Understanding Form 1065 (Partnership Tax Return)

Read More

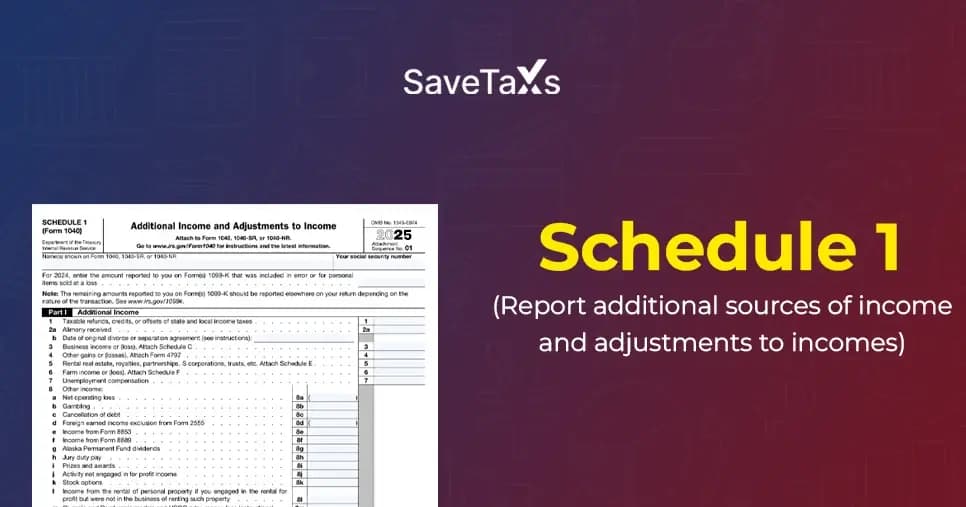

Form 1040 Schedule 1 is used to claim additional income sources that are not included on IRS Form 1040. It includes unemployment compensation, prize or award money, and gambling winnings. Also, you can use Schedule 1 to claim specific tax deductions. Some information mentioned on Schedule 1 must be accompanied by an additional form or Schedule.

You can use Schedule C to report income or loss from a business. Additionally, use Schedule E to report rental income or royalties. In case you have extra income sources this year, read this blog to know whether you need to file a Schedule 1 tax form.

Form 1040 is the main form; the schedules and other forms are just there to support or report what you cannot add in Form 1040.

This form states additional income types that are not included on Form 1040, along with some additional adjustments to income.

Not everyone is required to attach Schedule 1 to their federal income tax return. The IRS has shortened and simplified the old Form 1040. It enabled individuals to include forms as per the requirement.

You are only required to file Schedule 1 if you receive any of the additional income types or adjustments, which we will discuss further in the blog.

Before the IRS and the Treasury redesigned IRS Form 1040 in 2018, it comprised several lines to report various types of income. It also included a line for "Other Income". Additionally, it consisted of numerous lines for making adjustments to income, also called "above-the-line" deductions.

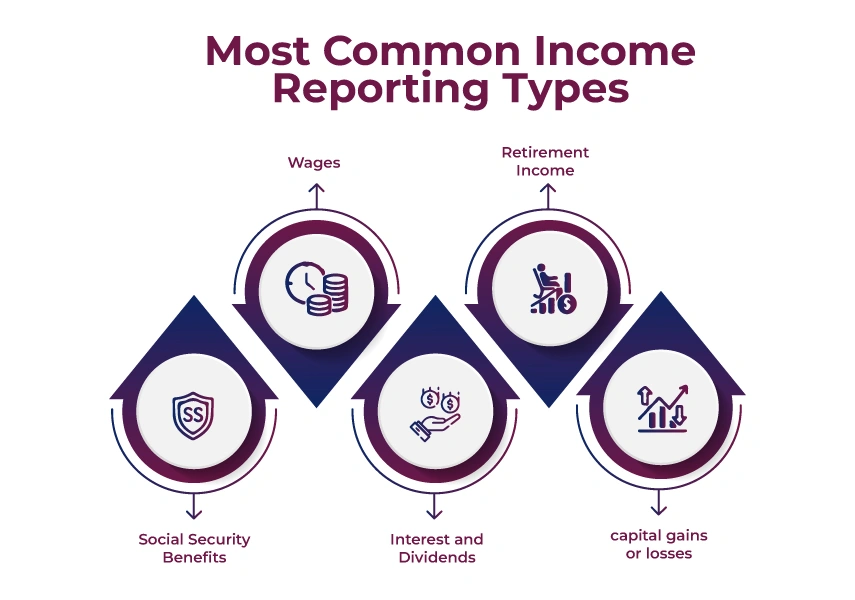

Now, in the latest version, taxpayers get a lot of lines reporting the most common income types. It can include:

