NRI Income Tax & Compliance

Income Tax Notice to Salaried EmployeesIncome Tax Notice to Salaried Employees

Written by Hatim Dudhiyawala

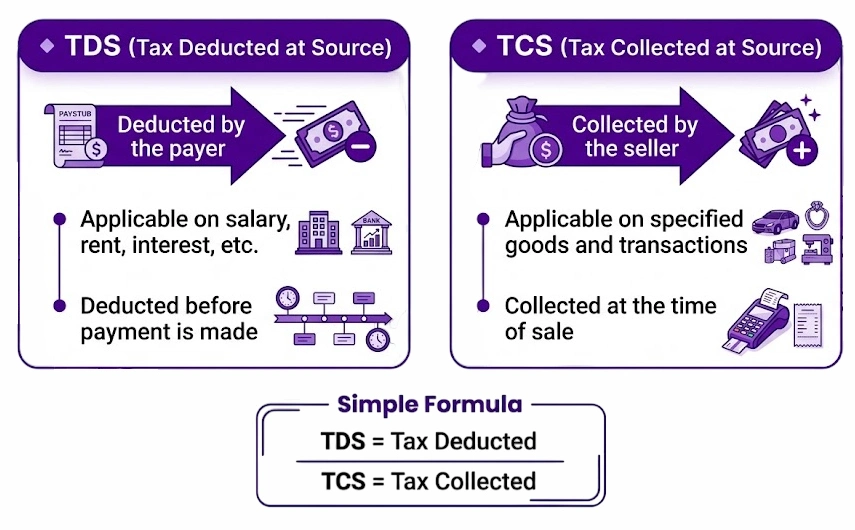

The tax collected at source and the tax deducted at source are both core concepts of Indian taxation. TDS is the tax deducted from payments made to an individual or other entity when the amount exceeds a set limit. While the TCS refers to the tax collected by the seller during a transaction with the buyer.

The provisions of TDS and TCS operate at the source of income and, as their full forms imply, tax collected or tax deducted at the SOURCE. The fundamentals of TDS and TCS are that both are advanced tax collection mechanisms used by the government to ensure a steady revenue stream and keep tax evasion at bay.

In this blog, we will understand the clear difference between TDS and TCS, how they apply, and more.

TDS is the tax that gets deducted at the source of a payment before it reaches you. The person or entity making the payment, such as your bank, employer, or tenant, is responsible for deducting a percentage from the payment as tax and depositing it with the government on your behalf. You receive the balance after deduction.

Under the IT Act, an individual or a company can deduct tax at source on income if the payment for any good or service exceeds a certain amount.

The Government of India determines the TDS rates and thresholds for different types of goods and services for a particular financial year.

The service includes the following.

In a transaction where the TDS is applicable, the person or a firm receiving the payment is called the deductee. The individual or entity deducting TDS from the payment is known as a deductor.

The following table demonstrates the TDS rates for some payment types.

| Type Of Payment | TDS Rate |

|---|---|

| Salaries | As per the tax slab |

| Rental charges greater than Rs 50,000 per month for building, plant, land, and machinery. |

10% for the land, building, and furniture, and 2% for the plant, machinery, and equipment. |

| Prize money for lotteries, horse races, crossword puzzles, and so on is more than Rs 10,000 per transaction. |

30% |

| Brokerage or commission from lottery ticket sales exceeding Rs 20,000. |

2% |

| Immovable property purchase of more than Rs 50,00,000 |

1% |

| Single Payment of Rs 30,000 or aggregate payment of Rs 1,00,000 during a year to a contractor. | 1% for individuals or HUFs, 2% for others. |

Here's an example to help with understanding. Assume XYZ Ltd pays rent of Rs 80,000 per month for a warehouse, which exceeds the Rs 50,000-per-month threshold.

Thus, XYZ Ltd will deduct TDS at 10%, amounting to Rs 8,000, and then pay Rs 72,000 as the monthly rental charge.

