_1784618918411.webp&w=828&q=75)

NRI Income Tax Compliance

7 Mistakes That Could Trigger an Income Tax Notice for salaried employees7 Mistakes That Could Trigger an Income Tax Notice for salaried employees

Written by Shubham Jain

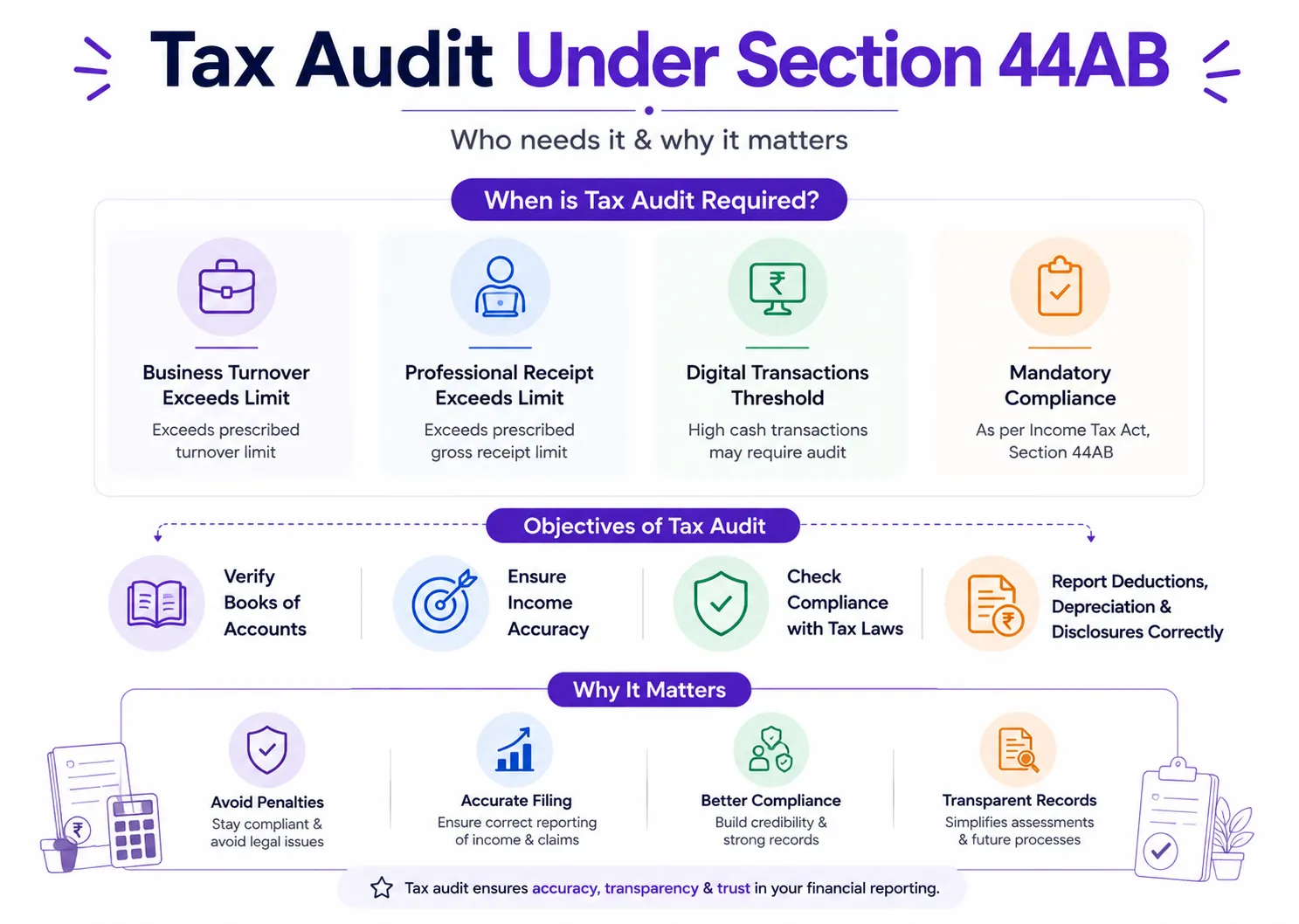

An Income Tax Audit under Section 44AB is an examination of a taxpayer’s books of accounts by a Chartered Accountant to verify compliance with the Income Tax Act. Tax audit is applicable to businesses with turnover exceeding ₹1 crore and professionals with gross receipts above ₹50 lakh.

The turnover limit for businesses increases to ₹10 crore if cash receipts and cash payments do not exceed 5% of total transactions. The due date for filing the tax audit report for FY 2025-26 (AY 2026-27) is 30 September 2026, while taxpayers covered under transfer pricing provisions must file the audit report by 31 October 2026.

