Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

In 2025, with a real GDP growth rate of 6.5%, India became the 4th largest global economy. It is also projected to be the fastest-growing major economy in the world. This growth is also evident in India's investment ecosystem and financial markets.

Furthermore, as the economy grows, the country offers several passive-income strategies for NRIs, from fixed deposits to dividend-paying stocks. It plays an important role in achieving financial freedom.

Being an NRI, are you also looking for passive income strategies? This blog provides you with complete information on what passive income is and strategies to build your income source in India. So read on and gather all the information.

Passive income can be defined as the money that you earn without active involvement or with minimal effort. Unlike active income generated through a job or employment (salary or wages), which requires constant work, passive income comes from royalties, investments, or other sources. Common examples of it include rental income, business earnings that you own but do not manage actively, dividends from investments, and more. Additionally, in active vs passive income for NRIs, passive income is a good option as it does not require much attention or minimal to no effort.

This was all about passive income. Moving ahead, let's know the benefits of passive income for NRIs.

Here are some of the benefits of creating a source of passive income for NRIs:

These are some of the key benefits of passive income for investors. Moving further, now let's know the top five passive income options for NRIs in India.

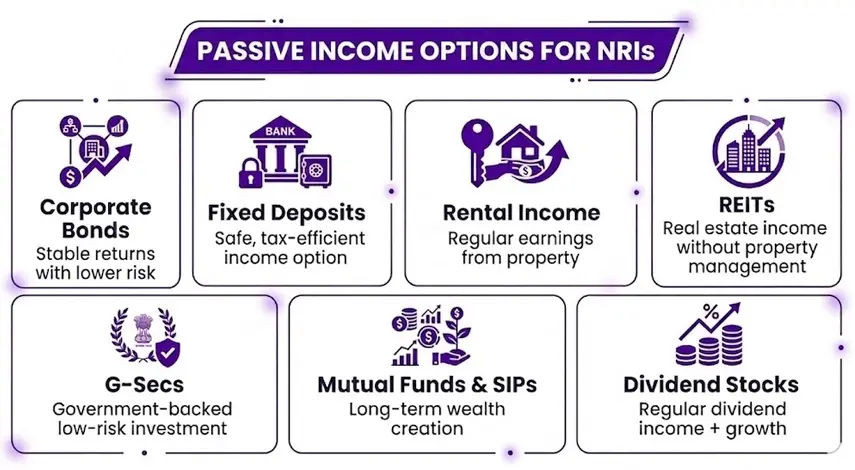

Here is the list of the top 7 passive income options for NRIs in India:

Issued by companies and corporations, Investment-Grade Corporate Bonds are debt securities with a high credit quality, often offering potential returns of up to 12-14%. These bonds are rated from AAA to BBB, issued and frequently evaluated by credit agencies like CARE, CRISIL, and ICRA.

Further, bond investments for NRIs offer stable passive income through fixed income payments at regular intervals. Additionally, these investments fall within the lower-risk segment of the corporate credit market.

Just like millions of Indian residents, NRIs also find that a fixed deposit is the most straightforward source of passive income in India. Additionally, according to RBI, in FY 2025, NRI fixed deposits in India increased nearly 9.9%, reaching US$ 16.16 billion (approx INR 1.39 lakh crore).

In India, FD options for NRIs depend on whether they are investing their Indian earnings or foreign earnings. Another thing that they consider is the repatriation of funds and taxation. Considering this, here is a breakdown of FD passive income options for NRIs available in India and how tax on NRI FD interest is taxed in India:

Real estate has always remained a preferred investment route for NRIs in India, and it is always backed by real growth. Additionally, the Indian real estate market between 2020 and 2025 has experienced a compound annual growth rate (CAGR) of 25.6%. This growth is driven by high demand for urbanization and luxury housing.

Considering this, for NRIs, real estate investments such as commercial office space rentals, residential property, and logistics or warehousing assets can help generate steady passive income. NRIs are allowed to purchase residential and commercial properties in India. However, under FEMA regulations, they are not permitted to purchase any type of plantation property, including farmhouses, agricultural land, and more.

Moreover, rental income is credited to an NRO account and is taxed in India. Apart from this, rental income repatriation is allowed up to certain limits annually, subject to applicable TDS.

