_1779454749573.webp&w=828&q=75)

NRI Returning to India

Managing Money Before Returning to IndiaManaging Money Before Returning to India

Written by Hatim Dudhiyawala

Apart from changing locations, an NRI returning to India from Australia after spending years is a major turning point. It's not only about changing countries, but also about transitioning financially, emotionally, and professionally. An NRI needs careful preparation when moving back to India, regardless of whether you have been living in Sydney, Melbourne, or Perth.

You need to consider several things, including financial matters, tax implications, and documentation. An NRI (Non-Resident Indian) might feel overwhelmed by the questions that come to their mind when returning to India - "How will my Australian income be taxed in India?'. 'What about my NRE and NRO accounts?' 'What happens to my residency status?' etc.

In this Blog, we will provide answers to all your questions to help you experience a smooth and well-planned transition when moving back to India from Australia.

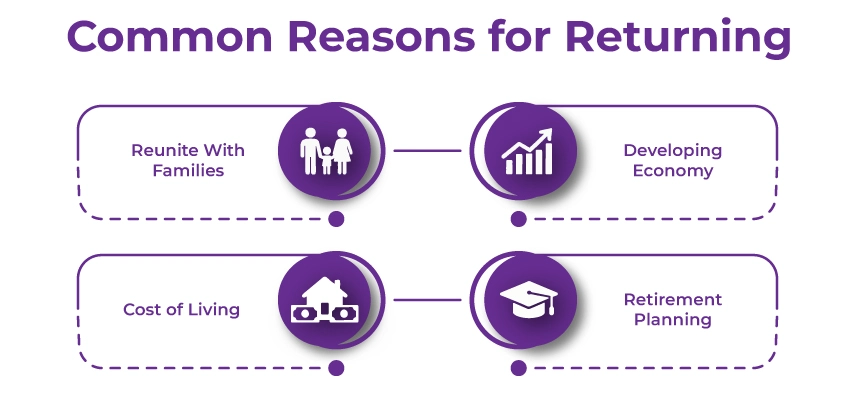

Before moving ahead, let's understand what could be the common reasons behind an NRI planning to move back to India. The reasons may differ widely depending on the individual. Some individuals are attracted by family connections, while others are drawn by professional opportunities and developing a feeling of belonging.

Here are some of the common reasons behind an NRI wanting to move back to India from Australia:

Once you move back to India, determining your Residential Status under the Indian tax law is vital to plan all your finances effortlessly. It will help you understand what income will be subject to taxation in India and the duration for which you can claim tax exemptions on your foreign income.

According to the Indian Income Tax Act, 1961, an individual's residency status is determined based on the number of days they stay in India during a financial year. There are three possible categories:

Upon your return, you may be deemed an RNOR for up to two years, provided you have been staying in Australia for several years. This status offers a transition period where your foreign income is not immediately taxed in India.

File NRI Income Tax Returns promptly on time to meet all legal requirements while maximizing your deductions and avoiding penalties.

You will be considered a resident if you stay:

RNOR status applies if you have not been a resident for nine out of the previous ten years or haven't stayed in India for more than 729 days in the last seven years.

You must be paying taxes in Australia if you have been living and working there. However, under the India-Australia DTAA (Double Taxation Avoidance Agreement), you can ensure that you are not being taxed twice on the same income.

You can claim a foreign tax credit for taxes you have already paid in Australia upon becoming a resident in India.

An NRI's tax implications can get complex once they move back to India, especially if they hold property, investments, or superannuation in Australia. You must understand how your income will be taxed to plan better and avoid any future surprises.

During your RNOR period, income earned overseas will remain exempt from taxation in India. It includes salary, pension, or rental income from Australian property. However, once you get the ROR status, your global income will be taxed under Indian law.

It means, suppose you own a rental property in Melbourne or have investments in the Australian stock market. Then, you will have to declare the income generated, and it will be taxed in India once your RNOR period concludes.

The DTAA between India and Australia prevents you from being taxed twice on the same income in two different nations. In case you have already paid taxes in Australia on your superannuation on property rental income. Then, you can claim the amount as a tax credit while filing your Indian returns.

