_1784120197435.webp&w=828&q=75)

NRI Banking Services

NRE FD vs FCNR(B): Which Is Better for NRIs?NRE FD vs FCNR(B): Which Is Better for NRIs?

Written by Hatim Dudhiyawala

Over the last few years, India, with its rapid industrial development, has been attracting a lot of Foreign Direct Investments (FDI). For any NRI, this makes investments highly valuable in the country. With many investment options available, NRIs often choose to invest in fixed deposits. It is because they are low-risk, offer guaranteed returns, and have convenient tenure flexibility.

However, rising inflation rates are forcing fixed deposit alternatives for NRIs in India. Considering this, with you as an NRI, are you also confused about choosing the right fixed deposit alternative for your investment? From mutual funds to government securities and NPS, there are several options available.

Want to know about them in detail and how they are good fixed deposit alternatives for NRIs in India? Well, you are on the right destination, read the blog, and clear all your doubts.

Before moving to the fixed deposit alternatives for NRIs, first, let's know whether NRIs should look beyond it. Though FDs are a safe and familiar investment option and are good for short-term parking of funds. However, they have certain constraints that hinder your financial progress. Considering this, the NRO fixed deposit for NRI interest is taxed at 30% TDS, which makes the after-tax return low.

Here is the issue: a 7% NRE fixed deposit interest rate looks good, but the inflation in India typically runs at 5%-6%, and the real return you get after adjusting for inflation is often only around 1%-2%. In this, add 3% - 4% annual rupee depreciation against the dollar, and in comparison to foreign currency, your actual buying power of returns is often negative or flat.

Considering this, compared to your NRE savings account, an FD offers you a higher interest rate, but the effective long-term return is relatively lower than several other investment options available in the market. Today, a 6-7% annual interest rate is generally provided by a few Indian banks for deposits below 2 crores.

Additionally, in the present time, an INR 10,00,000 FD with 7% interest over 20 years provides you with approx INR 38,00,007, while the same amount invested in an equity fund with a 12% annual return grows to approximately INR 95,00,005. Here, the difference is not a technicality; it is a major gap between preserving and creating wealth.

So yes, from the above information, it is clear that NRIs should look beyond fixed deposits. With liquid funds that match FD returns to equity funds that historically delivered 10%-14% annually over the long term, at every risk level, better options exist.

Moving ahead, let's know the best alternatives to NRE fixed deposits for NRIs in India.

With Savetaxs, file your ITR in India with expert guidance and 100% accuracy.

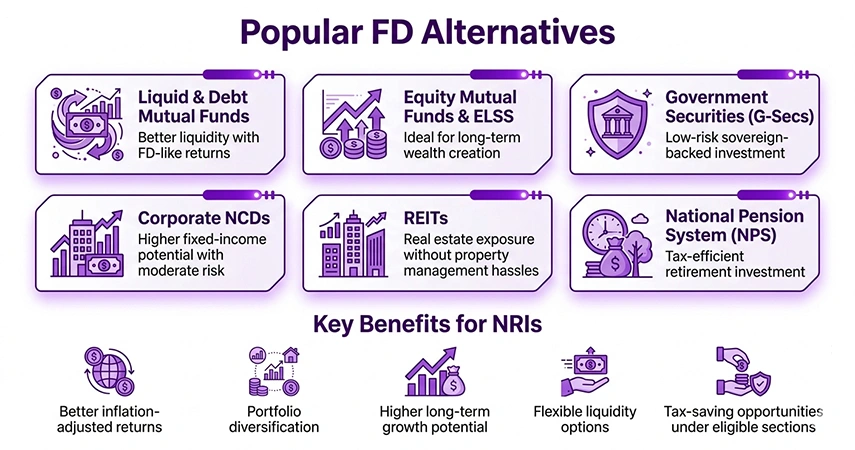

Here is the list of the best FD alternatives for NRIs in India:

Liquid and debt mutual funds for NRIs are the closest alternatives to fixed deposits, with the added benefit that you can exit anytime. With maturities under 91 days, liquid funds invest in short-term investments and offer an annual return of about 5.5% to 7%. Additionally, unlike FD, these investments do not charge a premature withdrawal penalty after 7 days and settle redemptions within 24 hours.

