_1779454749573.webp&w=828&q=75)

NRI Returning to India

Managing Money Before Returning to IndiaManaging Money Before Returning to India

Written by Hatim Dudhiyawala

Moving back to India after living in the UAE is a significant life change that includes both emotional and practical aspects. It's more than just relocating from one nation to another; it's about going back to your roots while adjusting financially, emotionally, and professionally. No matter where you have been living in Dubai, planning your return to India as an NRI needs careful planning and prepration.

From understanding your residential status and taxation to managing your NRE/NRO account and repatriating savings. There are several aspects to consider when moving back to India from the UAE to ensure a smooth transition. In this guide, we will cover everything you need to know about returning to India from the UAE. After reading the blog, you can plan your return confidently and avoid any financial or compliance issues.

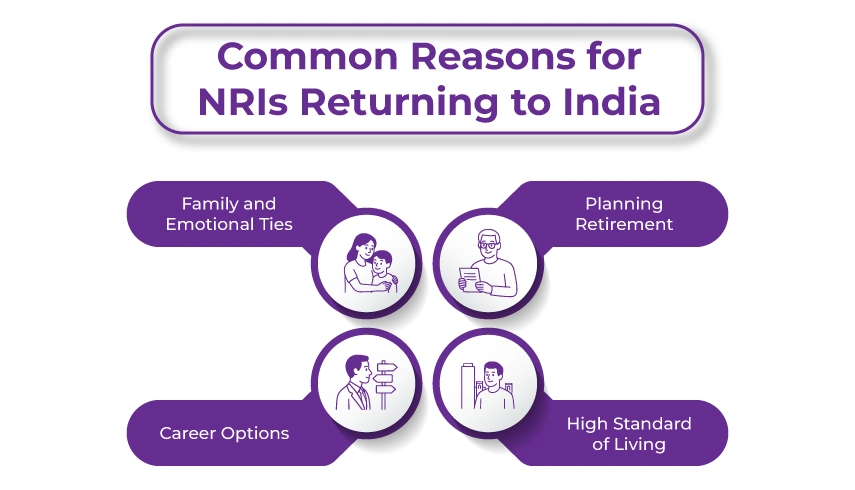

An NRI might have several reasons to return to India from the UAE. The reasons may vary, but mostly it revolves around family, long-term security, low-cost living, and the desire for belonging.

Here are some of the common reasons for an NRI deciding to move back to India from the UAE:

After your return to India, one essential thing you must do is to determine your Residential Status under Indian tax laws. Your tax liability will depend on the duration you have spent in India during a financial year.

Under the Income Tax Act, 1961, an individual can be classified into three categories:

Initially, most of the NRIs qualify as RNOR for up to two years. During this period, you can claim tax relief as your foreign income is not taxed immediately in India, such as a UAE salary or savings.

You will be deemed a resident if you:

You will qualify as RNOR if you:

The UAE is a tax-free jurisdiction, meaning NRIs staying there don't need to pay personal income tax. However, after moving back to India, your income and assets will be taxed under Indian taxation depending on your residency status.

Expereince tailored, accurate, and premium tax filing service at your fingertips to maximize savings.

Even though the UAE doesn't charge any personal income tax, the India-UAE DTAA (Double Taxation Avoidance Agreement) ensures that NRIs don't face double taxation on some income, such as dividends, interest, and royalties.

You get the option to claim a tax credit in India under the DTAA, provided you have already paid taxes on such income in the UAE. For example, on certain investments, earnings.

After a change in your residential status to a resident Indian, you need to update your banking arrangements in accordance with the RBI guidelines.

When you become a resident Indian, you must:

You need careful planning when transferring your savings from the UAE to India to ensure compliance with the regulations of both nations:

After returning, managing your assets in both nations becomes an essential part of your financial planning.

