy changes.

The NRI mutual fund is INR-denominated. When you repatriate your proceeds, the INR/foreign-currency exchange rate at the time of conversion affects your NRI real return. If the rupee is weak, it erodes gains, whereas a strengthening rupee amplifies them. Furthermore, if repatriations are made through the NRO route, they require CA certification, tax payment confirmation, and bank processing. If you need repatriation by a specific date, plan the repatriation well in advance.

As an NRI mutual fund investor, you may face tax obligations in two countries: one in India, where TDS is deducted, and another in your resident country, where the same income could be taxable. This is where the DTAA comes into play to mitigate actual double taxation, managing compliance in both tax jurisdictions, including ITR filing, DTAA claims, Form 15CA/15CB, and foreign country tax declarations, all of which require careful coordination.

Although everything is now digital, some AMCs still send account statements, redemption cheques, and KYC correspondence by post. Now, as an NRI without a reliable Indian address or a PoA holder to receive documents, you may miss out on critical communications. Ensure that your address is updated, and your email is linked to the digital statements.

If you have invested in a mutual fund from an NRO account, to repatriate funds, you require Form 15CA (a self-declaration form submitted to the Income Tax Department) and Form 15CB (a CA certificate of tax compliance). The Indian bank will not process your international Repatriation without these forms. In case you have filed incorrect or incomplete Form 15CA or CB, these forms can result in remittance delays and other regulatory queries.

Start your dream business in India with Savetaxs NRI Business Setup Consultation.

Yes, NRIs can invest in Indian mutual funds from abroad. The mutual fund investment opportunity for NRIs represents a comprehensive wealth-building opportunity, offering access to one of the world's largest and fastest-growing economies, a diverse range of fund categories, and a well-regulated investment environment overseen by SEBI. Over the years, the digital infrastructure around NRI investing has improved significantly, making the entire process far more accessible than it was a decade ago.

However, the path to a successful NRI mutual fund investment passes through three non-negotiable steps: first, open an NRE or NRO account and have KYC in place before making any investment as an NRI. Second, understand the TDS implications and file your Indian ITR every year to claim the applicable refunds. Third is to seek advice from an SEBI-registered advisor or a qualified CA who understands both Indian regulations and the compliance requirements of your home country. When it comes to having a team of qualified CAs and CPAs who understand NRI investments throughout, Savetaxs is the name to trust.

The experts provide strategic and advisory services on suitable mutual fund assets, onboarding, compliance, transaction processing, relationship management, regulatory knowledge, and more.

Connect with us as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)