US Tax Forms

IRS Form 1040 Schedule 2: Applicability, Steps, DeadlinesIRS Form 1040 Schedule 2: Applicability, Steps, Deadlines

Written by Hatim Dudhiyawala

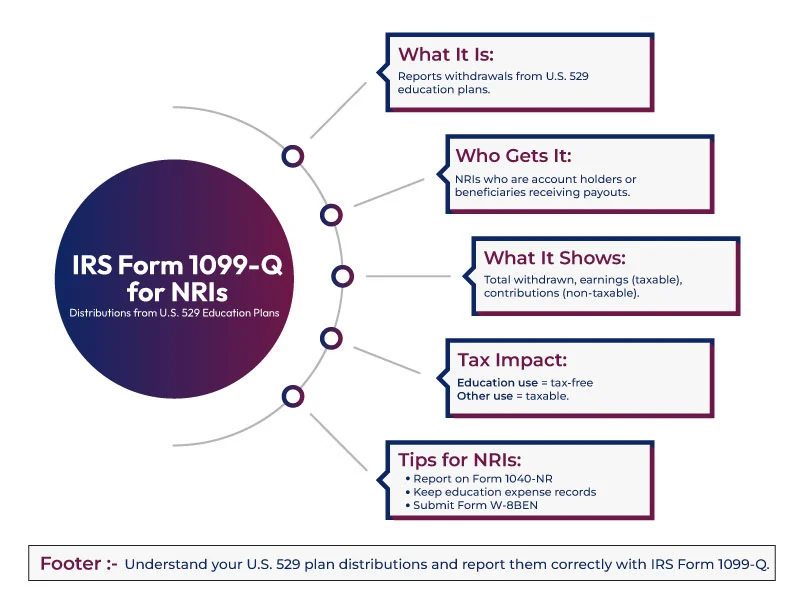

Form 1099-Q is an IRS tax form sent to students who received distributions from qualified education programs. It includes education programs like a 529 plan or a Coverdell education savings account (ESA or CESA). This form consists of the distribution details that you get from your qualified learning program.

Are you also out of your tax-free education account, paying your education expenses? Then, at the end of the year, you may also get this form from your administrator. Furthermore, knowing about the tax implications of these distributions is important. It helps in avoiding tax penalties and increases your education-related benefits.

Here, to provide you with an understanding of the Form 1099-Q, we have mentioned all the information about it on this blog. So, read on and learn when and how to include this form in your tax return.

The IRS Form 1099-Q tax form reports the distributions from qualified education programs. This form is issued to individuals who received payments from qualified education programs. This includes Coverdell Education savings accounts (ESAs) and 529 plans.

These distributions, including rollovers, can be taxable. Additionally, using the information from the IRS, you should determine the tax liability of any distribution. Then, this form is used by taxpayers for filing both their state and federal tax returns if the distributions are taxable.

Further, depending on how the money is spent by the account holder, taxes are imposed on the distribution. Depending on the withdrawals made, the details mentioned on the Form 1099-Q should be reported by the IRS and state agencies.

For instance, one year ago, a parent for their children set up a Coverdell ESA plan. During college, the child uses the payments from this qualified education program for tuition expenses. Here, the child will get a copy of Form 1099-Q from his college account administrator.

This was all about IRS Form 1099-Q. Moving ahead, let's know the different types of education programs included in this form.

At present, there are two types of qualified education programs included in Form 1099-Q. These are Coverdell ESA and 529 plans. Although the tax-free treatment of both forms is the same at the time of distribution. However, there are several differences in these accounts. Want to know what they are? Read the next section and get your answers.

Here is everything that you need to know about the Coverdell ESA qualified education program.

The contribution limits of Coverdell ESA include:

Here are all things about the 529 plan:

This was all about different types of educational programs included in Form 1099-Q. Moving ahead, let's know who can file this form.

The Form 1099-Q is generally filed by the employee or administrator who handles and manages the qualified education programs. They are accountable for sending a copy of the filled form to the IRS and the beneficiary. Here, the beneficiary is the one who receives the distribution. This form can also be filed by anyone who has made a distribution from a 529 plan. It is also called a qualified tuition program (QTP).

