NRI Income Tax & Compliance

Income Tax E-ProceedingsIncome Tax E-Proceedings

Written by Hatim Dudhiyawala

Looking for a simple way to claim tax benefits on home loan interest, HRA, Section 80C investments, and more? Then you must know about Form 12BB - a standardized tax declaration form introduced on 1 June 2016 by the Central Board of Direct Taxes (CBDT). Since its launch, it has become a crucial document for salaried employees and Non-Resident Indians (NRIs) earning income in India.

Under Section 80C, NRIs can claim deductions up to INR 1.5 lakh, resulting in tax savings depending on the applicable slab rate.

For both residents and NRIs, Form 12BB is mandatory if you want your employer to consider deductions while calculating TDS. By declaring eligible investments, expenses, and tax-saving instruments, you can claim deductions up to INR 1,50,000 under Section 80C along with other allowances, including HRA, LTA, Section 24(b), and more.

If you are an NRI with income taxable in India, this guide will help you understand why Form 12BB for NRIs is important and how to use it effectively.

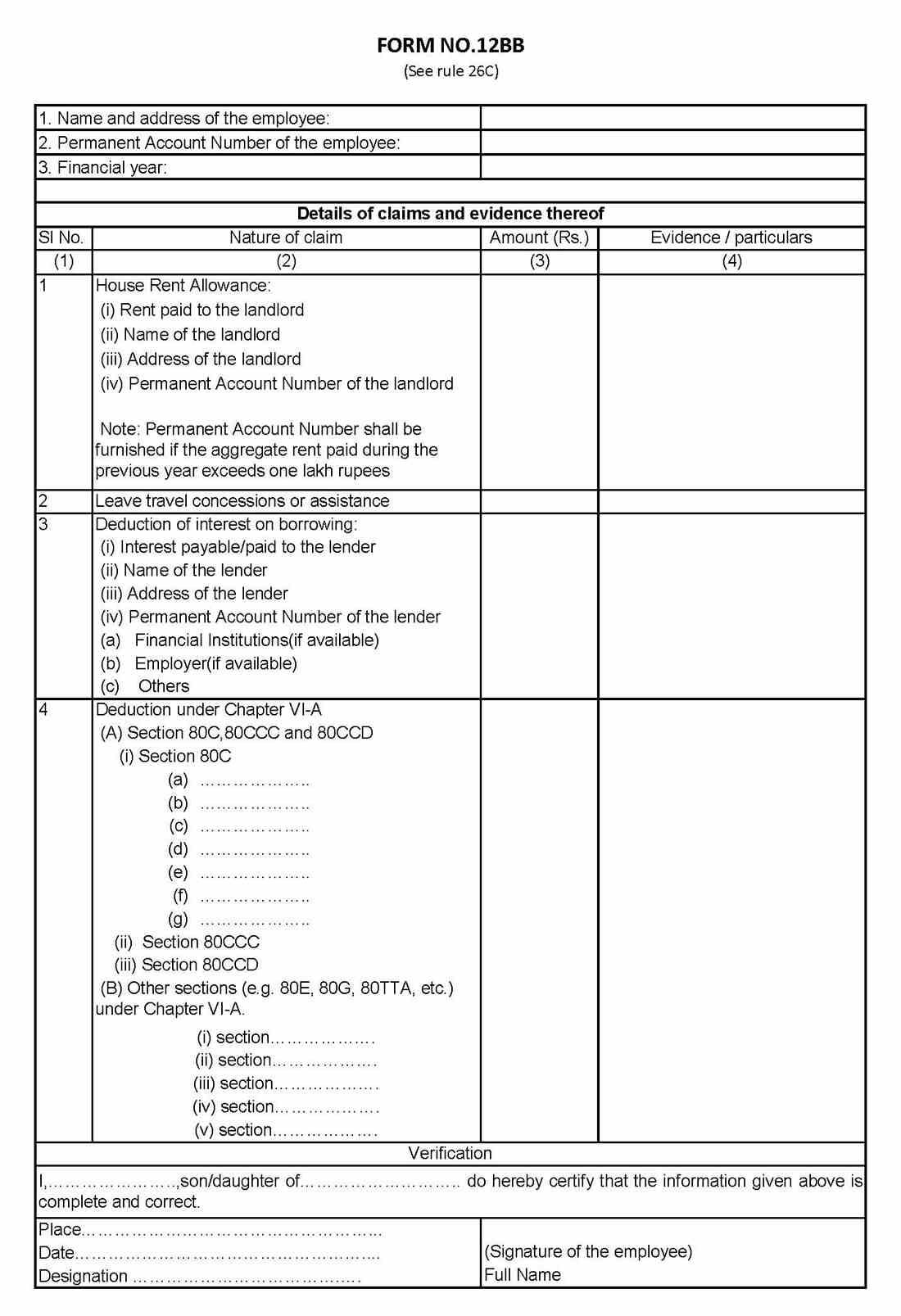