This agreement plays a crucial role in reducing the financial burden for returning NRIs and ensuring compliance with the tax systems of both nations.

Once you transition from being an NRI to a resident, you need to change your banking arrangements. It includes converting your exisitng NRE, NRO, and FCNR accounts in accordance with the RBI guidelines.

When you become a resident Indian:

An RFC account is mainly useful if you wish to save funds for future needs or travel in Australian Dollars.

You need to follow both Indian and Australian financial regulations while repatriating funds from Australia to India. To transfer funds, you must use official channels like SWIFT transfers through authorized banks.

Planning your finances doesn't stop at repatriation for returning NRIs. Managing your existing foreign assets and exploring new investment options in India are also essential.

You have three options if you own property or investments in Australia: retain, sell, or repatriate the proceeds. The process becomes easier if you sell the property before your return. However, if you plan to rent it out, be ready to report this income in India after your RNOR period concludes.

Australian superannuation funds also need attention. You may withdraw it based on your eligibility once you leave Australia permanently. The amount you withdraw will be subject to taxation in Australia. However, it can be adjusted under DTAA in India.

You can explore the following when back in India:

Make sure that your wills, nominations, and power of attorney (POA) documents are updated to show your current status. When you include both your Indian and Australian assets in your will, you can enjoy a seamless transfer to beneficiaries. Additionally, if you have dependents in both nations, estate planning becomes essential for you.

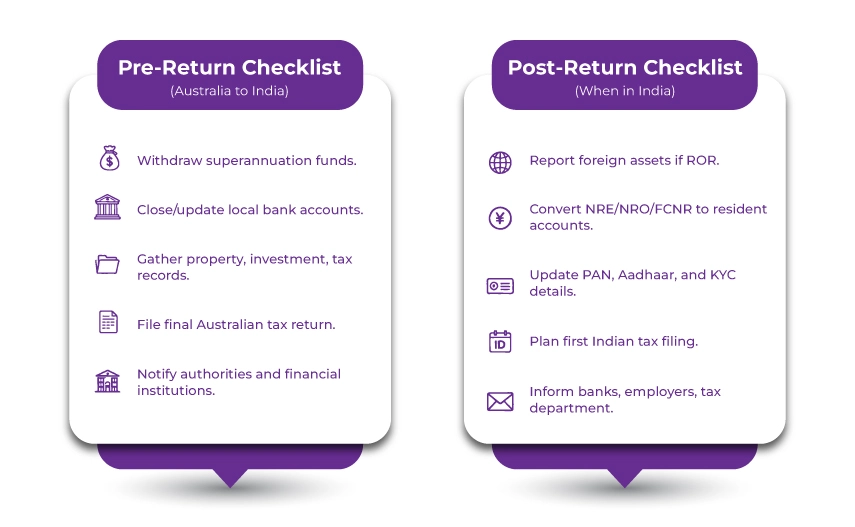

Consider this pre-return and post-return checklist to make your transition smooth and well-prepared:

Before you depart from Australia, ensure to:

After returning to India, you must:

Get customized assistance from experts who will handle your Income Tax Filing to maximize your refund.

Reuniting with your family and coming back home after spending years abroad can be exciting as well as overwhelming. It might take time to adjust to the fast-paced lifestyle, bureaucracy, and cultural nuances. With this checklist, you can navigate this transition easily. Ensure to take the necessary steps before and after moving back to India to ensure compliance and enjoy a hassle-free return to India.

Furthermore, understanding the legal and financial complexities might get stressful, so consider seeking help from an expert at Savetaxs. At Savetaxs, we are dedicated to assisting NRIs with their tax obligations and financial planning. Our team of professionals can help you navigate all the complexities easily. Be it converting your bank accounts, filing NRI ITR, completing exit tax, or determining your residential status, we can help you throughout. We are actively working around the clock across all time zones, so contact us anytime and enjoy the peace of mind you deserve while we handle your tax issues.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1778504462654.webp&w=828&q=75)

_1777726294138.webp&w=828&q=75)

_1771668297202.webp&w=828&q=75)