Apart from this, the taxation of debt mutual funds depends on the applicable tax provisions, acquisition date, and holding structure. Also, generally 30% TDS (maximum rate) is deducted on capital gains during redemption, which can later be adjusted while filing your income tax return. It is an ideal investment option for NRIs seeking FD-like returns without being in a fixed tenure.

If you have a financial goal of five years or more, equity mutual funds for NRIs are a good investment. With diversified options like flexi-cap funds, index funds, and large-cap funds, these have delivered 10%-14% historical returns annually over the long run.

Additionally, ELSS (Equity Linked Savings Scheme) offers a tax benefit to investors. These investments come with a three-year lock-in period. Also, if you have a taxable income in India, under Section 80C (up to INR 1,50,000 per year), under these investments, you qualify for tax deductions. ELSS among NRIs is one of the most underused instruments.

Moreover, NRI investments in equity mutual funds and ELSS with TDS deducted at source are taxed on capital gains. The taxation depends on the holding period, i.e., short-term and long-term.

These investment options are ideal for long-term wealth building, such as children's education, property purchase in 10 years, and more. However, returns on equity funds are not guaranteed as markets go through down periods. So invest in these funds if you have long-term investment plans.

G-secs are sovereign bonds issued by the Indian government. As these investments are backed by the government, you face zero default risk, do not require a broker, and yield generally 50-100 basis points above equivalent NRE FD rates.

Additionally, using the RBI Retail Direct platform, NRIs can directly invest in G-Secs, State Development Loans, and Treasury bills without any annual or intermediary cost. Apart from this, even after being an NRI, you get the same returns as institutional investors.

These investments face taxation on interest and capital gains. Considering this, interest income from Government Securities is generally taxed at the applicable Income Tax slab rates. On the other side, long-term capital gains (held > 1 year) are taxed at 12.5%, and short-term capital gains are taxed at slab rates generally without indexation.

Furthermore, these investments are an ideal option for risk-averse NRIs who want more returns above FD rates without equity exposure.

AAA or AA+ rated Non-Convertible Debentures (NCDs) from investment-grade companies generally offer yields that are 50 to 200 basis points more than bank fixed deposits for similar periods. These investments are listed on the Bombay Stock Exchange (BSE) and the National Stock Exchange (NSE). Additionally, you can buy them through a demat account linked to your NRE or NRO account.

When investing in these, it is vital to consider that you should avoid chasing the highest coupon rates. It is because compared to an AAA-rated NCD that provide 8.5%, a lower-rated NCD offering 11% returns carries significantly higher risk.

Furthermore, for NRIs, investments in NCDs in India under Section 195 are subject to a 20% TDS on interest income. Apart from this, long-term capital gains taxation on NCDs depends on their listing status and prevailing tax provisions under the Income Tax Act.

These investments are ideal for NRIs looking for a reliable fixed income that is more than the interest rates offered by FDs, and are okay with some corporate credit risk exposure.

India has publicly listed three Real Estate Investment Trusts (REITs), i.e., Embassy Office Parks, Brookfield India Real Estate Trust, and Mindspace Business Parks. This allows NRIs without the requirement to purchase property outright to invest in commercial real estate.

With historical returns averaging between 5% and 7% annually, these investments have the potential for profit through property value appreciation. Additionally, REITs distribute at least 90% of their income as dividends. Apart from this, units listed on the exchange can be purchased for INR 300 - INR 400 each.

REIT investments are taxed according to income type, i.e., interest (5% TDS/tax), dividends (10%-20% tax), and capital gains (12.5% for long-term listed). Furthermore, these investment options are ideal for NRIs who want real estate exposure without the issue of managing property from overseas- no maintenance and no tenants, and want regular income from real estate.

It is a government-regulated retirement savings vehicle available to NRIs aged 18 to 70 years. National Pension System invests in a mix of government securities, equity, and corporate bonds, providing market-linked growth with relatively low fund management charges.

