_1779454749573.webp&w=828&q=75)

NRI Returning to India

Managing Money Before Returning to IndiaManaging Money Before Returning to India

Written by Hatim Dudhiyawala

Far more than a change of address, for NRIs moving back to India after spending many years in Malaysia is a major transition. It's an event in life in which you need to adjust emotionally, financially, and professionally. Thoughtful prepration is a must when relocating to India, despite where you have been living in Malaysia.

You will need to plan for finances, taxes, documentation, and lifestyle adjustments well in advance. Some questions may arise in an NRI's mind, such as "Will my Malaysian income be taxable in India?" What to do with my NRE or NRO accounts?' and much more.

Keep reading this guide to get answers to all such questions and enjoy a smooth and well-planned transition back to India from Malaysia.

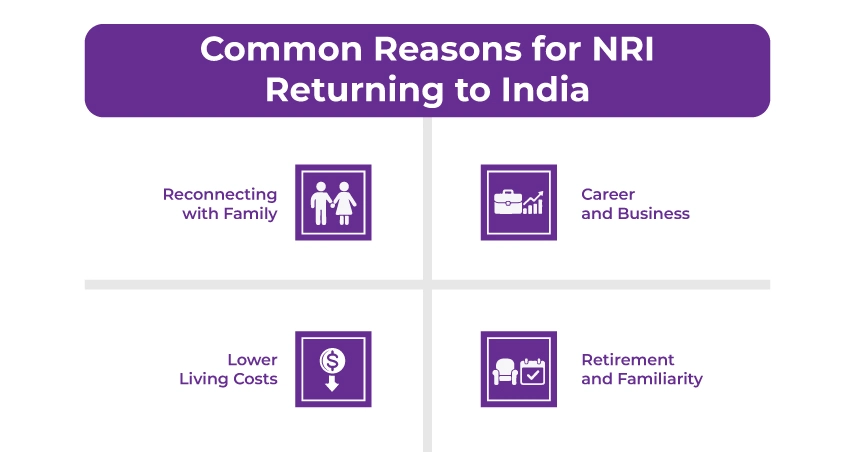

It's worth exploring the reasons behind an NRI deciding to move back to India after spending years in Malaysia. From family ties, professional opportunities, to emotional fulfillment, the reasons may differ from person to person.

Your residential status in India determines how your income will be taxed. According to the Indian Income Tax Act, an individual is classified depending on the number of days they spend in India during a financial year.

An individual falls into three categories under the Indian Income Tax Act, 1961:

For example, if you have been staying in Malaysia for a considerable time, you will probably qualify as an RNOR for up to two years after your return. During this duration, your Malaysian income will not be taxed immediately in India.

You will be deemed a resident if:

You qualify as an RNOR if:

If you have been working in Malaysia, you must have been paying taxes to the Inland Revenue Board of Malaysia (IRBM). Fortunately, you can prevent paying taxes twice on the same income through the DTAA between India and Malaysia.

Once you arrive in India, you can claim a foreign tax credit in India for the taxes you have already paid in Malaysia. This will ensure that you align with the tax regulations of both nations without being taxed twice.

Relocating to India can make your tax liabilities more complex, specifically if you own property, investments, or EPF (Employment Provident Funds) savings in Malaysia.

Your overseas income is tax-exempt in India during your RNOR period. It includes your salary, dividends, or rental earnings received from Malaysia. Your global income will be taxable under Indian laws after you become an ROR.

For example, if you own a rental apartment in Kuala Lumpur or hold shares in a Malaysian company. Then, the income generated from these must be declared and taxed in India after the RNOR period concludes.

The DTAA helps avoid double taxation and permits you to claim credit for taxes paid in Malaysia while filing your Indian tax return. This will ensure smooth financial management and compliance with both nations' tax systems.

Ensure timely NRI ITR filing while fulfilling all legal requirements and maximizing deductions.

Your banking setup must also be updated in line with the regulations of the RBI once your residential status changes.

When you become a resident, you should:

RFC accounts are ideal for people who still have an overseas income or future travel plans.

