_1784547039242.webp&w=828&q=75)

NRI Income Tax Compliance

30+ Important Income Tax Terms in India You Need to Know30+ Important Income Tax Terms in India You Need to Know

Written by Shubham Jain

Section 112 of the Income Tax Act governs the taxation of long-term capital gains arising from specified capital assets such as property, unlisted shares, bonds, and certain securities that are not covered under Section 112A. The applicable tax rate generally ranges from 12.5% to the prescribed rate depending on the nature of the asset and taxpayer category.

In this comprehensive guide, we explain the latest Section 112 provisions, tax rates, exemptions, NRI implications, DTAA benefits, and tax-saving opportunities for FY 2025-26.

| Particulars | Details |

|---|---|

| Applicable Provision | Section 112 of Income Tax Act |

| Tax Type | Long-Term Capital Gains (LTCG) |

| Applicable To | Residents, NRIs, HUFs, Firms, LLPs, Companies |

| Covered Assets | Property, Bonds, Debentures, Unlisted Shares, Certain Securities |

| Tax Rate | 12.5% or applicable rate depending on asset type |

| Indexation Benefit | Available only in specific situations |

| Exemptions Available | Section 54, 54EC, 54F, 54B, 54GB |

| ITR Forms | ITR-2, ITR-3 |

| Capital Loss Set-Off | Allowed against LTCG only |

Section 112 of the Income Tax Act provides the tax rules for long-term capital gains arising from the transfer of specified long-term capital assets that are not covered under Section 112A.

In simple terms, if you sell certain assets after holding them for the prescribed period and earn a profit, the gain may be taxable under Section 112.

Section 112 governs taxation of long-term capital gains on specified assets such as immovable property, listed securities, unlisted shares, and zero-coupon bonds that are not covered under Section 112A.

Recent capital gains tax reforms have significantly changed how long-term capital gains are taxed in India.

The government streamlined asset classification into two primary holding periods:

| Asset Category | Long-Term Holding Period |

|---|---|

| Listed Securities and Equity Investments | More than 12 Months |

| Immovable Property, Unlisted Shares and Most Other Assets | More than 24 Months |

The earlier 36-month holding period has been removed.

These changes simplify capital gains taxation and make it easier for taxpayers to determine whether gains qualify as short-term or long-term capital gains.

Taxpayers should review the latest capital gains provisions before computing tax liability, especially for property transactions, securities, and unlisted shares.

Section 112 applies to:

Resident Individuals

Non-Resident Indians (NRIs)

Hindu Undivided Families (HUFs)

Partnership Firms

Limited Liability Partnerships (LLPs)

Domestic Companies

Foreign Companies

Trusts and Other Taxable Entities

The following long-term capital assets are generally taxable under Section 112:

| Asset Type | Covered Under Section 112 |

|---|---|

| Listed Securities (other than Section 112A assets) | Yes |

| Zero-Coupon Bonds | Yes |

| Unlisted Shares | Yes |

| Unlisted Securities | Yes |

| Immovable Property | Yes |

| Debentures | Yes |

| Government Securities | Yes |

| Gold Bonds (where applicable) | Yes |

| Other Long-Term Capital Assets | Yes |

Section 112A specifically applies to:

| Asset Type | Covered Under Section 112A |

|---|---|

| Listed Equity Shares | Yes |

| Equity-Oriented Mutual Funds | Yes |

| Units of Business Trusts | Yes |

Provided the applicable Securities Transaction Tax (STT) conditions are satisfied.

The classification of assets as long-term or short-term depends on the holding period.

| Asset Type | Long-Term Asset | Short-Term Asset |

|---|---|---|

| Listed Equity Shares | More than 12 months | Up to 12 months |

| Equity Mutual Funds | More than 12 months | Up to 12 months |

| Listed Securities | More than 12 months | Up to 12 months |

| Unlisted Shares | More than 24 months | Up to 24 months |

| Immovable Property | More than 24 months | Up to 24 months |

The tax rate under Section 112 depends on the nature of the long-term capital asset and the taxpayer's residential status.

| Asset Type | Tax Rate |

|---|---|

| Listed Securities (other than assets covered under Section 112A) | 12.5% |

| Zero-Coupon Bonds | 12.5% |

| Unlisted Shares and Securities (for eligible NRIs) | 12.5% |

| Immovable Property | 12.5% without indexation (subject to applicable provisions) |

| Other Long-Term Capital Assets | As prescribed under the Income Tax Act |

The ₹1.25 lakh annual exemption available under Section 112A does not apply to Section 112.

