NRI Income Tax & Compliance

What Is Section 54B Of The Income Tax Act?What Is Section 54B Of The Income Tax Act?

Written by Hatim Dudhiyawala

RNOR is a transitional tax status. Also known as an intermediate category, RNOR (Resident Non-Ordinary Resident) is especially relevant for expatriates and returning NRIs returning to India.

In a nutshell, this residential status acts as a tax bridge between being an NRI and becoming a tax resident of India.

In this blog, we will discuss the key aspects of RNOR status, including its meaning, eligibility criteria, duration, tax obligations, and key compliance requirements.

The resident but not ordinarily Resident status is a transitional category under the Indian tax law.

This residential status is especially for individuals returning from abroad to India, offering them a partial tax exemption on their foreign income till they become tax residents of India.

Under this hybrid residential status, your foreign income is not entirely taxable in India.

To attain the Resident but not ordinarily resident (RNOR) status in a financial year, an NRI must meet any one of the following criteria:

In many cases, most expatriates or returning NRIs qualify for RNOR status after 1-2 years of returning to India.

To better understand the taxation of Indian and foreign income for RNOR, NRI, and resident residents, here is a table for clarity.

| Category | Taxation on Indian Income | Taxation on Foreign Income | The key benefits |

|---|---|---|---|

| NRI (Non-Resident Indian) | Taxed in India | Not taxed in India | The foreign income is fully exempted in India. |

| RNOR (Resident but not ordinarily Resident) | Taxed in India. | Not taxed in India unless the income source is controlled from India. | Partial tax relief for two to three years is provided. |

| Resident (Ordinary) | Taxed in India. | Taxed in India | No exemption is given |

Hence, RNOR provides the best of both the other residential statuses, namely NRI and a resident of India. Meaning you are a resident of India, so that you can invest freely in India. However, you are still enjoying most of the tax exemptions available to non-resident Indians (NRIs).

Below is a table that provides a clear understanding of which income for RNOR is taxable in India and which is not.

| Particulars of Income | RNOR Taxability |

|---|---|

| Income that has been earned, whether in foreign or India, that is received or is considered to be received in India. | Taxable |

| Any income that is deemed to accrue, arise, or accrue in India, even if the payment is received outside India. | Taxable. |

| Income generated from a business controlled from Indian, income arises or accrues outside India, and is received outside India. | Taxable |

| Any income that is sourced outside Indian, meaning which arises or accrues outside Indian and is received outside India during the previous year. | Non Taxable |

| Income that arises or accrues outside India, received outside India in the years preceding the current financial year, and then is remitted to India during the last year. | Non-taxable. |

To summarize, for RNOR, all income sources, such as salary received in India for services provided in India, rental income from a property in India, professional or business income earned in India, interest from an NRO account, and so on, are taxable in India.

Now, what is not taxable is income earned outside India, unless it is received directly in India or arises from a profession or business controlled or set up in India.

The benefits of resident but not ordinary resident (RNOR) stays last for two to three financial years after your return to India. However, it also depends on how long you have stayed abroad before that.

Hence, the duration of the RNOR period is not fixed for everyone. The longer you were an NRI, the longer you are eligible to receive the benefits of being an RNOR.

Once you meet the eligibility requirements to be an ordinary resident, your foreign income becomes taxable in India. This two- to three-year transitional window helps non-resident Indians adjust their financial affairs before becoming Indian residents for tax purposes.

Let us say you were an NRI for 15 years and returned to India in the financial year 2025-26. In this case, you can continue as an RNOR until FY 2027-28. Post this, you will be eligible to become a full resident.