QTPs and CEASs are investment accounts designed to be used for qualified higher education expenses. A Form 1099-Q determines the amount made over the year being stated from the accounts in gross distribution. These are then compared to the incurred educational expenses over the year.

In case the qualified education expenses are less than the gross distribution, then the excess distribution amount is taxable. Considering this, it should be reported on the tax return of the taxpayer. However, if the educational expenses are more than the distribution. In this scenario, the excess amount can be used to claim the Education Tax Credit.

This was all about who can file Form 1099-Q. Moving further, let's know who receives this form.

Generally, the Form 1099-Q is given to the beneficiary student. Additionally, the taxable amount of the distribution is stated in the income tax return of the beneficiary. Here, the distributions that are used for the payment of non-qualified expenses are liable to be taxed. Additionally, a penalty of 10% is also imposed on the earnings portion of the amount withdrawn.

Further, there is often confusion about who uses this form during their tax return, i.e., the beneficiary student or the account owner. Here, the account owner can be a parent or other relative. Considering this, the individual who gets the funds and whose Social Security number is stated on the form can use it on their ITR.

Generally, if a student receives the distribution, then they pay very less or no tax. However, it is not the same case for someone other than students using the distribution. Also, the younger students often fall below the threshold limit of a federal income tax return.

So, it totally depends on the individual who receives the funds and whose SSN is stated in the form to get the Form 1099-Q. Moving ahead, let's know how to fill out this form.