If you own a property or investment in the UAE, you can either:

UAE-based end-of-service benefits (gratuity) can also be claimed tax-free in the UAE. However, once you get the status of an Indian resident, these amounts may be subject to taxation, unless transferred beforehand.

Upon return, you can explore:

To reflect your new residency status, you must update your wills, nominations, and power of attorney (POA). It includes both India and UAE assets in your estate plan to ensure easy inheritance.

Additionally, dual-country estate planning is advisable if your family or dependents are in both nations.

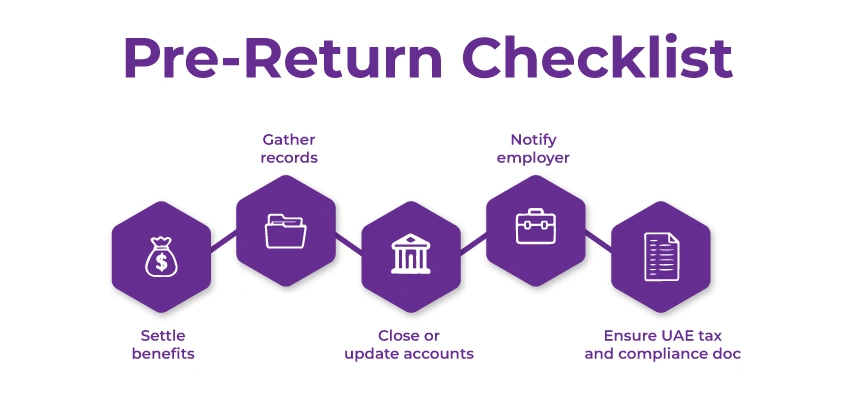

Consider this pre-return and post-return checklist to ensure that you stay compliant before leaving the UAE and after arriving in India.

Here are the things to do before leaving the UAE:

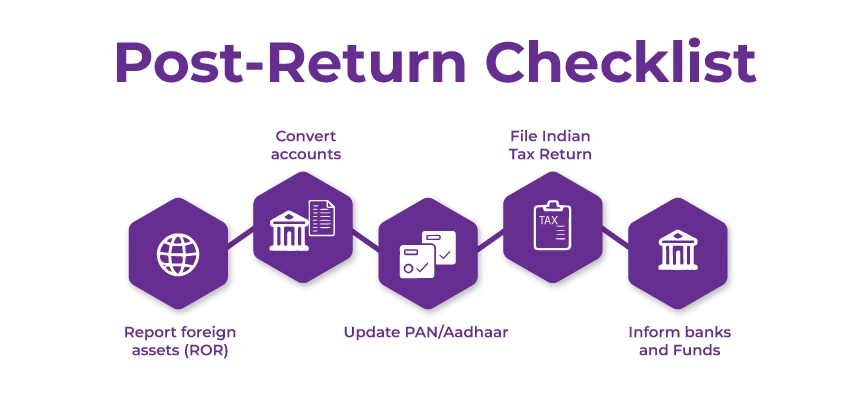

Here are the things you need to do once you have arrived in India:

Consult personal experts and get end-to-end solutions for all your tax obligations and financial planning.

Moving back to India from the UAE is a life-changing journey, emotionally, financially, and culturally. Reconnecting with your family and adapting to life back home can be exciting, but you must not forget to plan everything to ensure a smooth and compliant transition.

Take sufficient time to plan everything carefully and enjoy the new opportunities that await you. Additionally, consider seeking help from an expert to navigate the financial and legal complexities easily. One such expert is Savetaxs.

At Savetaxs, we have a team of expert CAs and professionals, working 24*7 to assist NRIs with all their legal, financial, and tax issues. We can guide you when you decide to move back from the UAE to India in determining your residential status, converting your bank accounts, filing NRI ITR, and much more.

Contact us today, and enjoy utmost convenience and highest quality service, all while sitting in the comfort of your home.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1778504462654.webp&w=828&q=75)

_1777726294138.webp&w=828&q=75)

_1771668297202.webp&w=828&q=75)