You must follow both Indian and Malaysian financial regulations when repatriating funds. Consider using authorized banking channels like SWIFT to ensure transparency and compliance.

Your financial planning doesn't stop after returning home. You should manage your foreign assets and discover new investment opportunities in India.

If you hold a property or investment in Malaysia, you can either retain it or sell it before returning. If you sell them before relocating, you can simplify taxation.

However, if you continue to receive rent from it, then the income acquired will be taxed in India after you gain the ROR status.

Additionally, withdrawals from Malaysia's EPF are subject to local tax, but it can be adjusted through the DTAA while filing taxes in India.

After resettling in India, consider:

It's advised to update your will, nominations, and power of attorney (POA) to show your residential status. Include both Indian and Malaysian assets in your estate planning to ensure a smooth transfer to the successor.

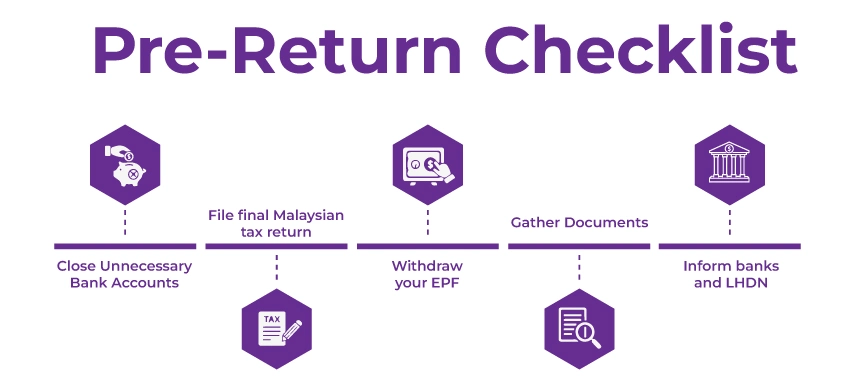

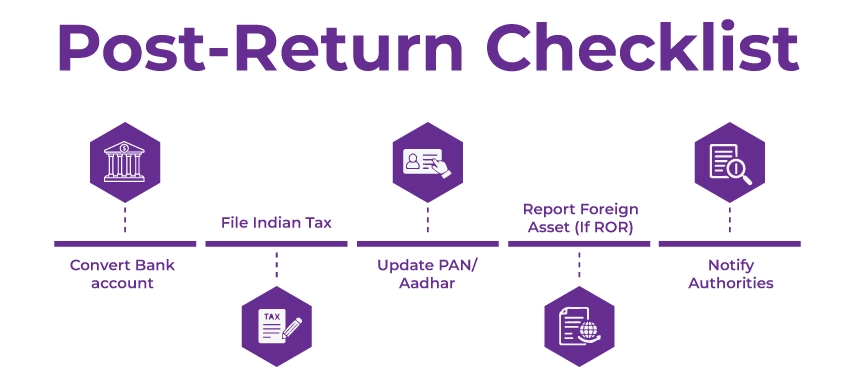

Here is a pre-return and post-return checklist to consider so that you stay well-prepared and compliant while going through this transition.

You should make sure to do the following things before you move back to India:

After arriving in India, ensure to:

Avoid worrying about complying with the regulations with our expert solutions.

Moving back to India from Malaysia can be both exciting and challenging. You get a chance to reunite with your roots, explore new opportunities, and stay close to family. However, this transition also needs careful financial and tax planning.

You can make this tra nsi tion much easier by preparing in advance and understanding your obligations. Additionally, for more accurate compliance and an easy transition, seek expert guidance from Savetaxs.

At Savetaxs, we specialize in assisting NRIs with tax compliance and financial planning. Our team of experts can guide you through everything, from determining residency status to claiming DTAA benefits and filing tax returns. Contact us right away, and we will handle your tax issues so that you can focus on starting your new chapter in India without any worries.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1778504462654.webp&w=828&q=75)

_1777726294138.webp&w=828&q=75)

_1771668297202.webp&w=828&q=75)