_1770727924470.webp&w=828&q=75)

Difference Between FATCA and CRS Compliance

Read More

_1781070005858.webp&w=3840&q=75)

For Assessment Year 2026-27, income tax return filing is officially open. Well ahead of the ITR deadline, on March 30, 2026, the Central Board of Direct Taxes (CBDT) notified all ITR forms, ITR-1 to ITR-7. Considering this, you can start filing your returns for the Financial Year 2025-26 without waiting until July.

However, this year is not a routine tax-filing season, as the CBDT has introduced several enhanced ITR-filing disclosure requirements across all ITR forms. It aims to improve transparency, aligning income reporting with digital payment systems and avoiding misuse of tax deductions. Considering this, nearly every taxpayer category, from restructuring capital gains and F&O trading to foreign asset declarations and donation traceability, is affected.

Confused? This blog contains new ITR filing disclosures and key changes that you need to know before ITR filing 2026-27. So read on and clear all your doubts.

Before moving forward to the new disclosure and key changes in ITR filing 2026-27, let's first know the due dates for ITR filing for AY 2026-27 as per the taxpayer category.

| Taxpayer Category | ITR Form | Due Date |

|---|---|---|

| Salaried individuals, pensioners with income up to INR 50,00,000 and one house property | ITR-1 (Sahaj) | July 31, 2026 |

| Individuals/ HUFs with multiple house properties, capital gains, foreign income | ITR-2 | July 31, 2026 |

| Non-audit business/ professional taxpayers | ITR-3/ ITR-4 | August 31, 2026 (Extended this year) |

| Tax audit cases | ITR-3/ ITR-5/ ITR-6 | October 31, 2026 |

| Transfer pricing cases | ITR-3/ ITR-6 | November 30, 2026 |

| Belated return (if you missed the original deadline) | Any applicable ITR form | December 31, 2026 |

| Revised return (to correct errors in original filing) | Any applicable ITR form | March 31, 2027 (date extended from December 31) |

| Updated return ITR-U (missed or incorrect past returns) | ITR-U | March 31, 2031 (48 months from the end of AY) |

Further, the due date for ITR-3 and ITR-4 (non-audit professional and business cases) has been extended to August 31. This makes them distinguish from salaried individuals whose deadline for Form ITR-3 and ITR-4 is July 31. Under the Finance Act, 2026, there is a new provision that provides additional time to small professionals and businesses with extra time to file their returns.

Additionally, under Budget 2026, the deadline for filing a revised return has been extended from 9 months to 12 months from the end of the relevant tax year. Apart from this, a fee of INR 1000 applies to individuals with an income up to INR 5,00,000, and a fee of INR 5,000 for all taxpayers if revised after December 31.

Now, moving ahead, let's know according to your income time which ITR form you should file for AY 2026-27.

The table below showcases the ITR form that should be filed for AY 2026-27:

| ITR Form | Who Should File |

|---|---|

| ITR-1 (Sahaj) | Salaried individuals, pensioners with gross income not more than INR 50,00,000, and one or two house properties (expanded this year), income from other sources, LTCG under section 112A up to INR 1,25,000 |

| ITR-2 | Individuals/ HUFs with capital gains, more than two house properties in India, unlisted equity shares, foreign assets/ income, and a director in a company |

| ITR-3 | Individuals/ HUFs with business or professional income not covered under the presumptive scheme |

| ITR-4 | Individuals, HUFs, and firms (excluding LLPs) under presumptive taxation- sections 44AD, 44ADA, 44AE income up to INR 50,00,000 |

| ITR-5 | LLPs, Partnership Firms, BOIs, AOPs, and other entities (not trusts or companies) |

| ITR-6 | Companies (other than those claiming tax exemption under section 11) |

| ITR-7 | Research institutions, political parties, trusts, and other entities are required to file under sections 139(4A) to 139(4F). |

*Note: Even though the Income Tax Act, 2025, came into effect from April 1, 2026, the ITR form for AY 2026-27 is still governed under the Income Tax Act, 1961. Considering this, the Act will come into force from AY 2027-28.

Moving further, let's know the new disclosures for AY 2026-27 as per the ITR form type.

ITR-1, also popularly known as Sahaj, is the simplest ITR form. With new reporting requirements, ITR-1 has become more taxpayer-friendly this year.