Health and Education Cess at 4% applies in addition to the tax.

Surcharge may apply depending on the taxpayer's total income.

Before calculating tax liability, taxpayers should verify whether the asset falls under Section 112 or Section 112A, as different tax rates and exemptions may apply.

Follow these steps:

Determine the amount received from the sale of the asset.

Subtract:

Cost of acquisition

Cost of improvement (where applicable)

Transfer expenses

LTCG = Sale Value – Eligible Deductions

Reduce exemptions claimed under:

Section 54

Other applicable provisions

Apply the applicable LTCG tax rate under Section 112.

Add applicable surcharge and 4% health and education cess.

Mr. A sells a residential property.

| Particulars | Amount |

|---|---|

| Sale Price | ₹80,00,000 |

| Cost of Acquisition | ₹50,00,000 |

| LTCG | ₹30,00,000 |

Tax is calculated on the net taxable capital gain after claiming eligible exemptions.

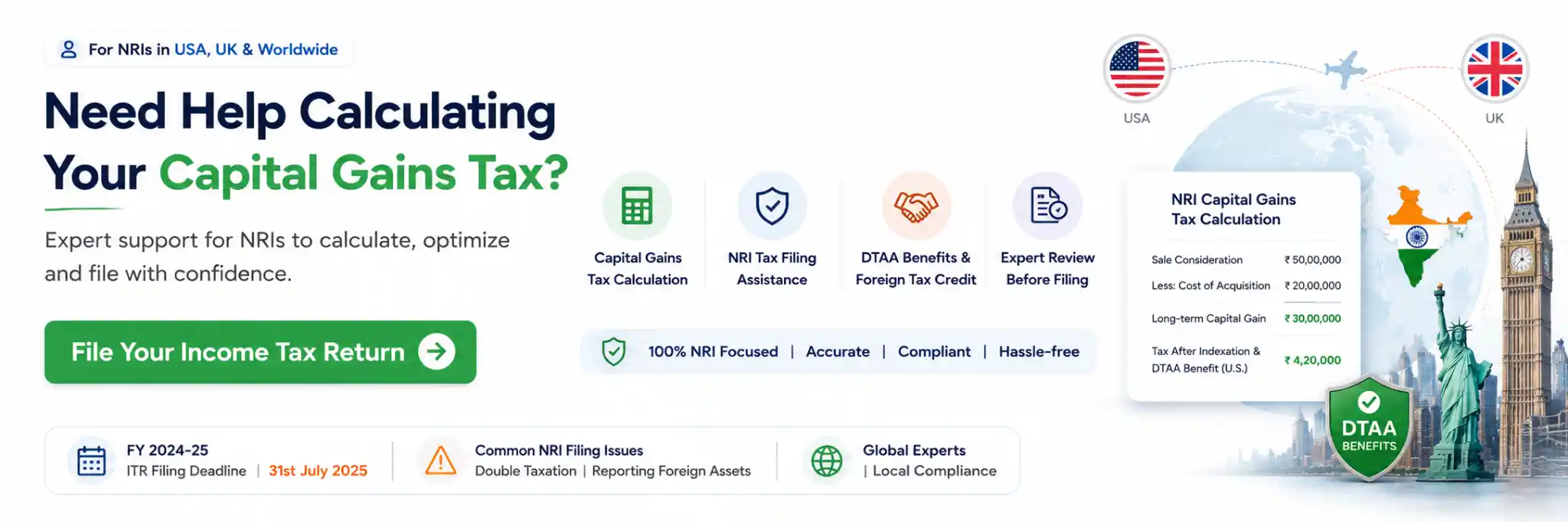

An NRI sells a property in India and earns LTCG of ₹40 lakh.

The buyer may deduct TDS under Section 195. The NRI can:

Apply for a lower TDS certificate

Claim exemptions

Claim DTAA relief if eligible

Adjust actual tax liability while filing ITR

If an NRI sells unlisted shares after the prescribed holding period, the gains may qualify as long-term capital gains taxable under Section 112.