Apart from this, instead of directly owning and managing properties, NRIs may consider investment through Real Estate Investment Trusts (REITs). These are listed instruments that allow NRIs to take part in commercial real estate income. It includes malls, office parks, warehouses, and more. These are suitable options for NRIs who want exposure to India's real estate market without the hassle of property management. Here is what they need to consider before investing in REITs:

Introduced in March 2020, the Fully Accessible Route (FAR) framework allows NRIs to invest in government securities without restrictions or investment caps. G-secs or government securities are debt instruments backed by a sovereign guarantee. These include dated government bonds, Treasury Bills (T-bills), municipal bonds, and state development loans (SDLs). Additionally, as these investments are backed by the government, they carry very minimal credit risk.

However, compared to privately issued corporate bonds, the return on investments in these is low. These passive income options for NRIs are good for parking funds or capital preservation for short-term and long-term goals. Furthermore, with maturities ranging from 91 days to 40 years, these investments offer NRIs flexibility across different time horizons.

Mutual funds offer NRIs a diversified, professionally managed route into Indian financial markets without the requirements to manage individual bonds or stocks. Subject to compliance requirements and fund house-specific KYC, they can invest in several mutual fund schemes.

Apart from this, systematic investment plans for NRIs allow you to invest a fixed amount at regular intervals, i.e., quarterly or monthly. This makes it practical to consistently invest from abroad. These are of two types: dividend option equity funds and growth option funds. Dividend option funds generate periodic income while growth funds focus on long-term wealth generation.

Historically, Indian equity markets have delivered competitive long-term returns compared to several global indices, although returns vary across market cycles. Dividend stocks are shares of companies that pay part of their profit to their shareholders. Considering this, if you purchase these stocks every year or even every few months, you can receive dividends.

Additionally, with dividends, the share value also grows, which means that you can earn more money if, later on, you sell them. However, it is advisable to choose a stable and well-known company for this type of investment.

These are popular NRI investment options for passive income in India. Moving forward, let's know how these passive income sources are taxed in India.

It is important for NRIs to understand how different passive incomes are taxed in India. It helps in staying compliant with Indian tax laws and estimating your returns. To provide you with an idea, here is the table below that showcases how different income streams are generally taxed.

|

Income Source |

NRI Passive Income Tax Treatment in India |

Key Notes |

|

Investment Grade Corporate Bonds |

Face 30% TDS on interest (NRO account) and 12.5% -30% in capital gains based on listing status and holding period. |

Interest is tax-free if invested via an NRE account, while PSU bonds provide tax exemption, and DTAA provides tax relief. |

|

NRI Fixed Deposits |

Depends on NRI FD type, i.e.,

|

Should check taxability in your resident country. Additionally, if applicable, the DTAA benefit may reduce the TDS rate. |

|

Real Estate Rental Income |

Taxable, TDS applicable |

Credited to NRO account, limited repatriation allowed, i.e., USD 1 million per financial year. |

|

REITS Investment |

Depending on the distribution type, partially taxable. |

Tax liability is determined by investment structure. |

|

G-Secs |

Based on income slabs and holding periods, interest and capital gains are taxed. |

Allow fund repatriation based on NRI account type (NRE/ NRO); DTAA may also be applicable depending on the country. |

|

Mutual Funds |

Taxed based on fund type and holding period |

Debt vs equity treatment significantly differs |

|

Stock Dividends |

The company deducts TDS before payment |

Taxation rates vary; DTAA may also be applicable |

This is how different passive income options are taxed in India. Moving ahead, let's know the common mistakes to avoid while investing in passive income in India.

Investors often confuse passive investment with quickly getting rich. However, if you do not correctly invest in a passive income source, it can impact your financial security. Additionally, even well-intentioned NRI investors make avoidable mistakes. To help you out, here are some common mistakes that most NRIs make while investing in passive income sources.

These are some of the mistakes that NRIs unknowingly make that further impact their investments in India. To manage better, it is advisable to take the help of a professional.

With smart investment options provided by experts at Savetaxs, begin your secure financial journey in India.

Lastly, passive income strategies for NRIs are a powerful tool for achieving financial freedom. Considering this, if you want to be secure financially today and in the future, it is a great idea to invest in different passive income sources. Now, the investment choice depends on your investment goals, time horizon, and risk appetite.

However, if you are confused and looking for assistance in selecting the right NRI investment, connect with Savetaxs. Our financial experts will provide your personalized guidance and assist you in selecting the right investment that perfectly matches your needs.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)