_1784624542261.png&w=828&q=75)

NRI Income Tax Compliance

7 Mistakes That Could Trigger an Income Tax Notice for salaried employees7 Mistakes That Could Trigger an Income Tax Notice for salaried employees

Written by Shubham Jain

A foreign source of income is earnings derived from an activity or source located outside India. In India, an individual's tax obligations depend on their residential status and source of income.

Generally, Indian residents pay tax on their global income, while NRIs pay tax on income received in India. According to section 5 of the Income Tax Act, 1961, an Indian resident is liable to pay tax on their global income, whether it is earned from local or foreign sources.

Want to know more about how foreign sources of income are taxed in India? Read the blog and get all the information.

As mentioned above, a foreign source of income can be defined as the income that is earned outside your resident country. It includes dividends, royalties, interest, and fees for technical services from outside sources.

To consider your income earned outside India, you should conduct the following activities overseas. Further, you may also provide your services from within the country. However, they should be used by an individual working outside India.

Apart from this, even if the income is earned overseas, it is advisable not to receive it directly in your Indian bank account. The first receipt of it should be received outside India. This helps you remit the income to India later.

So, this was all about foreign source income. Moving ahead, let's know how India taxes this income.

Across the globe, all countries impose the income tax based on two rules: the residency rule and the source rule. The same taxation rule is also followed by India.

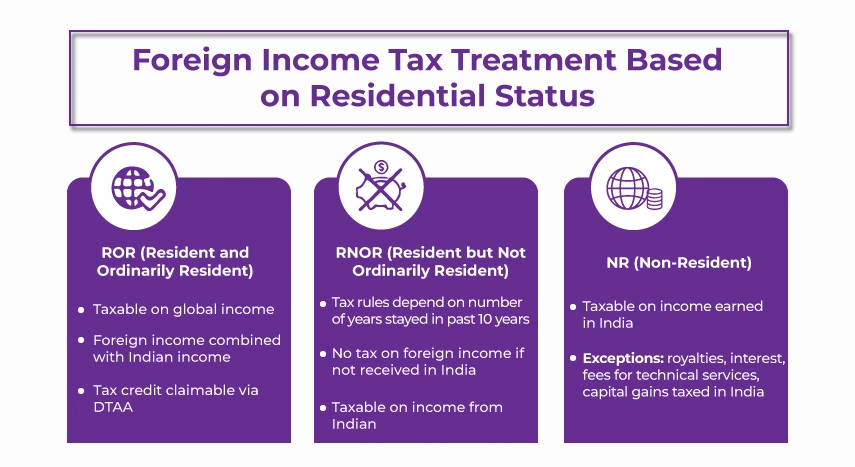

Considering this, in India, the residential status of an individual is divided into three groups, i.e., non-resident (NR), Resident, and ordinary resident (ROR) and Resident but not ordinary resident (RNOR). Further, according to the residential status, the person pays tax in India.

Confused, let's understand this better in the next section.

Here is how India imposed tax on foreign income based on the Residential Status of the taxpayer:

This was all about how foreign source income is taxed in India. Moving further, let's know how DTAA helps in avoiding paying tax on the same income twice.

To solve the issue of double taxation, wherein income is taxation in both the residence and source countries, the Double Taxation Avoidance Agreement (DTAA) comes as a relief. India has signed this agreement with several foreign countries. It helps the taxpayers in claiming tax relief from the already paid tax on foreign income against the tax payable in India.

Considering this, using the DTAA, taxpayers can claim a foreign tax credit on the income that is liable to be taxed in both India and a foreign country. Under sections 90 and 91 of the Income Tax Act, you can claim this tax credit benefit. Through these sections, taxpayers get relief from paying taxes on the same income twice in two different countries.

Further, to avail the DTAA benefits, you need to consider the following things:

This is how DTAA helps taxpayers in India avoid paying taxes on the same income twice. However, to claim the tax benefits, it is vital to mention all your foreign assets in Schedule FA. Additionally, report your foreign source of income in Schedule FSI (foreign source of income) when filing your ITR form. Only then will you be able to claim the tax benefit.

Now, moving ahead, let's know how to claim the foreign tax credit in India.

Here are the steps that you need to follow to claim a foreign tax credit in India:

This is how you can claim a foreign tax credit in India. Moving further, let's know the common mistakes that NRIs often make while filing taxes in India.

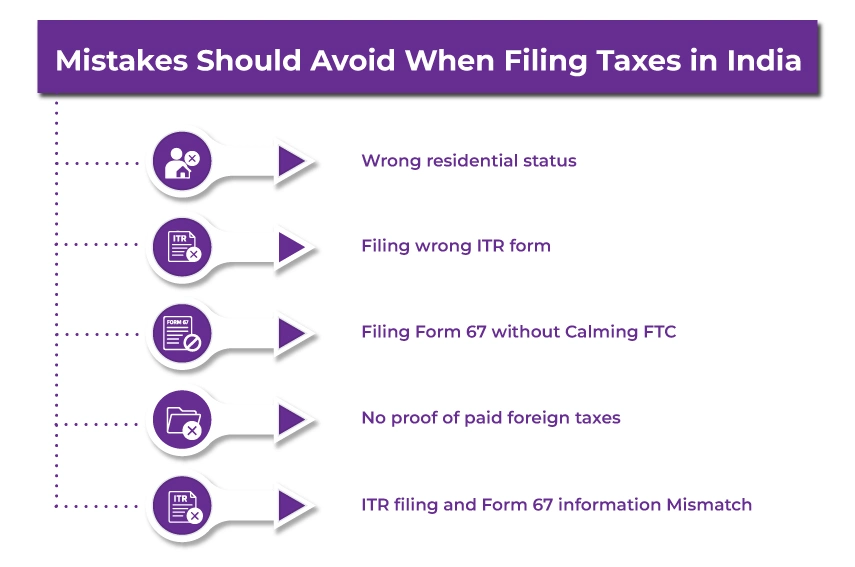

Here are some of the common mistakes that NRIs should avoid when filing taxes in India:

These are some of the common mistakes that NRIs often make when filing their ITR.

Lastly, this was all about the taxation of foreign sources of income in India. Under the DTAA signed between India and other foreign countries, you can claim FTC and avoid paying twice the taxes on your foreign income. However, for this, you need to fulfill several requirements, such as filing out Form 67 and more.

Furthermore, if you need more information about foreign source income or need assistance in claiming the DTAA benefits, connect with Savetaxs. We have a team of professionals who will help you out in this and solve all your tax-related queries.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784624729370.webp&w=828&q=75)

_1784547039242.webp&w=828&q=75)

_1784546974133.webp&w=828&q=75)