If a taxpayer earns:

LTCG = ₹10 lakh

LTCL = ₹4 lakh

Taxable LTCG becomes:

₹10 lakh − ₹4 lakh = ₹6 lakh

Section 112 is particularly relevant for Non-Resident Indians (NRIs) who earn long-term capital gains from assets located in India.

Common transactions include:

Sale of residential property

Sale of commercial property

Transfer of inherited property

Sale of gifted property

Sale of unlisted shares

Sale of bonds and securities

When an NRI sells property in India, the buyer is generally required to deduct TDS under Section 195 of the Income Tax Act.

In many cases, the TDS deducted may be significantly higher than the actual tax liability.

Yes. NRIs can apply for a Lower Deduction Certificate through Form 13.

Benefits include:

Reduced TDS deduction

Improved cash flow

Faster access to sale proceeds

Lower refund dependency

NRIs may be eligible to claim benefits under the Double Taxation Avoidance Agreement (DTAA) between India and their country of residence.

Subject to treaty provisions, NRIs may:

Avoid double taxation

Claim foreign tax credit

Reduce overall tax burden

After paying applicable taxes and complying with FEMA regulations, NRIs may repatriate eligible sale proceeds outside India through authorized banking channels.

Professional tax planning can help NRIs optimize TDS, exemptions, DTAA benefits, and repatriation procedures.

Several exemptions can help reduce or eliminate tax liability.

Available when capital gains from a residential property are invested in another residential property within prescribed timelines.

Available when LTCG is invested in specified capital gains bonds within the prescribed period.

Applicable when capital gains from certain assets are invested in a residential house property.

Available for capital gains arising from the transfer of agricultural land subject to conditions.

Provides relief where eligible gains are invested in specified businesses or startups, subject to prescribed conditions.

Long-term capital loss can be adjusted only against long-term capital gains.

It cannot be adjusted against:

Salary income

Business income

House property income

Short-term capital gains taxable under certain provisions

Unabsorbed LTCL may be carried forward for up to 8 assessment years, subject to timely filing of the income tax return.

Long-term capital gains under Section 112 are generally reported in:

Applicable for individuals and HUFs without business income.

Applicable for taxpayers having business or professional income.

Sale consideration

Cost of acquisition

Cost of improvement

Transfer expenses

Exemptions claimed

Capital loss adjustments

The gains are reported under Schedule CG of the income tax return.

| Particulars | Section 112 | Section 112A | Section 111A |

|---|---|---|---|

| Nature of Gain | Long-Term Capital Gain | Long-Term Capital Gain | Short-Term Capital Gain |

| Assets Covered | Property, Bonds, Unlisted Shares | Listed Equity Investments | Listed Equity Transactions |

| STT Requirement | Generally Not Mandatory | Mandatory | Mandatory |

| Exemption Threshold | No ₹1.25 Lakh Benefit | Available Subject to Conditions | Not Applicable |

| Tax Category | LTCG | LTCG | STCG |

| Applies To | Residents & NRIs | Residents & NRIs | Residents & NRIs |

Avoid these common errors:

Incorrectly classifying assets as long-term or short-term

Ignoring available exemptions

Not claiming DTAA benefits

Incorrect cost calculation

Missing capital loss adjustments

Incorrect ITR reporting

Not applying for lower TDS certificates

Failing to maintain supporting documents

Section 112 plays a crucial role in determining the taxation of long-term capital gains on property, securities, unlisted shares, bonds, and other capital assets. Understanding the applicable tax rates, exemptions, reporting requirements, and NRI-specific provisions can help taxpayers reduce errors and optimize their tax position.

For NRIs, proper planning around TDS, DTAA relief, capital gains exemptions, and repatriation can significantly improve tax efficiency and compliance.

Whether you're selling property in India, transferring unlisted shares, claiming DTAA benefits, or filing your tax return, SaveTaxs experts can help you accurately calculate capital gains, claim eligible exemptions, and stay fully compliant with Indian tax laws.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784546974133.webp&w=828&q=75)

_1784376356528.webp&w=828&q=75)

_1784375756402.webp&w=828&q=75)