_1782996918646.png&w=828&q=75)

NRI Income Tax & Compliance

NRE Fixed Deposits: Eligibility, Benefits, NRE FD Rate, and MoreNRE Fixed Deposits: Eligibility, Benefits, NRE FD Rate, and More

Written by Shubham Jain

Among global professionals, NRIs, and investors, cross-border income has become very common. However, earning income in different jurisdictions comes with one major issue, i.e., double taxation. It means you are liable to pay tax on the same income twice, once in your resident country and once in the country where you generated this income. To reduce the tax burden and avoid double taxation, the government introduced the Foreign Tax Credit (FTC) under DTAA. While this process looks straightforward, the timeline to claim foreign tax credit is often misunderstood by taxpayers. It further led to missing tax relief, compliance notices, delayed refunds, and processing disputes.

Considering this, it is now a strategic compliance necessity to understand the FTC timeline among NRIs and global investors. Additionally, the Central Board of Direct Taxes has extended the time limit to claim foreign tax credit. Now, eligible taxpayers can file Form 67 on or before the end of the relevant assessment year, subject to prescribed return filing conditions.

Want to know more about the timeline to claim the foreign tax credit? Read the blog and get your answers.

Before diving into the timeline to claim foreign tax credit, let's first understand the related concept. Let's start by knowing what a foreign tax credit is. You can define foreign tax credit as a mechanism under the Double Tax Avoidance Agreement (DTAA) signed by India with 90+ countries that allows taxpayers to claim credit on their already paid taxes on the same income. In short, it helps you avoid paying taxes twice on the same income. In India, FTC is generally available under:

However, you did not get the FTC automatically. Yes, you read it right. FTC is governed by Rule 128 of the Income Tax Rules, 1962. To claim the tax credit, you need to provide documentary evidence, correct currency conversion, and, most importantly, timely filing of the Form 67.

Considering this, whether the tax credit is allowed smoothly, pushed into litigation and verification, or restricted during processing, the FTC timeline plays an essential role. Additionally, the Central Board of Direct Taxes has made a significant change in Rule 128 of the Income Tax Rules that provided a major relief to individuals claiming FTC. Now, you can claim the FTC on or before the end of the relevant assessment year. Further delays or incorrect sequencing can lead to:

So you can say that the current compliance environment, timing has become as vital as substantive eligibility.

This was all about the foreign tax credit and why the timeline matters in this. Moving ahead, let's know the financial year alignment and FTC eligibility.

Connect with Savetaxs and fulfill your tax obligations with professional support.

The first and most vital step in understanding the timeline to claim the foreign tax credit is aligning the foreign income and taxes with the correct Indian financial year. In India, you generally claim the FTC in the same year when you report your foreign income for tax purposes. This includes:

You should match the above-mentioned foreign income to your Indian financial year when it is taxable. For instance, if you disclose your foreign income in FY 2025-26, the foreign taxes you claim as FTC should match that income. If there is any mismatch in years, it results in denial of tax credit, inquiries from the tax department, or limited allowances. This is specifically vital if:

Hence, from the above information, it is clear that to claim the foreign tax credit, it is vital to synchronize your income and tax filings. Now, moving ahead, let's understand the process to claim FTC.

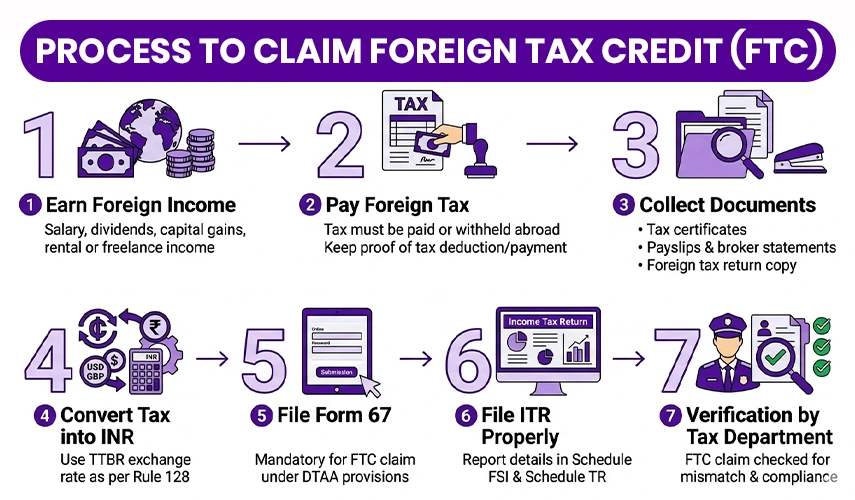

Claiming the foreign tax credit is not about filling out a form; you need to follow the proper steps carefully. To help you out, here is a simplified breakdown of the process:

The timeline to claim the foreign tax credit starts when you have earned foreign income. It includes:

Here, the foreign income type determines the applicability of DTAA benefits and your eligibility for foreign tax credit.

You can only claim the foreign tax credit if it has been:

Additionally, you should have the evidence that shows the following things:

Without paying the foreign tax, you cannot claim the foreign tax credit.

According to Rule 128, to claim the foreign tax credit, you need to have proper documents. It includes:

Further, missing any of these documents can lead to mismatch notices.

