Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

Capital appreciation, high rental yield, a close connection to the homeland, and so on. All this makes investing in India an attractive option for NRIs.

Non-resident Indians do contribute a good share to the growth of the Indian economy by making right and profitable investments, but this is not the case for all. Many NRIs who don't understand the Indian government's investment regulations end up losing everything.

In this guide, we will discuss 10 problems NRIs face when investing in India and the solutions to those problems.

1) NRIs face an array of problems when investing in India, including limited investment options, complex taxation, limited market awareness, difficulties with property management, and more.

2) Despite any challenges, NRIs can successfully invest in India by seeking professional help, conducting research on the investment type they want to pursue, and staying updated on Indian tax laws.

3) Here are some actionable steps that NRIs must take to avoid any unnecessary investment issues:

The NRIs must comply with an array of regulations specific to their investment type and chosen NRI status. This means that, under Reserve Bank of India (RBI) regulations, once an Indian resident attains NRI status, they cannot operate their old resident bank accounts for any transactions.

They are required to open designated NRI bank accounts, such as NRE accounts and NRO accounts. Moreover, as an NRI, you must obtain a PIS account for investment-related to the stock market, and to adhere to real estate ownership limitations.

Additionally, they are required to update their Know Your Customer (KYC) details.

In a nutshell, some key regulations are complex for NRIs, such as using NRIs' specific bank accounts, cross-border taxation and Double Taxation (DTAA), KYC updates, and so on.

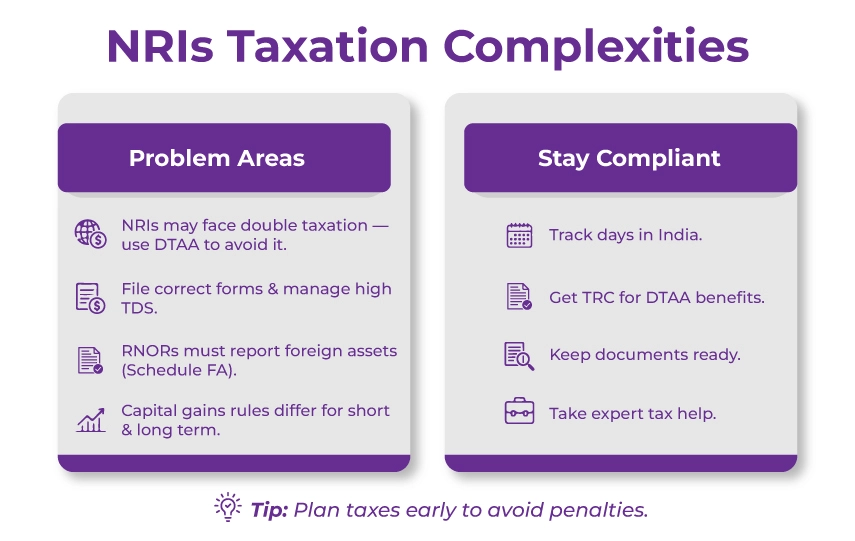

NRIs are considered susceptible to double taxation on income earned in India. However, India has signed a double taxation avoidance agreement (DTAA) with more than 100 countries to mitigate this.

But yes, understanding the specific tax treaty with the NRI's residence country and then claiming its benefits by filing the appropriate forms is crucial.

Apart from DTAA, working with the high tax deducted at source (TDS) rates and ensuring compliance with them is also essential.

Additionally, NRIs, especially those classified as this Resident or RNOR (which usually end if the stay in India exceeds the set number of days), must meet specific requirements to report all foreign earnings and assets while filing ITR in India using Schedule FA.

If not, penalties are imposed.

The complexities of taxation also determine when capital gains for NRIs are taxed in India. This means capital gains taxation for NRIs also involves complex rules for each holding period, including short-term and long-term capital gains, deductions, reinvestment tax exemptions, and more.

There is a trend of not investing in non-fungible tokens (NFTs) and cryptocurrencies without understanding their legitimate use cases. Non-resident Indians should invest in such digital assest which the Indian Law does not approve.

Young NRIs or those unfamiliar with Indian tax laws or Indian laws in general tend to invest in these digital assets with the expectation of high returns.

However, NRIs must be aware of the legal consequences and tax implications of such financial assets in India to avoid last-minute hassles. Additionally, please invest or allocate your funds to financial assets that are legally recognised in India.

Non-resident Indians (NRIs) often complain about the investment process, as it is quite delayed. Many background checks are required, which delays every investment process.

To avoid being stuck in the long-delayed process, NRIs are advised to use the investment services of credible banks.

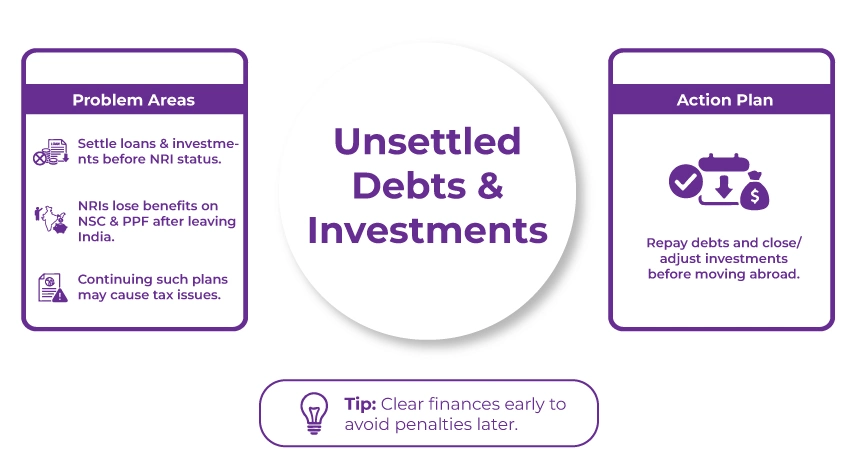

Before attaining the NRI status, an individual must settle their debts and investment plans. This is because NRIs cannot avail themselves of the benefits or advantages they received in India.

Let us say, for example, investments made in a National Savings Certificate (NSC). The interest earned on this investment is not subject to taxation under Section 80 of the IT Act. And a resident who has attained the NRI status cannot continue with this particular investment plan.

The same applies to the Public Provident Fund (PPF).

In a nutshell, it is wise to repay all such loans and settle the investments before leaving the country to avoid penalties or notices.

An NRI investor must abide by the above-discussed hitches to have a profitable investment portfolio. In case of any doubts, you can consult an expert NRI taxation consultant so that you ensure a portfolio is diversified and profitable.

There is no doubt that NRI taxation in India is quite a complicated aspect, but with expert guidance, you can get it done like a breeze. Savetaxs is one such NRI taxation expert that has been serving NRIs with the best taxation consultancy services in India. Our expert brings more than 30 years of combined experience, making them a trusted partner for individuals seeking NRI taxation in India. By now, we have a service serving thousands of clients across the USA, UAE, UK, Australia, and more.

Savetaxs is a taxation strategist who specializes in helping you stay compliant with Indian tax laws, all while maximizing your assets and minimizing your tax liability.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)