Form 12BB is a unified tax declaration form for salaried individuals, introduced by the CBDT to standardize investment and deduction declarations that employees submit to employers.

Before 2016, employers used inconsistent formats for tax declarations. Form 12BB replaced all of them with one universal format.

You do not submit Form 12BB to the Income Tax Department. It must be submitted directly to your employer, usually between January and February every year.

For NRIs in particular, this helps streamline tax planning and prevent unnecessary TDS deductions.

For NRIs earning salary income in India, Form 12BB functions as a salary-based deduction declaration to the employer.

NRIs with salary income in India can use Form 12BB as a tax shield. However, without giving this form to your company or employer, you cannot get tax relief from the deducted TDS on your salary. Based on the declarations you made in Form 12BB, your employer calculates your monthly applicable tax deduction. Through this form, you can streamline your tax planning in the following ways:

Form 12BB includes the following details:

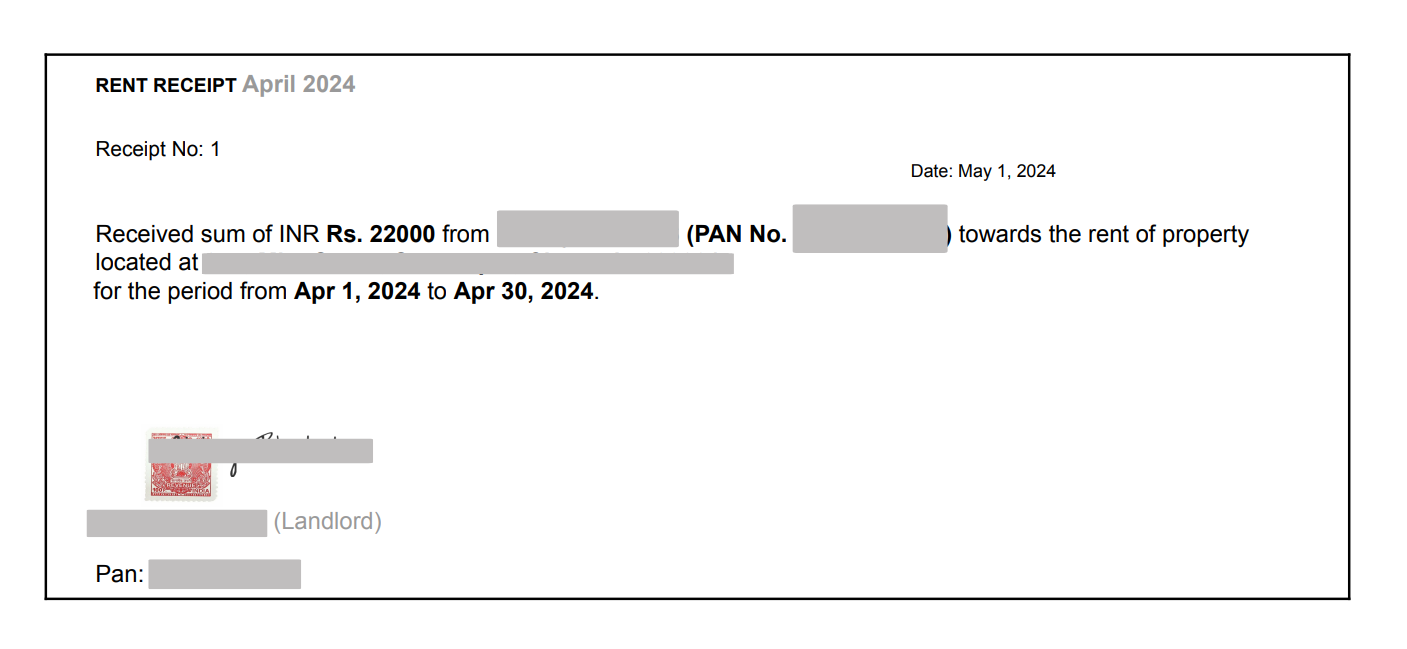

If HRA is included in your salary, you must declare:

Important Notes:

LTA is one of the few allowances that offer tax-exempt domestic travel.

