NRI Income Tax & Compliance

Tax Exemption Under Section 54GA for NRIsTax Exemption Under Section 54GA for NRIs

Written by Hatim Dudhiyawala

Whether an Indian Resident or an NRI, an increase in overall income has made tax planning an essential part of financial planning. Taxpayers are now seeking potential investment schemes to save on taxes. The Income Tax Act of India has various provisions that permit a taxpayer to claim an exemption, and one such provision is Section 54F.

This section of the Income Tax Act allows the taxpayer to claim a tax exemption on the sale proceeds of any capital asset, except for the residential property, by reinvesting the capital gain in the purchase or construction of a house property.

In this blog, we will explore Section 54F of Income Tax Act, covering who can claim, the amount of exemption available, and more.

Section 54F of Income Tax Act states that individuals and Hindu Undivided Families (HUF) can avail a tax exemption on capital gains income made by selling an asset, including land, gold shares, or anything other than a residential house, and then reinvesting the sale proceeds in a new residential property within a given time frame.

Here is how Section 54F of the Income Tax Act works for capital gains exemption:

Ensure that if any of the rules mentioned above to claim tax exemption under Section 54F are not met, the tax exemption is cancelled, and the entire capital gain will be taxable for the respective financial years.

For a taxpayer to qualify for the tax exemption on long-term capital gains, they must reinvest the net consideration sale proceeds from selling a non-residential asset in India into a new residential property.

Here is what net consideration means:

The total amount the taxpayer received by selling the assets is the full value of the consideration.

Now the seller must subtract any expenses that they have incurred specifically for the sale of the property, like the legal charges or the broker fees. Upon subtracting such charges, the amount left is the "net consideration" amount, which needs to be reinvested within the specified time frame.

As mentioned above, to claim tax exemption under Section 54F of the Income Tax Act, the taxpayer must be:

Calculating a tax exemption under Section 54F is no rocket science; in fact, it is based on a simple formula. Here is how you can calculate the Section 54F exemption.

Let us understand it with an example:

Mr Khemraj sold a land to Mr. Raj on 10th July 2024 for Rs 5 Crore, which Mr Khemraj originally bought for 50 lakhs in May 2020.

In August 2025, he purchased a residential house for three crore.

So can Mr Khemraj avail an exemption under Section 54F? Let us see:

Yes, he is eligible for the tax exemption. So, here is the capital gains calculation:

| Particulars | Amount |

|---|---|

| Sale Price | 5,00,00,000 |

| Indexed Cost of Purchase (5,00,00,000 * 365 / 301) | 60,20,900 |

| Long-Term Capital Gain | 4,39,79,100 |

Now, let us calculate the portion of exemption:

Exempt Capital Gains: 4,39,79,100 * (3,00,00,000/5,00,00,000)

Exempt Capital Gains: Rs 2,63,87,460

The taxable capital gains = 4,39,79,100 - 2,63,87,460 = Rs 1,75,91,64.

Note: From April 1, 2024, the maximum deduction available under section 54F is Rs 10 crore. This limit came into effect from April 1, 2024, but was initially introduced in the Union Budget 2023.

Let us now understand the differences between sections 54 and 54F of the Income Tax Act.

| Basis of Difference | Section 54F | Section 54 |

|---|---|---|

| Eligible Capital Asset | Tax exemptions are applicable on the sale of any capital asset other than residential property. | Tax exemptions are available on the sale of a residential property. |

| Amount of Exemption | Full or Partial Exemption allowed. | To the extent of long-term capital gain invested. |

| Reinvestment Requirement | Entire sale proceeds must be reinvested. | The entire capital gains must be reinvested. |

| No. of properties eligible for exemption. | NA | One-time exemptions are available for investments in two provinces, provided the gains are less than Rs 2 crore. |

This scheme was introduced by the government of India in 1988 under the Income Tax Act to help the concerned taxpayers save on capital gains. Here's how CGAS works:

A taxpayer who wants to sell an asset and claim a tax exemption under either Section 54 or 54F can use this account scheme. The taxpayer can deposit the money from selling the original assets into the CGAS account until they are looking to purchase or construct a new residential house.

The Capital gains account works like a fixed deposit, providing the taxpayer with some extra time to realize the capital gains into a new residential property. The capital gains account should be opened with an authorized bank in India, and the amount deposited in such an account can only be used either to build or purchase a new house within a specific time frame.

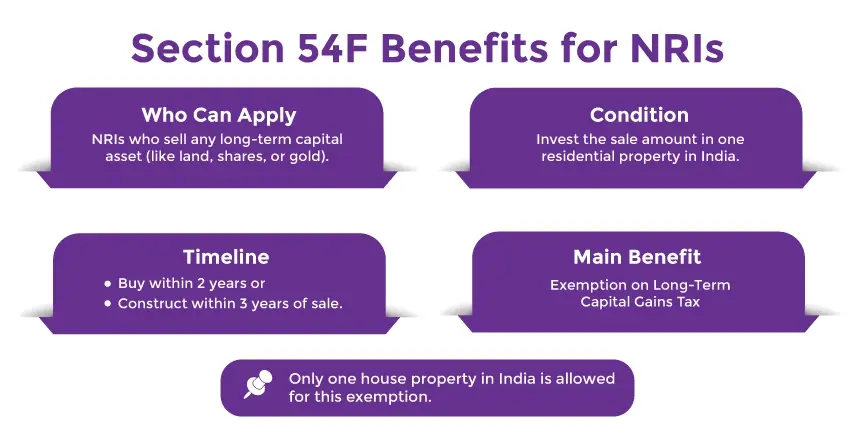

Section 54F brings in a lot of benefits for Indian residents and non-indian residents (NRIs) like:

We at Savetaxs provide a varied range of tax services, including NRI income tax consultancy, ITR filing, repatriation, and more. We have a team of experts with over 30 years of combined experience providing NRIs with personalized NRI tax planning to optimize the capital gain tax liability of each client while ensuring they deserve every exemption possible.

Savetaxs boasts a staggering client base of thousands of NRIs like you, being a beacon of the kind of services we offer. So, what's stopping you? We are available 24/7 across all time zones to provide our clients with the best long-term capital gain tax for NRI advice possible.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1782996918646.png&w=828&q=75)

_1782911003992.webp&w=828&q=75)

_1782823781148.webp&w=828&q=75)