Now, the warehouse owner will list Rs 9,60,000 gross income in the income tax return and claim a TDS of Rs 96,000, which can already be deducted as a tax liability credit, also showing a TDS credit.

Tax collected at source works differently from TDS. Here, it's the seller, not the buyer, who collects tax from the buyer at the point of sale and deposits it with the government.

Instead of deducting TCS from the income you receive, it is added to what you pay. Here, the seller collects a small percentage of the amount over and above the transaction amount as a tax, which is then deposited into the government.

The tax collected at source applies to specific categories of transactions, including:

Sale of scrap, minerals, and forest products.

The following are the TCS rates for some commonly bought goods.

|

Goods Purchased |

TCS Rate |

|---|---|

|

Tendu leaves |

2% |

|

Alcohol |

2% |

|

Timber wood from a forest on lease |

2.5% |

|

Scrap |

2% |

|

Motor vehicles worth more than Rs 10 lakh |

1% |

|

Toll plaza, quarry, mine, and the parking lot. |

2% |

|

Metals (including iron ore, lignite, and coal) |

2% |

|

Forest produce (excluding tendu leaves and timber) |

2.5% |

Suppose Mr. Mishra purchases tendu leaves worth Rs 60,000 from Mr. Sharma. However, Mr. Mishra will pay the following amount:

Rs [ 60,000 + (5% of 60,000)] = Rs 63,000

Mr Sharma will collect the extra amount of Rs 3000, known as the TCS credit.

The following table demonstrates the clear difference between TDS and TCS.

|

Parameters |

TDS |

TCS |

|---|---|---|

|

Meaning |

TDS is the tax deducted by a person or entity when making a payment. |

TCS is the tax collected by the seller at the time of sale. |

|

Time Of Incidence |

The purchase of goods or services. |

Sale of goods and services. |

|

Transaction Covered |

Rent, interest.commission, salaries, brokerage, and more. |

Selling of the toll tickets, forest products, tendu leaves, cars, minerals, liquor, timber scrap, etc. |

|

Time Of Deduction |

When the payment is either due or made, whichever comes sooner. |

At the time of sale. |

|

Person Responsible |

An individual or a company making the payment (the customer). |

Person receiving the payment (the supplier). |

|

Filing Quarterly Statements |

Form 24Q (for salaries, pension, and interest income of senior citizens), Form 26Q (for anything except salary), and Form 27Q (for payments made to NRIs). The returns have to be submitted quarterly except under exceptional circumstances. |

Form 27EQ. The returns have to be submitted quarterly. |

|

Relevant Sections |

Section 192, Section 194A, Section 194C, Section 194I, Section 194J, Section 194lA, Section 195. |

Section 206C, Section 206(1G), section 206C(1H). |

In a transaction, if a buyer deducts TDS under the provisions of the Income-tax Act, TCS is not applicable.

Connect with Savetaxs to apply for your NRI PAN card without errors or hurdles.

The provisions of TDS and TCS are applicable to prevent tax evasion, maintain a record of transactions undertaken by taxpayers, etc. Henceforth, it becomes necessary to understand the key difference between TDS and TCS to understand the compliance requirements and adhere to them accordingly.

For NRIs, both TDS and TCS regularly apply: TDS on Indian income sources and TCS on foreign remittances under LRS. Keeping track of what has been deducted or collected, cross-checking it against your Form 26AS, and claiming the correct credit in your ITR are ways to avoid either overpaying tax or facing a demand for the shortfall.

In India, if you are dealing with a large property transaction, NRI income with applicable DTAA benefits, significant LRS remittances, a CA familiar with cross-border taxation can help ensure the right rates are applied and that no refunds go unclaimed.

Such a team of expert CAs is available at Savetaxs and is well-versed in NRI and cross-border taxation. They will help you calculate tax credits, file returns, resolve mismatches, and maximize tax recovery.

Connect with us as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence.

Want to read more? Explore Blogs

_1782219386740.webp&w=828&q=75)