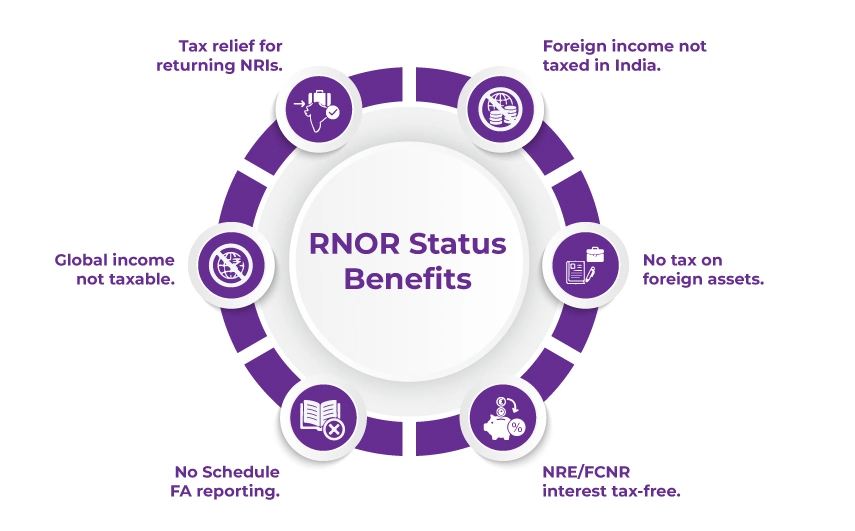

RNOR residential status comes with an array of tax advantages for individuals who are earning income from abroad or have any foreign assets.

Here is a list of some of the major benefits.

As aforementioned, an RNOR individual is not taxed on their foreign income in India unless it is received in India. Income such as interest from foreign bank accounts, dividends or capital gains earned from investments abroad, rental income from foreign properties, retirement or pension income, and more.

During the RNOR time period, income received or deemed received in India is taxable.

Any income earned from foreign assets is also exempt from Indian taxation while you are an RNOR.

Interest earned on FCNR (foreign currency non-resident) and NRE (Non-resident External) accounts is tax-free while you're on your RNOR periods.

Individuals on their RNOR status are not required to disclose their foreign assets in Schedule FA, unlike ordinary tax residents of India.

This exemption lets you avoid complex foreign asset reporting.

Individuals with RNOR status find this one of the biggest benefits: their global income is not taxed in India.

This is a great benefit for individuals who are still drawing income from other foreign countries or hold foreign assets there that generate income.

For non-residents in India planning to either gradually transition or return permanently, the RNOR residential status offers a tax-efficient status while you settle in India.

The following are a few key points to help you plan moving back to India using RNOR.

Yes, the benefits of RNOR are significant, but so are the risks of non-compliance. Many individuals either miss out on RNOR benefits or incur penalties due to errors.

Here is a list of 5 common RNOR mistakes individuals make, which you must be mindful of so that you don't end up losing the benefits.

No, just because you are returning from abroad does not mean you are RNOR by default. This residential status is evaluated and reduced each calendar year under Section 6 of the Income Tax Act.

Absolutely avoidable, yet many still make it. Even a single-day miscalculation can change your status from RNOR to ROR (resident and ordinary), triggering global taxation.

Hence, always keep copies of your passport or travel logs to evaluate the days you have spent in India in the current and preceding years.

Even if you have earned the income abroad and it is received directly into your Indian bank account, it is immediately taxable in India, even though you are in the RNOR case. Many individuals think that since it's a labor-intensive process, it won't be taxable, but it is taxable in India if the income is deposited in an Indian account.

Hence, to avoid this unnecessary tax implication, ensure that such income remains abroad only.

In a case where your foreign income is taxed abroad and is also taxable in India—for example, because of remittances—then to avoid double taxation and claim a relief under the Double Taxation Avoidance Agreement. You must file Form 67 before you file your income tax return.

The RNOR phase is best used when individuals do effective tax planning for their resident indian statuses. However, many individuals still fail to capitalize on it. Tax planning can be strategic, focusing on how well you can restructure your offshore holdings, remittances, Indian tax implications, and more.

There is no separate income tax return for RNORs; only the correct residential status must be disclosed when filing an Income tax return. Depending on your source of income, ITR-2 or ITR-3 may apply.

The resident but not ordinarily resident RNOR residential status in India acts as a bridge between non-to full residency. So, if you are moving back to India or spending an extended time here after staying abroad, you need to assess your residential status under Section 6 (1) and Section 6 (6) of the Income Tax Act.

At Savetaxs, we help NRIs across the UK, US, UAE, Australia, Singapore, and more navigate this transitional phase easily. Our experts ensure you get expert-backed tax planning, FEMA compliance, and cross-border structuring.

If you are planning to move back to India and are on an extended stay, connect with Savetaxs — we serve clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1782996918646.png&w=828&q=75)

_1782911003992.webp&w=828&q=75)