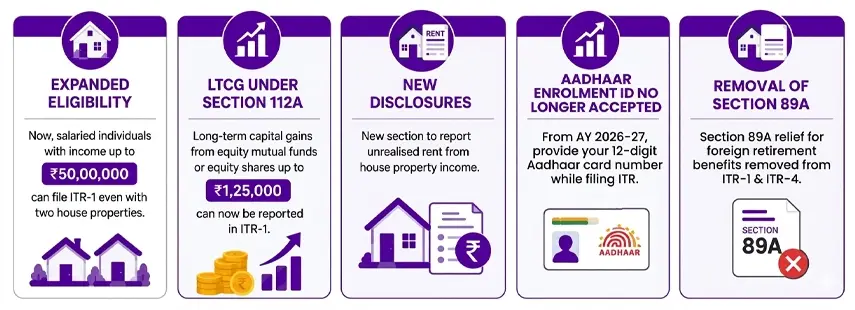

Previously, the ITR-1 form was filed by taxpayers with income up to INR 50,00,000 and who owned a single house property. From AY 2026-27, now salaried individuals with INR 50,00,000 and two house properties are also allowed to file ITR-1. This removes the need for millions of taxpayers who need to file ITR-2 only because they own a second home or a rented-out flat.

Taxpayers with long-term capital gains from equity mutual funds or equity shares not exceeding INR 1,25,000 can now directly report in the ITR-1. Earlier, for long-term capital gains, taxpayers needed to file ITR-2.

To report unrealized rent from house property income, ITR-1 added a new section. It is good for landlords who have not been able to collect house rent from tenants.

From AY 2026-27, when filing the ITR, taxpayers need to provide their 12-digit Aadhaar card number. Now, as a substitute, you will no longer use your Aadhaar Enrolment ID to file the ITR.

Under Section 89A, the tax relief available for Indian residents with retirement benefits accounts in foreign nations has been removed from ITR-1 and ITR-4. Considering this, taxpayers with such income need to file ITR-2 or ITR-3.

These are new ITR filing disclosures made in the ITR-1 form. Moving forward, now let's know the ITR-2 form disclosures.

The ITR-2 form is filled out by residents, HUFs, and NRIs whose income is more than INR 50,00,000 and has income from multiple sources. It includes income from capital gains, foreign assets, rental property, dividends, and more. However, taxpayers with business or professional income are not eligible to fill out this form.

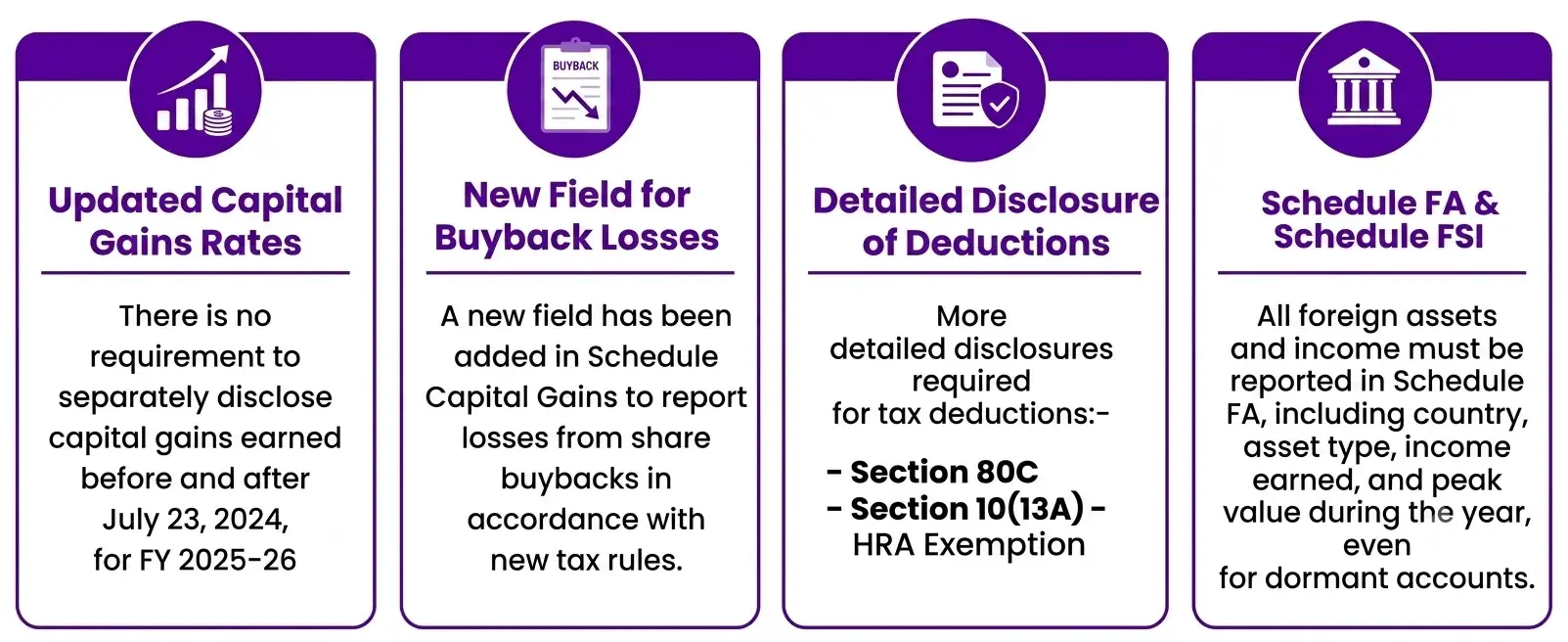

Now, taxpayers no longer need to separately disclose capital gains earned before and after July 23, 2024, for FY 2025-26. These requirements have been removed from all relevant ITR forms. Considering this, the applicable capital gains tax rates are as follows:

