US Tax Filing and Compliance

Substantial Presence Test Explained: How NRIs Determine US Tax Residency?Substantial Presence Test Explained: How NRIs Determine US Tax Residency?

Written by Shubham Jain

The tax credit vs tax deduction has a simple difference: the tax deduction reduces your taxable income, whereas the tax credit reduces your tax bill or tax liability. Both the tax credit and the deductions are among the most rewarding parts of the entire tax return preparation process.

Both reduce your overall tax bill, just the way of doing so is different.

The Tax Credit: This directly reduces the taxable amount you owe, providing a dollar-for-dollar federal reduction on your overall tax liability. For instance, let's say you have a tax credit worth $1,000; then it will directly lower your overall tax bill by $1,000.

The Tax Deduction: The deduction reduces the amount of your income that is subject to taxes. The tax deductions lower your entire taxable income by a percentage. This percentage, however, depends on your federal income tax bracket.

Let's say there is a deduction of $1000, and you fall into a 22% tax bracket. In this case, your deduction amount will be 22% of the $1000. This means that the deduction will save you $220 (22% of the $1000) on your overall tax bill.

In this blog, we will clarify the difference between a tax credit vs tax deduction through a simple example.

We will demonstrate an example showing how a tax deduction and credit work on your overall taxable income.

| - | $10,000 Tax Deduction | $10,000 Tax Credit |

|---|---|---|

| Your AGI | $100,000 | $100,000 |

| The Tax Deduction | - | $10,000 |

| Taxable Income | $90,000 | $100,000 |

| The Tax Rate* | 25% | 25% |

| Calculated Tax | $22,500 (25% of $90,000) |

$25,000 (25% of $100,000) |

| Tax Credit | - | $10,000 |

| Your Final Tax Bill | $22,500 | $15,000 |

*Example Rate: The United States has a progressive tax system.

Now, via the example, we can see that both benefit in lowering your taxes, but how they work is totally different.

Usually, the tax credit has a greater impact because it aims directly at reducing the taxes you owe, rather than reducing the income that you will be taxed on.

For an NRI, a tax credit is more valuable than a tax deduction. The main difference is how these two reduce your tax liability.

Here are a few things to consider about the tax credits:

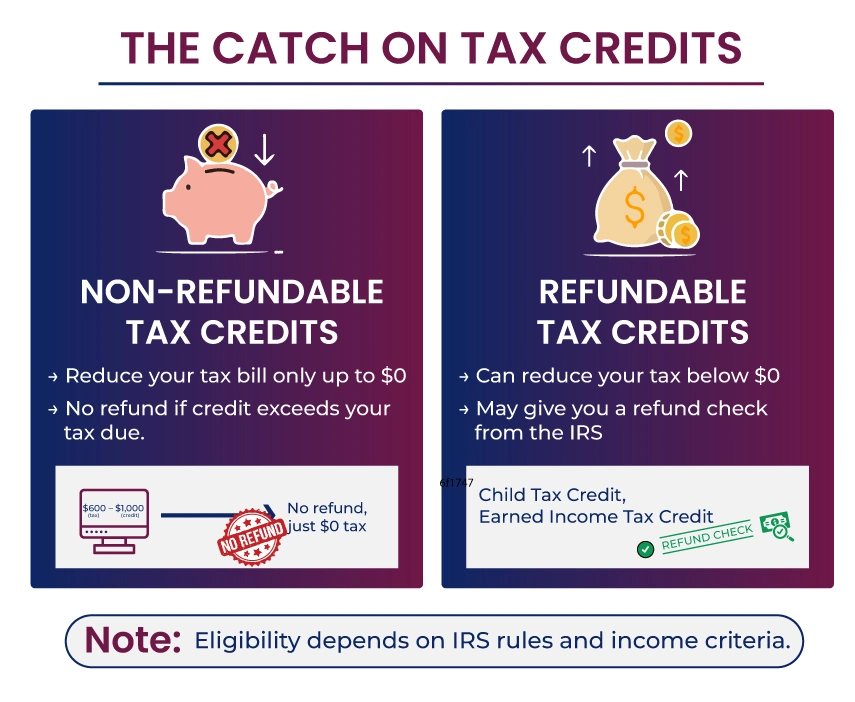

Non-redundant tax credits: Such Tax Credits mean that even if you owe less in taxes, you will not get the full value of the credit if it takes your federal tax bill to zero.

For example, a $600 tax bill, when combined with a $1000 non-refundable credit, does not mean that you will get a $400 tax refund check. All you will get is $0 tax bill.