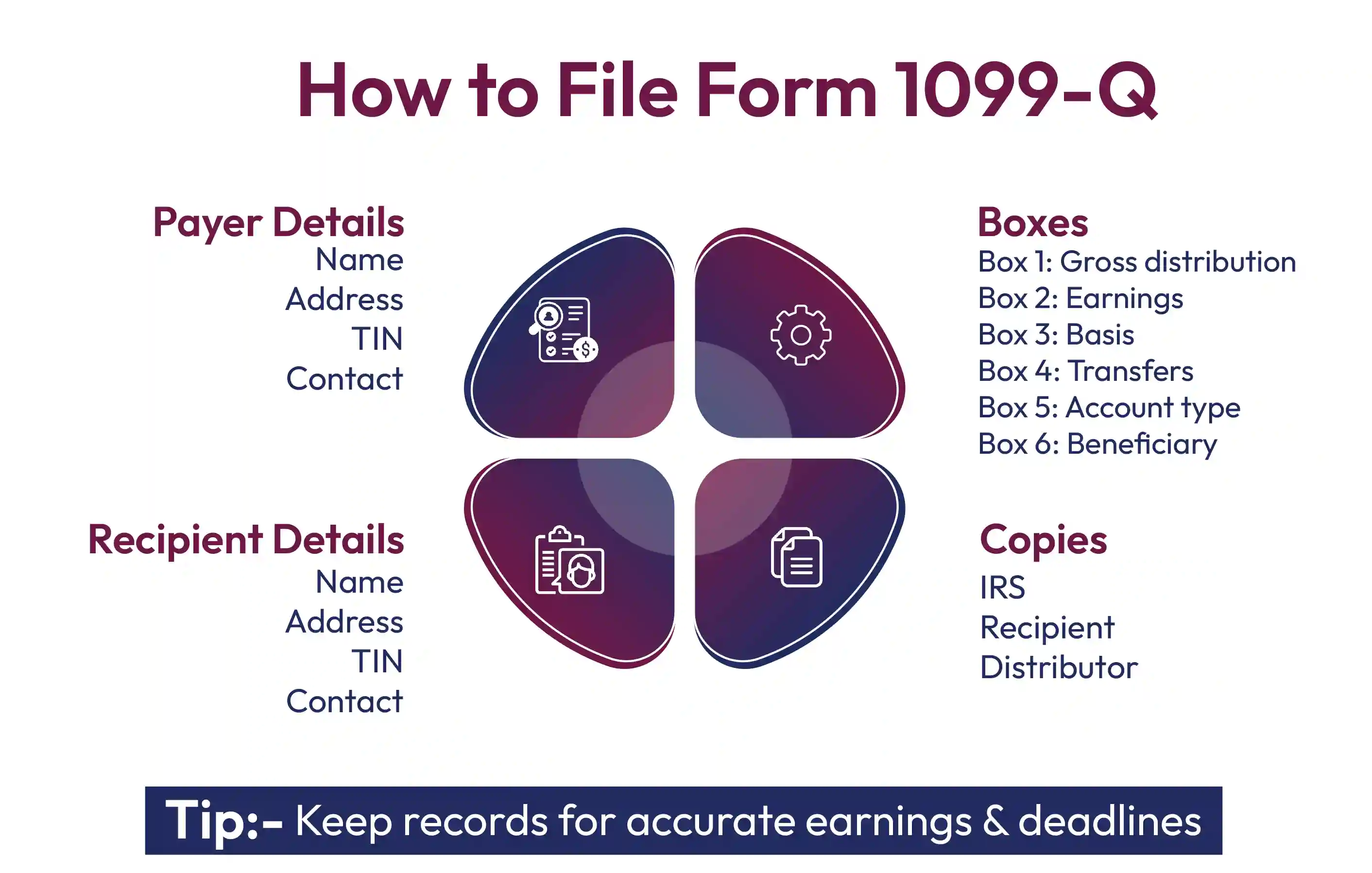

To fill out Form 1099-Q, you need to mention the name and address of the payer/ trustee. Along with it, you also need to mention the tax identification number (TIN) and contact number. Additionally, you also need to provide the complete details of the recipients in the form. It includes the name, address, contact number, account number, and TIN for individuals, which is generally a Social Security number. Furthermore, the form also involves six numbered boxes:

Furthermore, individuals who fill out this form, in the blank space, can mention a distribution code below boxes 5 and 6. The distributor files three copies of the form. The first copy of the files with the IRS, the second copy is sent to you, and the third copy is retained by the distributor. Generally, you receive the form in your email.

This was all about how to fill out Form 1090-Q and the boxes it consists of. Moving further, let's know the tax implications for the beneficiary.

For beneficiaries, many of the qualified education programs, the amount stated on the Form 1090-Q is not mentioned in their tax return. However, if the total distribution in the tax year is more than your qualified education expenses. In this scenario, you need to mention some of the earnings stated in box 2 as your taxable income. Additionally, you also need to pay an extra 10% on it.

Here, your adjusted expenses will be equal to the total of your qualified expenses minus the tax-free assistance you get, such as Pell grants & scholarships. Confused? Let's better understand it with an example.

For instance, your qualified education expenses are $10,000, and from a Pell grant, you get $2000. Additionally, both boxes, i.e., 1 and 2, in your Form 1099-Q report $8000 gross distribution and earnings of $1000. Here, your adjusted qualified education expenses are $8000. This means that in your tax return, you did not need to report any distribution you received from an education program.

This was all about the tax implications of the beneficiary. Moving ahead, when you receive this Form 1090-Q.

You generally receive the Form 1099-Q in any year when you do a fund transfer between your accounts or take a distribution. Your administrator sent you this form for your qualified tuition plans. Typically, you get this form no longer than early February, following the end of the tax year.

Further, administrators should also provide a copy of each form to the IRS by March 31 if it is sent electronically or February 28 if sent through courier.

Lastly, IRS Form 1099-Q- Payments for qualified education programs ensures you are paying the correct amount of taxes on your distributions received. If the form shows, you owe any taxes, then you need to include that amount on your federal and state tax returns.

Furthermore, if you are still confused about this form and looking for assistance, connect with Savetaxs. We have a team of professional tax advisors who can help you with your query. Also, assist you in filing your IRS and claiming the available tax refunds. So, do consider us if you are looking for reliable tax services in the US.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1781869155314.webp&w=828&q=75)