However, the drawback of this investment is that funds are locked until age 60 with limited withdrawal options. Additionally, in NPS, contributions are eligible for tax deductions of up to INR 1,50,000 under Section 80C/80CCD(1), plus an additional INR 50,000 under Section 80CCD(1B), making a total tax exemption of INR 2,00,000. Apart from this, at 60, 60% of the corpus is free from taxation.

NPS is an ideal investment option for NRIs who want to create a dedicated retirement corpus and do not need money before 60.

The above-mentioned NRI investment alternatives to FD, while handling the issues created by economic conditions and rising inflation, will also enhance their investment portfolio. Additionally, the right investment completely depends on your time horizon and the volatility you can handle.

Moving further, let's take a quick overview of FD and its other alternatives for NRIs with a comparison table.

The table below compares FD with its other alternative options available for NRIs based on indicative return, taxation, liquidity, capital safety, and inflation hedge.

| Instrument | Indicative Return | Tax (NRE Route) | Liquidity | Capital Safety | Inflation Hedge |

|---|---|---|---|---|---|

| NRE Fixed Deposit | 6.5% - 7.5% p.a. | Fully tax-exempt | Low (penalty on exit) | Guaranteed | Weak |

| Liquid/ Debt Fund | 6.5% - 8% p.a. | 12.5% LTCG above INR 1,25,000 | Very high (T+1) | Not guaranteed | Moderate |

| Equity Mutual Fund | 10% - 14% p.a. | 12.5% LTCG above INR 1,25,000 | High (T+2) | Market-linked | Strong |

| G-Secs (RBI Retail Direct) | 7% - 8.5% p.a. | Slab rate | Moderate | Sovereign-backed | Moderate |

| Corporate NCDs (AAA) | 7.5% - 9.5% p.a. | Slab rate | Moderate (listed) | Credit risk | Moderate |

| REITs | 5% - 7% yield + growth | Multi-component | High (exchange-listed) | Market-linked | Moderate-Strong |

| NPS | 8% - 12% est. | Partial tax exemption at maturity | Very low (locked to 60) | Regulated | Strong |

Moving forward, let's know the key factors NRIs should consider before investing in India.

Key factors NRIs should consider before investing in India are as follows:

This is the most important factor while investing. Match your investment vehicle to your actual financial timeline. For instance:

The most costly and common mistake NRIs make is investing long-horizon money into an FD for guaranteed returns and then watching inflation quietly erode it over time.

Your Residential Status changes your tax picture completely in India.

If you are planning to return to India, typically for 2 to 3 years, you hold RNOR status. It is a tax planning opportunity worth mapping carefully with a tax expert before you invest.

Choose the correct NRI account before you plan to invest in India.

When you earn returns from Indian investments in rupees, they will eventually become foreign currency. Compared to the US dollar, each year the value of the Indian rupee has generally lost about 3% - 4%. So, on your Indian investment, if you get a 12% return in rupees, it translates to around 8%-9% in dollars. Although it is a good return, it is vital to consider this currency conversion when planning big expenses or retirement in a foreign currency.

Capital gains on Indian investment may also be taxable in your residence country. In this, DTAA foreign tax credits provide tax relief. However, for this, you need to file the correct forms on time. Additionally, US-based NRIs also need to fulfill FBAR reporting obligations for Indian accounts exceeding USD 10,000 in total value.

These are some key things NRIs need to consider before investing in India. Additionally, to have a smooth investment journey, it is advisable to seek help from a financial expert.

Connect with Savetaxs and start your investment journey in India without any hassle.

Lastly, there are several fixed deposit alternatives for NRIs in India, including equity and debt mutual funds, REITs, non-convertible debentures, and more. To choose the right investment, consider factors such as risk tolerance, residential status, taxation rules, investment horizon, financial goals, and repatriation requirements.

Furthermore, if you need any assistance in your investment journey in India, connect with Savetaxs. The financial experts in our team will help you choose the right investment as per your financial goals, risk appetite, and time horizon.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1783598615351.webp&w=828&q=75)

_1781767087029.webp&w=828&q=75)