_1767077669.webp&w=828&q=75)

Open NRI Account Online - Types, Process, Timeline & More

Read More

An NRI fixed deposit is a type of savings account that Non-resident Indians open in India. It is one of the popular investment choices among NRIs seeking a secure and safe way to increase their savings. The fixed deposits in India provide high returns to NRIs. Additionally, with the fastest-developing economies among the NRIs, India has become a favorable option for investment for fixed deposits.

However, NRIs often make mistakes when investing in fixed deposits. This further impacts their financial planning and returns. Considering this, to help you better understand NRI fixed deposits in India, we will provide you with a comprehensive overview in this blog. So read on and gather all the details.

NRI fixed deposits are an attractive investment option in India and offer several benefits. Here are some of the key advantages of these accounts to NRIs:

These were some of the key benefits of NRI fixed deposits in India. Moving ahead, let's know the different types of these.

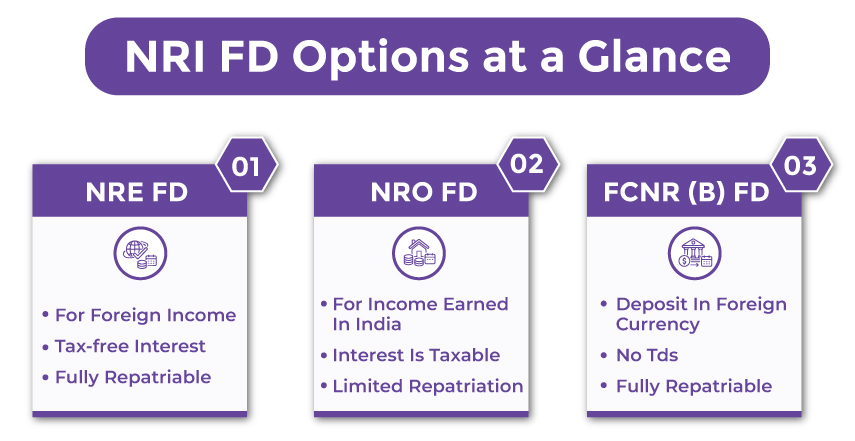

There are three different types of NRI fixed deposits you can choose from:

These were the different NRI fixed deposit accounts that you can opt for as per your financial goals. Moving further, let's know the interest rates on NRI fixed deposits offered by the best banks for NRI fixed deposits in India.

Connect with Savetaxs and simply open your NRE/ NRO account without issues in a few steps.

The table below shows the interest rates on NRI fixed deposits by account type and the best banks for NRI fixed deposits in India.

| Account Type | Bank | Tenure | Rate of Return (p.a.) |

|---|---|---|---|

| NRE Fixed Deposits Rates | HDFC Bank | 1 year to 10 years | 6.60% - 7.20% |

| SBI Bank | 1 year to 10 years | 6.80% - 7.10% | |

| Axix Bank | 1 year to 10 years | 6.70% - 7.10% | |

| Federal Bank | 1 year to above 5 years | 6.80% - 7.40% | |

| NRO Fixed Deposits Rates | HDFC Bank | 7 days to 10 years | 3.00% - 7.20% |

| SBI Bank | 7 days to 10 years | 3.00% - 7.10% | |

| Axis Bank | 7 days to 10 years | 3.00% - 7.10% | |

| Federal Bank | 7 days to above 5 years | 3.00% - 7.40% | |

| FCNR (B) Fixed Deposit Rates in US Dollar | HDFC Bank | 1 year to 5 years | 3.90% - 5.50% |

| SBI Bank | 1 year to 5 years | 3.80% - 5.00% | |

| Axis Bank | 1 year to 5 years | 4.10% - 5.60% | |

| Federal Bank | 1 year to 5 years | 3.90% to 5.25% |

These were the best banks for NRI fixed deposits in India, and the interest rate they offer on the investment. Moving ahead, let's know the taxation rules for NRI fixed deposits in India.

When it comes to taxation, NRO and NRE FDs are treated differently. The interest earned from the NRE and FCNR (B) FDs is tax-free in India. Considering this, as mentioned above, this makes them an attractive option for NRIs seeking to increase their returns.

On the other hand, tax at source (TDS) is deducted by your bank on the interest you earn from your NRO FDs. The current rate of TDS for NRIs is 30%. However, the TDS rate can be lower if your residency country has signed a tax treaty, i.e., DTAA (Double Taxation Avoidance Agreement) with India. It helps you avoid paying taxes twice on the same income.