Failure to comply with Section 44AB may attract a fee under Section 271B of 0.5% of turnover or ₹1.5 lakh, whichever is lower.

| Particulars | Limits |

|---|---|

| Business turnover limit | ₹1 crore |

| Digital transaction turnover limit | ₹10 crore |

| Professional receipts limit | ₹50 lakh |

| Tax audit due date | 30 September 2026 |

| Transfer pricing due date | 31 October 2026 |

| Fee under Section 271B | Lower of 0.5% or ₹1.5 lakh |

A tax audit is the examination and verification of books of accounts by a Chartered Accountant from an income tax compliance perspective. Under Section 44AB of the Income Tax Act, taxpayers crossing the prescribed turnover or gross receipt limits are required to get their accounts audited and submit the audit report electronically.

The objective of tax audit is to:

Tax audit helps the Income Tax Department verify whether taxpayers have correctly reported income and complied with applicable tax laws. It also simplifies the computation of taxable income, deductions, depreciation, and other claims.

For Financial Year (FY) 2025-26 corresponding to Assessment Year (AY) 2026-27, the due date for completing and furnishing the tax audit report is:

The tax audit report must be submitted electronically before filing the Income Tax Return (ITR).

The primary objectives of tax audit under Section 44AB are:

A tax audit also improves financial transparency and ensures that taxpayers maintain proper accounting records as prescribed under the law.

A taxpayer is required to get a tax audit conducted if the turnover or gross receipts exceed prescribed limits during a financial year.

The applicability limits are:

Apart from the above, tax audit may also apply in certain cases under presumptive taxation schemes.

Suppose a business has:

In this case, tax audit may not apply because cash transactions are within the 5% limit and the enhanced turnover threshold of ₹10 crore becomes applicable.

However, if cash receipts or cash payments exceed 5%, the normal turnover threshold of ₹1 crore will apply.

The following categories of taxpayers are required to get their books of accounts audited under Section 44AB of the Income Tax Act:

| Category of Taxpayer | Condition | Tax Audit Applicable When |

|---|---|---|

| Business (Not opting for presumptive taxation) | Carrying on business | Turnover exceeds ₹1 crore |

| Business with digital transactions | Cash receipts & payments do not exceed 5% | Turnover exceeds ₹10 crore |

| Business under Section 44AD | Declares lower profit than prescribed | Income exceeds basic exemption limit |

| Business opting out of Section 44AD | Within lock-in period of 5 years | Income exceeds exemption limit |

| Business under Sections 44AE/44BB/44BBB | Declares lower profit than presumptive income | Tax audit applicable |

| Profession | Carrying on profession | Gross receipts exceed ₹50 lakh |

| Profession under Section 44ADA | Declares profit below 50% of receipts | Income exceeds exemption limit |

| Business loss cases | Turnover exceeds prescribed limits | Tax audit applicable |

Tax audit may also become applicable under presumptive taxation schemes in the following situations:

Tax audit becomes mandatory if:

Professionals opting for presumptive taxation under Section 44ADA must get tax audit done if:

Tax audit is applicable where taxpayers declare lower profits than prescribed under these presumptive taxation provisions.

If a taxpayer has already got the books of accounts audited under another law, a separate audit under the Income Tax Act is not required.

For example:

In such cases, the taxpayer only needs to furnish the prescribed tax audit report under Section 44AB before the due date of filing the return.

The tax auditor must furnish the audit report in prescribed forms depending on the applicability.

Form 3CA is applicable where the taxpayer is already required to get accounts audited under another law.

Form 3CB is applicable where the taxpayer is not required to undergo audit under any other law.

Form 3CD is a detailed statement containing particulars related to:

Form 3CD must be filed along with either Form 3CA or Form 3CB.

Form 3CE applies to non-residents and foreign companies receiving royalties or technical service fees from the Government or Indian concerns.

The tax audit report must be filed electronically through the Income Tax Department’s e-filing portal by a Chartered Accountant.

The process generally involves:

If the taxpayer rejects the audit report, the process must be repeated until acceptance.

If a taxpayer fails to get accounts audited as required under Section 44AB, a fee under Section 271B may be levied. The fee shall be lower of:

As proposed in Budget 2026, this amount will now be treated as a fee instead of a penalty to reduce litigation.

Non-compliance with tax audit provisions may also result in:

No fee under Section 271B may be imposed if the taxpayer can prove a reasonable cause for failure to comply.

Some commonly accepted reasonable causes include:

Courts and tribunals have accepted such genuine hardships in various cases.

Tax audit offers several advantages to businesses and professionals, including:

It also helps taxpayers identify accounting discrepancies and rectify them before filing returns.

Tax audit under Section 44AB is an important compliance requirement for businesses and professionals exceeding prescribed turnover or gross receipt limits. Understanding tax audit applicability, due dates, turnover thresholds, and filing requirements can help taxpayers avoid notices, fees, and legal complications.

Timely compliance with tax audit provisions also improves financial transparency and ensures accurate reporting of income, deductions, and tax liability. Businesses and professionals should maintain proper books of accounts and seek professional guidance wherever necessary to ensure smooth and compliant tax filing.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784617942800.webp&w=828&q=75)

_1784547039242.webp&w=828&q=75)

_1784546974133.webp&w=828&q=75)