To report losses from share buybacks, a new field has been added in ITR-2, i.e., Schedule Capital Gains. The changes are made in consideration of the introduction of new tax rules, ensuring proper tracking of such transactions.

Now, more detailed disclosures are required for tax deductions available under Section 80C and HRA. Considering this:

Foreign holdings face tighter rules, too, in new ITR filing disclosures. This includes overseas bank accounts, property abroad, foreign investments, and stakes in foreign entities. Considering this, report all of it under Schedule FA. Additionally, mention the country, asset type, any income earned, and the peak value during the year. Even if you have a dormant account with no income, you still need to mention it.

This applies to:

The Schedule FA and Schedule FSI are only available in ITR-2 and ITR-3. Apart from this, under the Black Money (Undisclosed Foreign Income and Assets) Act, non-disclosure of foreign assets results in severe consequences, including facing legal obligations. To avoid this, the Income Tax Department actively cross-verifies the information through the Automatic Exchange of Information (AEOF) structure.

Crypto stays firmly under the scanner. So if you purchase or sell Ethereum, Bitcoin, NFTs, or any virtual digital asset, you need to mention it in Schedule VDA in the ITR-2. Under this section, you need to enter the asset type, purchase date, cost, sale date, and sale value. Apart from this, a flat 30% tax is imposed on capital gains, with no set-off of losses against other gains. Even small trades or losses need to be mentioned in it.

This was all about the changes made in the ITR-2 form for AY 2026-27. Moving ahead, let's know the changes made in the ITR-3 form.

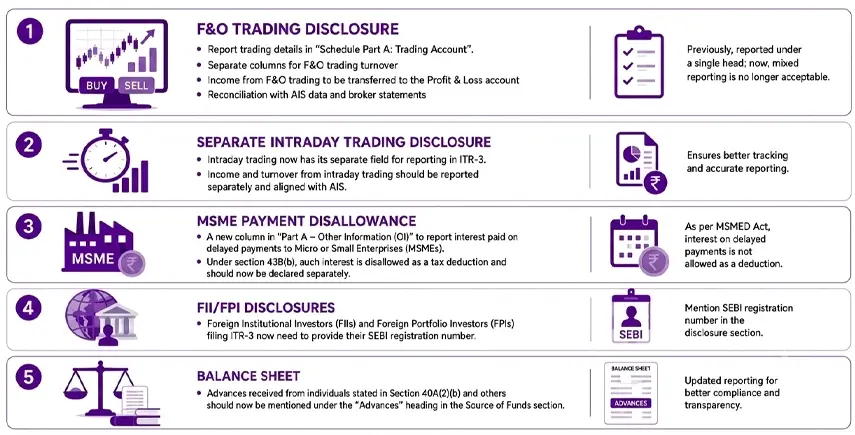

ITR-3 is for individuals, HUFs, and NRIs who have income from business or profession. Considering this, the key changes in the form for AY 2026-27 include:

Futures & Options (F&O) traders now need to report their trading details in "Schedule Part A: Trading Account." It includes the following things:

Previously, these were reported under a single head; now, mixed reporting is no longer acceptable.

Similarly, now intraday trading also has its separate field for reporting in ITR-2. Considering this, income and turnover from intraday trading should be reported separately and aligned with AIS.

Under the MSMED Act, to report interest paid on delayed payments to Micro or Small Enterprises (MSMEs), a new column in the ITR-3 has been introduced- "Part A- Other Information (OI). Under section 43B(h), such interest is disallowed as a tax deduction and should now be declared separately.

Foreign Institutional Investors (FIIs) and Foreign Portfolio Investors (FPIs) who are filing ITR 3 now need to provide their SEBI registration number. It should be mentioned in the disclosure section.

The updated ITR-3 form has brought a little change in the reporting of balance sheets. Considering this, advances received from individuals stated in Section 40A(2)(b) of the Income Tax Act and others should now be mentioned under the "Advances" heading in the Source of Funds section.

This was all about the major changes in the ITR-3 form. Now, moving further, let's discover the changes made in the ITR-4 form in the new ITR filing disclosures in AY 2026-27.