Refundable tax credits: If you are qualified to take a refundable tax credit, such as the child tax credit or the earned income tax credit, then the value of these credits exceeds your tax liability and may even result in a refund check.

However, please note that the Internal Revenue Service (IRS) has specific criteria that you must meet to qualify for either nonrefundable or refundable credits.

There are two types of tax deduction methods that individuals can choose from, namely the standard deduction method and the itemized deduction method.

This is kind of a one-size-fits-all type of decision. The IRS determines a standard and fixed deduction amount. You do not have to do anything to qualify for the Standard Deduction, nor do you have to provide any documentation.

You can claim the standard deduction on Form 1040. However, depending on your filing status, the amount will vary.

| Filing Status | Standard Deduction Amount |

|---|---|

| Single | $15,750 |

| Married Filing Separately | $15,750 |

| Head of Household | $23,626 |

| Married Filing Jointly | $31,500 |

| Surviving Spouses | $31,500 |

The itemized deductions allow you to take advantage of various deductions, including medical expenses, charitable donations, and others. After calculating your total itemized deduction, if it exceeds the value of the standard deduction, you must choose itemizing your deduction.

Use Form 1040 and Schedule A to claim the Itemized Deductions.

Choosing between the standard deduction or itemized deduction is an either-or situation. Meaning you can choose either one of the two in a tax year, but not both.

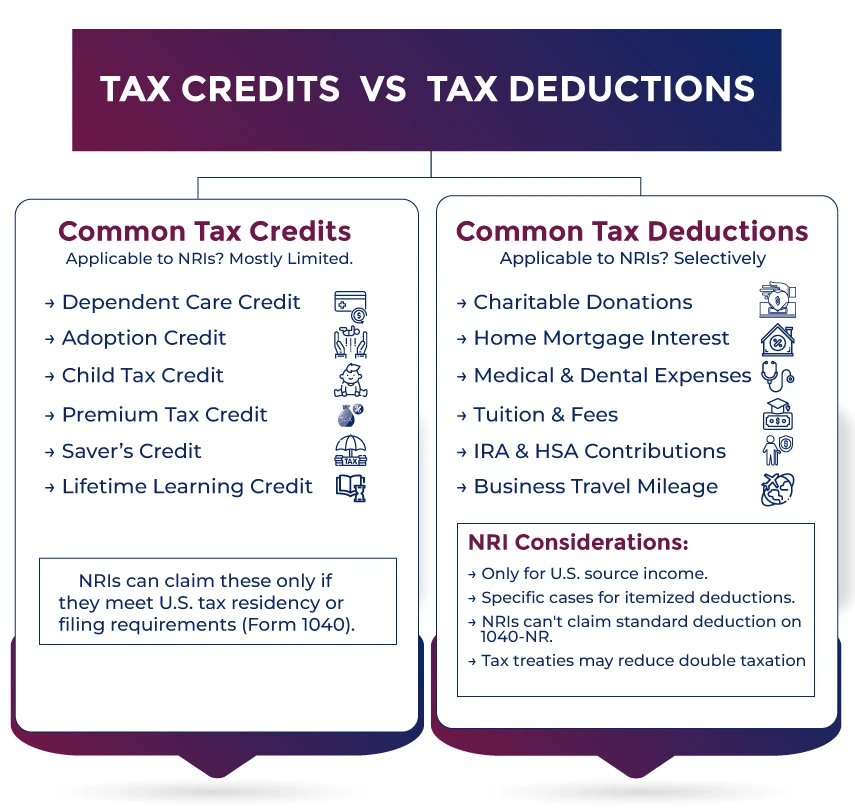

Below is a list of common tax credits and deductions that individuals must be aware of.

To know which credit might be eligible for your situation, you must talk with an expert.

Here are some examples of the common tax deductions. A few of them, such as the itemized deduction, are considered above-the-line deductions, while others, like the student loan interest deduction, are not. The above-the-line deductions can be claimed as separate deductions even if you choose not to itemize your deductions.

The tax credit vs the tax deduction both help in reducing the total amount you will have to pay in taxes, but their implementation is different. However, understanding both is crucial. The tax return preparation process was straightforward.

Be it tax deductions or tax credits, our experts will help you claim the maximum of both, ensuring your overall tax bill is reduced significantly. Savetaxs has expertise in US taxation and has helped thousands of US residents and citizens with their tax queries. We serve our clients 24/7 across all time zones, so connect with us today and reduce your overall tax bill.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784032485815.webp&w=828&q=75)