Further, it is vital to note that, even if your interest income is tax-free in India, you might be required to pay taxes on it in the country where you currently reside. So, to avoid any tax obligations and legal issues, it is advisable to consult a tax advisor who can help you understand the tax laws of India and other countries.

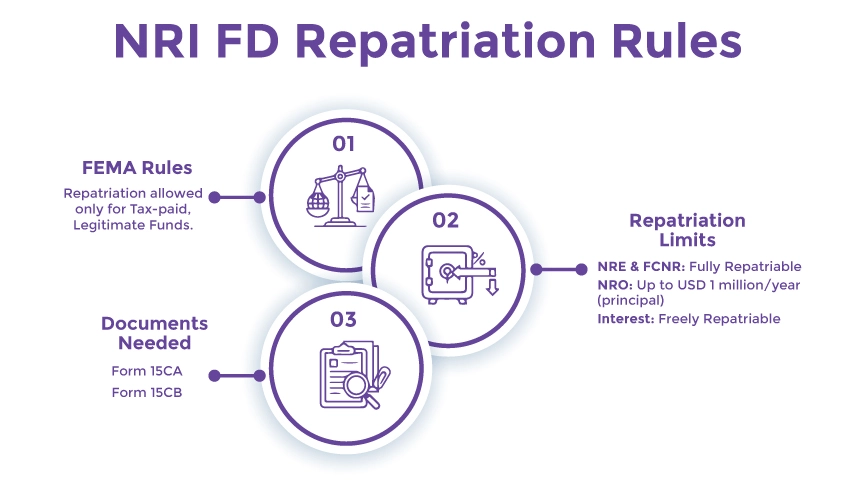

Now, let's know the NRI FD repatriation rules.

The NRI FD repatriation rules are primarily governed by the Foreign Exchange Management Act (FEMA). These rules are introduced to safeguard both the tax and legal status of funds moving in and out of India. Further, let's know the NRI FD repatriation rules that NRIs should know.

So, this was all about the NRI FD repatriation rules. Moving ahead, let's know the documents NRIs need to submit to open a fixed deposit account in India.

Take control of your investment options with Savetaxs and unlock the full potential of your returns.

Here is the list of documents required to open an NRI fixed deposit account in India:

These were the documents that you generally required to open an NRI fixed deposit account in India. Moving on, let's see how you can open this account in India.

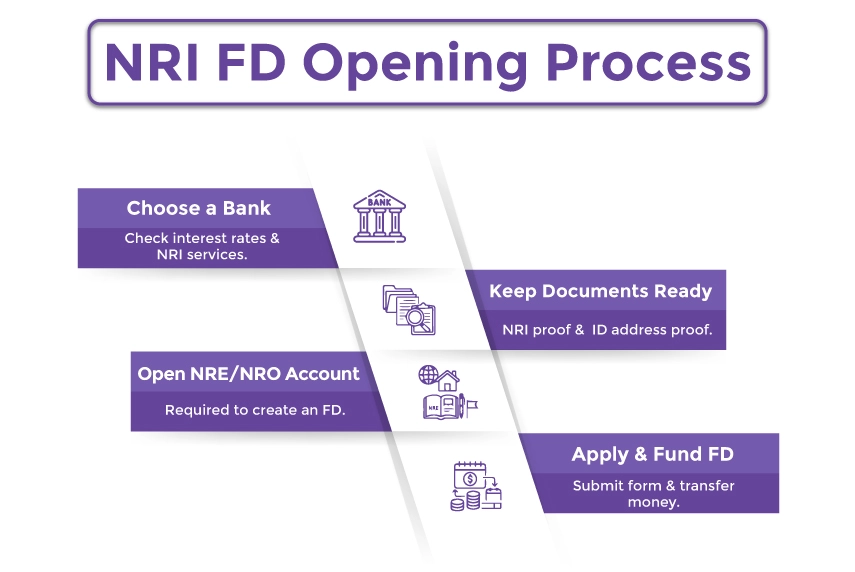

Opening an NRI fixed deposit account in India is straightforward. Here is how you can do so:

This is how you can open an NRI fixed deposit account in India by following the account mentioned earlier.

Lastly, NRI fixed deposits are a great way for NRIs to grow and save their money in India. These investments offer guaranteed returns, safety, and tax benefits to NRI investors. However, like any financial decision, it is vital to consider your financial situation and goals.

Further, if you are still confused and seeking a liable financial planner who has experience in NRI investments, connect with Savetaxs. We have a team of professionals who can help you make the right investment choices in India to deliver higher returns.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs

_1768474831.webp&w=828&q=75)