Eligibility

Key Rules

Accommodation expenses are not exempt.

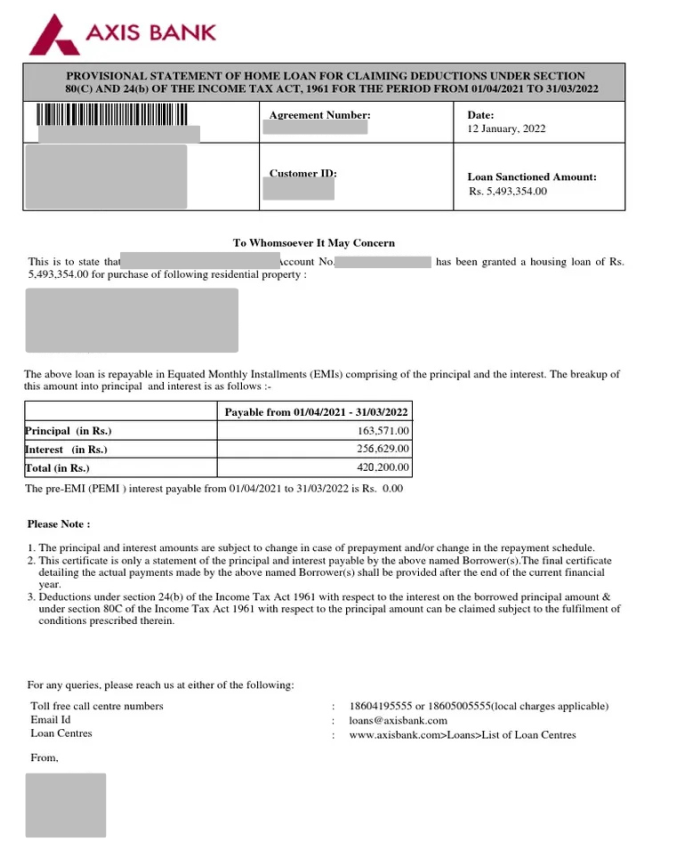

NRIs can claim interest deduction on home loans taken for:

Details Needed in Form 12BB

Tax Benefits for NRIs

Proof Required

Disclaimer: This image is for educational purposes only.

This is the final section of Form 12BB and contains the maximum tax deduction available under Chapter VI-A of the Income Tax Act. It includes several sections, such as 80C investments, Section 80G donations, and more. See the table below for the available deductions.

| Sections | Conditions to Avail | Maximum Deduction |

|---|---|---|

| 80C | Tax deduction for expenses and investments such as Public Provident Fund (PPF), life insurance premiums, National Savings Certificates (NSC), Employee Provident Fund (EPF), payment of tuition fees, and principal repayment of a housing loan. | INR 1,50,000 |

| 80CCC | Tax deductions for employees' contributions to pension funds offered by the private and public sectors. | INR 1,50,000 |

| 80CCD | An additional deduction is available for contributions of employees to the National Pension System (NPS) | INR 2,00,000 |

| 80D | Tax deduction available for medical insurance premiums for self, parents, spouse, and dependent children. | INR 25,000, which can be increased to INR 50,000 if parents are senior citizens. |

| 80E | Deduction for paid interest on the loan taken for higher studies. | Available for 8 years |

| 80G | Deduction for donations given to political parties, charitable organizations, and trusts. | Based on the donation type, the limit varies |

| 80TTA | Tax deductions for earned interest on savings accounts. | INR 10,000 |

The final section requires:

This verifies that all declarations made are accurate and supported by documents.

Before submitting your NRI tax declaration form, ensure:

Whether you are an Indian resident or an NRI, it is essential to manage your tax obligations in India. In this, Form 12BB is a vital component to save tax on your investments. Through this blog, we have provided you with all the information about this form and how you can claim tax deductions through this. Moreover, if you need more guidance on Form 12BB or are facing issues in filing out this form, consider taking help from a tax expert like Savetaxs. We have a team of professionals who assist you in solving your tax-related queries and help you in filing your ITR on time. So connect with us now.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1782475363401.webp&w=828&q=75)