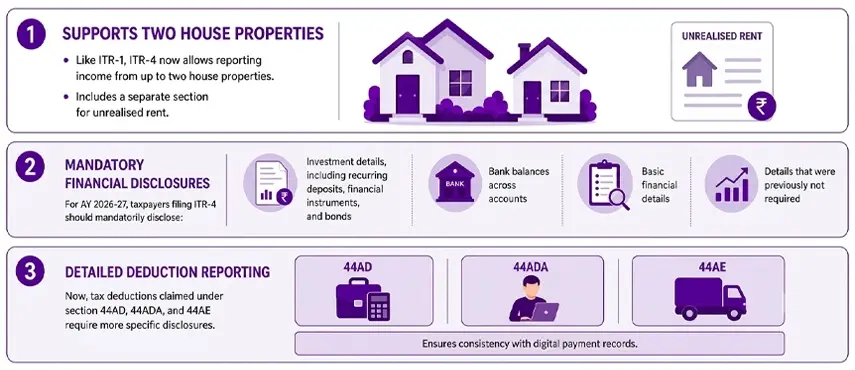

ITR-4 or Sugam is the ITR form filled by small businesses, professionals, and freelancers with a simple income structure, who choose presumptive taxation. Additionally, taxpayers who do not have detailed books of account. Further, let's know the key changes introduced in this ITR form.

Like ITR-1, ITR-4 is now also allowed under the presumptive taxation scheme to report income from up to two house properties. Additionally, ITR-4 now also includes a separate section for unrealized rent.

For AY 2026-27, taxpayers filing form ITR-4 should mandatorily disclose:

Now, tax deductions claimed under section 44AD, 44ADA, and 44AE require more specific disclosures. It ensures consistency with digital payment records.

These are the key modifications made under ITR-4. Now moving forward, let's know the new ITR filing disclosures common across all ITR forms.

Fulfill your tax obligations in minutes, and avoid the stress of deadlines with Savetaxs.

The new ITR filing disclosures common across all ITR forms are as follows:

Taxpayers claiming tax deductions under Section 80GGC (donations made to registered political parties) now need to disclose:

It is a new mandatory field introduced in all the ITR forms. The aim behind introducing it is to improve transparency and traceability in political funds. Previously, the contribution amount and date were mentioned under this section.

For claiming tax deduction under section 80F for charitable donations, taxpayers also need to mention:

It aims to prevent fraudulent donation claims, which previously became a significant compliance issue.

Across all ITR forms, a new field "secondary address" has been introduced. Considering this, the contact information section now separately mentions primary and secondary mobile numbers and email IDs. This change aims to reduce communication failures from the Income Tax Department when the primary contact is not working.

Earlier, the representative assessee needed to provide their name, PAN, address, and capacity. Now, tax filing is simplified for the assessee. Considering this, from AY 2026-27, they only need to mention the following things:

To indicate whether the tax return is filed by the taxpayer or the representative assessee, a new checkbox has been added across all ITR forms.

Now, the asset and liability detailed disclosure under Schedule AL is only required if your total income is more than INR 1 crore. This removes the compliance burden for taxpayers who previously needed to disclose the details of their assets.

In all ITR forms, the Annual Information Statement (AIS) and Taxpayer Information Summary (TIS) are the key sources of pre-filled information. Now, the data covers a wide range of transactions from multiple sources. It includes bank interest, capital gains from broker platforms, property sale proceeds, mutual fund redemptions, and high-value spends

These are the new ITR filing disclosures common in all the ITR forms for AY 2026-27. To avoid errors or penalties, file your returns according to them.

Finish your ITR in minutes with complete accuracy and maximize your refunds with Savetaxs.

Lastly, the ITR filing disclosures and changes for AY 2026-27 showcase one clear goal, i.e., transparency. Considering it, this year, basic reporting is not enough; instead, the information you mentioned in your ITR should match your own records and the data of the department. From capital gains and foreign assets to donations and crypto, now your financial life connects through TIS and AIS. Therefore, before filing, review your information carefully.

Furthermore, at Savetaxs, we understand that tax changes can be overwhelming, and it becomes more difficult if you are an NRI. So, whether you are filing your ITR or navigating through the latest tax changes, tax experts in our team help you stay compliant and certify your filings are accurate.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Shaw brings 8 years of experience in auditing and taxation. He has a deep understanding of disciplinary regulations and delivers comprehensive auditing services to businesses and individuals. From financial auditing to tax planning, risk assessment, and financial reporting. Mr Shaw's expertise is impeccable.

Want to read more? Explore Blogs

_1770810988642.webp&w=828&q=75)

_1771224750019.webp&w=828&q=75)

_1771243586808.webp&w=828&q=75)

_1771243559271.webp&w=828&q=75)