You cannot claim the foreign tax credit using approximate exchange rates. Considering this, under the FTC rules, the tax paid overseas using the Telegraphic Transfer Buying Rate (TTBR) should be converted into INR. It should be done immediately on the last day of the month preceding the month in which such taxes were deducted or paid. It is technical, but an essential compliance point. Moreover, incorrect conversion often leads to:

Form 67 is mandatory to claim tax relief under sections 90, 90A, and 91. This form is a statutory foreign tax credit disclosure statement. It contains the following information:

To claim the foreign tax credit, it is vital to fill out Form 67 on time. According to the current Rule 128 framework, the form should be filled out online within the stated statutory timeline associated with the financial year. Further, for FY 2024-25, the foreign tax credit claim deadline was March 31, 2026, subject to valid tax return filing conditions.

However, from a practical compliance perspective, ideally, taxpayers should file Form 67 before or along with ITR. It helps in avoiding:

Additionally, to avoid issues like processing delays or auto-disallowance, it is best to file Form 67 along with your tax return.

You cannot claim only through Form 67. Considering this, you should disclose the foreign tax information in:

Further, if the information mentioned in Form 67 and Schedule FSI, and Schedule TR, did not match, during the process, your FTC can be rejected.

Once you file the tax returns, the Income Tax Department of India verifies the following information:

Any mismatch can result in:

This is how you can claim a foreign tax credit. Now moving further, let's see the FTC timeline table.

The table below showcases the foreign tax credit timeline:

| FTC Stage | Required Action | Ideal Time | Practical Outer Limit |

|---|---|---|---|

| Foreign Income Earned | Determine foreign taxable income | During the financial year | During the relevant financial year |

| Foreign tax paid/ deducted | Preserve tax proof | Same month/ quarter | Before ITR prep |

| Document collection | Gather statements/ certificates | Before the ITR season | Before Form 67 |

| TTBR conversion working | Prepare INR computation | During ITR prep | Before claiming the foreign tax credit |

| Form 67 filing | Upload the FTC statement | Before ITR filing | Within the Rule 128-stated timeline |

| ITR filing with Schedule FSI/ TR | Claim FTC in ITR | Due date/ belated return period | According to section 139 |

| Rectification/ response | Handle mismatch notices | Immediately after CPC processing | Case specific |

This is the general timeline for the foreign tax credit. Moving forward, let's know the common timing mistakes taxpayers make while claiming the foreign tax credit.

The common timeline mistakes that taxpayers make when claiming FTC are:

These are the common mistakes that taxpayers unknowingly make while claiming foreign tax credit. Now moving ahead, let's know the tips to avoid these mistakes.

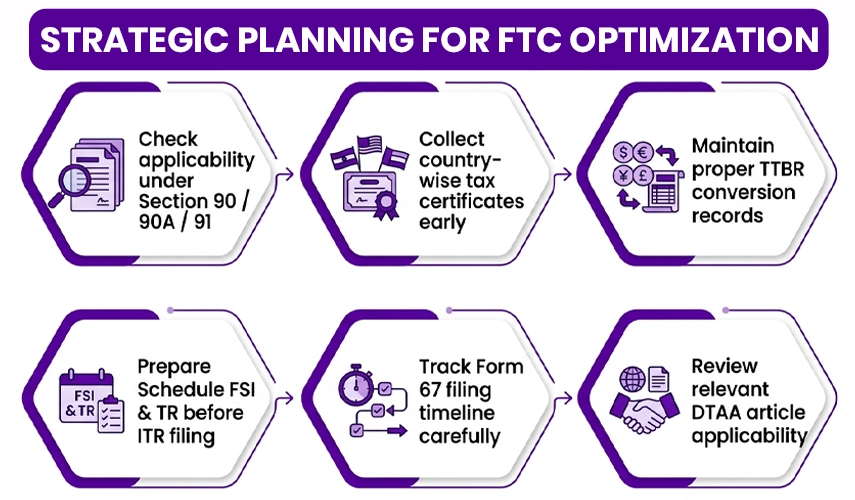

To avoid mistakes in FTC, with form filing, you should do strategic planning. This includes:

Following this structure converts FTC from a filing burden to a structured tax-saving strategy. Still confused? Moving further, let's understand this with a real-world example.

Let's assume Mr. A is an NRI who, while being a tax resident in India, earns a consulting income in the US.

In this scenario, Mr. A will smoothly get the foreign tax credit. However, if he:

In this scenario, the foreign tax credit claim of Mr. A during the automated processing will be denied even though he genuinely paid the foreign tax credit.

Furthermore, let's know the challenges taxpayers face in claiming cross-border FTC.

From tax filing to deduction and compliance, the experts at Savetaxs handle everything for you.

Here are some of the common challenges that taxpayers generally face in cross-border FTC claims:

These are the common challenges in cross-border FTC claims that taxpayers often face.

Lastly, in today's global tax environment, to reduce double taxation on foreign income, a foreign tax credit is an essential tool. However, it is vital to follow the proper timeline to claim the foreign tax credit from foreign income recognition to ITR submission to get the benefits. It is because even if you do not properly manage the timeline to claim FTC, a technically eligible claim can get disputed or delayed.

Furthermore, if you need any assistance in filing Form 67, calculating FTC, evaluating DTAA relief, or handling cross-border tax disclosures, connect with Savetaxs. We have a team of financial experts who will help in managing the complete process with compliance and accuracy.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1782911003992.webp&w=828&q=75)

_1782823781148.webp&w=828&q=75)