Remember that the requirement to report any other type of income and adjustments to income has not disappeared. Instead, the reporting requirements have shifted to Schedule 1.

When Congress reduced the reporting thresholds for issuing Form 1099-K, Schedule 1 was updated to add a new section. It was added to simplify entering those amounts that don't affect your taxable income. It includes amounts added on a 1099-K reported in error.

The transfer of personal money and the sale of personal items at a loss, and hence they are neither taxable nor deductible.

Additionally, imposed in 2024 in line 8v in Section 1 for reporting digital assets acquired as ordinary income that aren't reported anywhere else on your tax return. It can include income received from forks, staking, or mining, which aren't wages on line 1a, or capital gain or loss reported on Form 8949 and Schedule D.

You will use part I of Schedule 1 to report the following income types:

Now, line 8 of Schedule 1 is the comprehensive for other income types that are unsuitable for the predefined lines. Such as prizes, awards, or winnings from gambling.

When you navigate down to the Schedule 1 lines, you may find that some of the items also need an additional form or schedule. For example, you will be required to attach Schedule C to your return in case you acquire profit or loss from a business.

Also, you will have to attach Schedule E if you want to report rent and royalties as income. After you have filled out all your various income types on Schedule 1. Then, the aggregate is transferred to line 8 of Form 1040.

If you receive all your income from the five categories mentioned on Form 1040, you don't need to use Schedule 1. The five categories are wages, interest, and dividends, retirement income, social security benefits, and capital gains or losses.

Part II of Schedule 1 includes adjustments to income, including:

These deductions can be valuable for several taxpayers for mainly two reasons. Firstly, these deductions reduce your adjusted gross income directly. It helps in uncovering the possibility of claiming other deductions and getting tax credits that have adjusted gross income limits.

If you wish to claim the full American Opportunity Tax Credit. Then, your modified adjusted income for 2025 must be $80,000 or below ($160,000 or less if you are married filing jointly). Also, if your modified adjusted gross income is above $90,000 ($180,000 for joint filers), you can't claim the credit.

Suppose you have an income of $91,000. However, you decided to contribute $3,000 to your health savings account, $8,000 to a SEP IRA. Also, paid a student loan interest, which added up $1,000.

Now, with a total of $12,000 in above-the-line deductions, your adjusted gross income would be $79,000. It means that you are probably eligible to claim the full American Opportunity Tax Credit.

Secondly, Schedule 1 adjustments to income are also valuable, as you are not required to itemize deductions to claim them. Above-the-line deductions help in lowering your income before applying either the Standard Deduction or itemized deductions.

Almost 90% of the taxpayers choose the standard deduction. However, above-the-line deductions are a helpful tax break that can be achieved by avoiding the extra paperwork of itemizing.

Schedule 1 Form 1040 is vital for those who have additional income sources and wish to claim adjustments to lower their taxability. It is an essential part of your tax return as it covers income and deductions that are stated directly on Form 1040. This form ensures that all income and adjustments are reported properly to the IRS.

You must complete Schedule 1 accurately to maximize your deduction and prevent hefty penalties. In case you find any difficulties with completing Schedule 1, connect with the team at Savetaxs.

We offer the best taxation services in the U.S, which can be seen by our satisfied base of clients. Savetaxs has a team of experts and professionals carrying more than 30 years of expertise and knowledge in the taxation field. Hence, if you need any help with Form 1040 or other US taxation forms, contact us right away. We are serving our clients 24*7 across all time zones: connect with us and experience expertise at your home.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Want to read more? Explore Blogs

Schedule 1 reports additional income, such as:

Common deductions reported on Schedule 1 include the following: